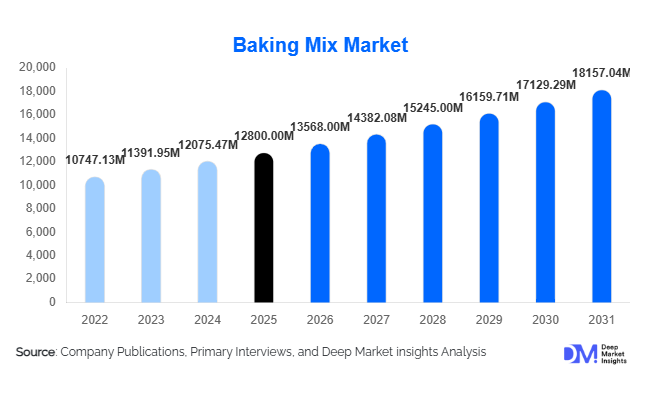

Global Baking Mix Market Size

According to Deep Market Insights, the global baking mix market size was valued at USD 12,800 million in 2026 and is projected to grow from USD 13,568 million in 2027 to reach USD 18,157.04 million by 2031, expanding at a CAGR of 6.0% during the forecast period (2026–2031). The baking mix market growth is primarily driven by rising demand for convenience foods, increasing penetration of home baking culture, expansion of modern retail and e-commerce channels, and growing consumer preference for clean-label and health-oriented baking solutions such as gluten-free and organic mixes.

Key Market Insights

- Cake mixes dominate the global baking mix industry due to high household usage and strong demand during celebrations and everyday baking activities.

- North America remains the largest regional market, supported by strong retail infrastructure, high home baking penetration, and established branded product consumption.

- Asia-Pacific is the fastest-growing region, driven by urbanization, rising disposable income, and increasing Western food adoption patterns.

- E-commerce channels are expanding rapidly, enabling niche and premium baking mix brands to reach global consumers without traditional retail dependency.

- Health-focused baking mixes such as gluten-free and high-protein variants are gaining strong traction, driven by dietary awareness and lifestyle disease concerns.

- Dry baking mixes dominate product form due to longer shelf life, cost efficiency, and ease of transportation.

baking mix market latest trends

Rising Demand for Clean-Label and Functional Baking Mixes

The baking mix industry is undergoing a major shift toward clean-label formulations, with consumers increasingly demanding products free from artificial preservatives, additives, and synthetic flavors. Manufacturers are responding with organic, non-GMO, and nutrient-enriched mixes containing whole grains, plant-based proteins, and fiber. Functional baking mixes targeting specific health needs such as high-protein, keto-friendly, and diabetic-safe formulations are expanding rapidly. This trend is particularly strong in developed markets such as North America and Europe, where health-conscious consumption is reshaping packaged food categories. Brands that emphasize ingredient transparency and nutritional benefits are gaining a competitive edge in premium segments.

Digital Retail and Home Baking Culture Expansion

The rise of digital commerce platforms and social media-driven food culture is significantly influencing the baking mix market. Online grocery platforms and direct-to-consumer (DTC) brands are reshaping distribution dynamics by offering personalized baking kits, subscription models, and niche artisanal products. Social media platforms continue to fuel home baking trends through recipe sharing, influencer-led baking content, and cooking tutorials. This has led to sustained post-pandemic growth in home baking activity, particularly among younger consumers. Technology-enabled personalization and recipe integration are further enhancing consumer engagement and driving repeat purchases across online channels.

baking mix market drivers

Rising Demand for Convenience and Time-Saving Food Solutions

Modern lifestyles characterized by busy work schedules and urban living patterns are driving strong demand for convenient food preparation solutions. Baking mixes eliminate the need for multiple ingredients and complex preparation processes, offering consistent results with minimal effort. This convenience factor is particularly appealing to beginners and time-constrained households, making baking mixes a staple in urban kitchens across developed and emerging economies.

Growth of Home Baking and Recreational Cooking Trends

Home baking has evolved from a necessity-driven activity to a lifestyle and recreational trend, fueled by digital media platforms, cooking shows, and influencer content. The COVID-19 pandemic further accelerated this behavior, and the trend has remained strong post-pandemic. Consumers increasingly engage in baking as a hobby, leading to higher consumption of cake, cookie, and pancake mixes. This behavioral shift continues to support long-term market expansion.

Expansion of Organized Retail and E-Commerce Infrastructure

The rapid expansion of supermarkets, hypermarkets, and online grocery platforms has significantly improved product availability and visibility. E-commerce platforms in particular are enabling global accessibility for niche and premium baking mix brands, supporting category penetration in emerging markets. This distribution transformation is enhancing consumer choice and driving volume growth across both urban and semi-urban regions.

global market restraints

Perception of Processed Food and Health Concerns

Despite innovation in clean-label and organic formulations, baking mixes are still perceived by some consumers as processed food products containing preservatives and refined ingredients. This perception limits adoption among highly health-conscious consumers and restricts penetration in certain premium wellness-focused segments.

Raw Material Price Volatility

Fluctuations in the prices of wheat, sugar, cocoa, dairy, and other core ingredients significantly impact production costs. This volatility affects profit margins and pricing stability across the value chain. Manufacturers are often required to adopt hedging strategies and long-term procurement contracts to manage cost fluctuations.

baking mix industry key opportunities

Expansion of Gluten-Free and Specialty Baking Segments

The increasing prevalence of gluten intolerance, lifestyle diseases, and dietary customization is driving strong demand for gluten-free, keto, and allergen-free baking mixes. This segment presents a high-margin opportunity for manufacturers, especially in developed economies where health-oriented consumption is rapidly increasing.

Growth of Emerging Markets and Urban Consumption

Rapid urbanization and rising disposable incomes in Asia-Pacific, Latin America, and the Middle East are expanding the consumer base for baking mixes. Increasing exposure to Western diets and expansion of modern retail formats are further accelerating adoption in countries such as India, China, Brazil, and the UAE.

Private Label and Direct-to-Consumer Brand Expansion

Retailers and startups are increasingly launching private-label baking mixes and D2C brands to capture margin advantages and consumer loyalty. Digital-first strategies, subscription models, and personalized baking kits are enabling new entrants to compete effectively against established FMCG players.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12800.00 Million |

| Market Size in 2026 | USD 13568.00 Million |

| Market Size in 2031 | USD 18157.04 Million |

| CAGR | 6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Cake mixes continue to dominate the global baking mix market, accounting for the highest consumption share due to their strong association with celebrations, home baking traditions, and growing commercial bakery usage. Their popularity is further supported by increasing demand for convenient, time-saving dessert preparation solutions and consistent product outcomes in both household and professional settings. Bread mixes hold a significant share of the market, driven by the rising trend of home baking, artisanal bread preparation, and consumer preference for fresher, preservative-free baked goods. The growing health consciousness among consumers has also encouraged the adoption of whole grain and multigrain bread mix variants, further strengthening this segment’s expansion.Cookie and biscuit mixes are witnessing steady growth, particularly among younger consumers who prefer quick snack solutions with minimal preparation effort. Their appeal is reinforced by innovation in flavors, portion control packaging, and indulgence-oriented positioning. Pancake and waffle mixes maintain consistent demand, especially in North America and Europe, where breakfast consumption habits are well established and consumers increasingly seek convenient yet quality breakfast alternatives. Specialty baking mixes, including gluten-free, vegan, and high-protein variants, represent the fastest-growing segment, fueled by rising dietary awareness, lifestyle-driven food choices, and premiumization trends that emphasize health, functionality, and ingredient transparency.

Application Insights

Household consumption remains the largest application segment, driven by the growing popularity of home baking, increased experimentation with recipes, and a broader shift toward convenience-oriented cooking habits. The expansion of social media influence and baking-focused content has further encouraged consumers to adopt baking mixes as easy-to-use solutions for homemade products. Commercial bakeries represent a stable and essential segment, relying on baking mixes to ensure consistency in taste, texture, and quality while optimizing operational efficiency and reducing preparation time and costs.The HoReCa sector is expanding steadily, supported by rising demand from hotels, restaurants, and cafés that require standardized baked goods for large-scale service delivery and menu consistency. Growth in global tourism and hospitality infrastructure has further strengthened this segment. Industrial food manufacturers are increasingly incorporating baking mixes as base ingredients in packaged bakery products, frozen foods, and ready-to-eat snacks, driven by scalability and formulation control advantages. Emerging applications are centered around functional and health-focused bakery products, including protein-enriched baked goods, low-sugar formulations, and ready-to-bake meal kits, reflecting strong innovation momentum in the functional food and wellness category.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate distribution due to strong product visibility, consumer trust, and the ability to offer wide product assortments under one roof. These channels benefit from promotional strategies, in-store sampling, and established consumer purchasing habits. However, online retail is emerging as the fastest-growing channel, driven by convenience, broader product selection, competitive pricing, and the increasing popularity of subscription-based grocery services. Digital platforms are also enabling niche and premium baking mix brands to reach targeted consumer segments more effectively.Specialty health food stores are expanding in urban markets, catering to increasing demand for organic, gluten-free, and clean-label baking mixes among health-conscious consumers. Foodservice and bakery supply distributors remain critical for commercial demand, ensuring consistent bulk supply to bakeries, hotels, and institutional buyers. The rise of direct-to-consumer models is reshaping the competitive landscape, with brands leveraging digital marketing, personalized product recommendations, and e-commerce platforms to build stronger consumer engagement and loyalty.

End-Use Insights

The household segment leads the baking mix market, supported by rising home baking adoption, convenience-driven lifestyles, and increasing interest in culinary experimentation. Consumers are increasingly seeking easy-to-use solutions that deliver bakery-style results at home without requiring advanced baking skills. Commercial bakeries continue to expand steadily, driven by the need for standardized production, operational efficiency, and consistent product quality across large volumes.The HoReCa segment is witnessing strong growth, particularly in urban hospitality environments and café chains, where demand for quick-service desserts and baked goods is increasing. Industrial applications are also expanding as baking mixes are widely used as foundational ingredients in packaged bakery products, snacks, and frozen food categories, enabling manufacturers to streamline production processes. Export-driven demand is gaining momentum, with developed regions such as North America and Europe supplying premium baking mixes to emerging markets in Asia-Pacific and the Middle East, supporting global trade expansion and product diversification.

Explore more data points, trends and opportunities Download Free Sample Report

Baking Mix Market Segmentations

By Product Type

- Cake Mixes

- Bread Mixes

- Cookie & Biscuit Mixes

- Pancake & Waffle Mixes

- Brownie Mixes

- Pastry & Dough Mixes

- Specialty & Functional Mixes

By Ingredient Base

- Wheat-Based Baking Mixes

- Gluten-Free Baking Mixes

- Multigrain & Fiber-Enriched Mixes

- Keto & Low-Carb Baking Mixes

- Organic & Natural Baking Mixes

By Form

- Dry Powder Mixes

- Ready-to-Bake Batter Mixes

- Frozen Dough-Based Mixes

- Liquid Concentrate Mixes

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail / E-commerce

- Specialty Health Food Stores

- Foodservice & Bakery Distributors

By End Use

- Household Consumers

- Commercial Bakeries

- HoReCa (Hotels, Restaurants, Cafés)

- Industrial Food Manufacturers

Regional Insights

North America

North America leads the global baking mix market, accounting for approximately 34% of global demand in 2025. The region’s dominance is driven by a strong home baking culture, high consumption of convenience foods, and widespread availability of branded packaged baking products. The United States remains the primary growth engine, supported by high consumer awareness, strong retail penetration, and growing demand for premium and health-oriented baking mixes. Canada also contributes significantly, with rising preference for organic, gluten-free, and clean-label products. The regional growth is further supported by robust e-commerce infrastructure, product innovation, and increasing demand for functional bakery offerings aligned with health and wellness trends.

Europe

Europe holds around 28% of the global market share, with strong contributions from Germany, the United Kingdom, and France. The region benefits from a long-standing bakery tradition and well-established consumption patterns across both household and commercial segments. Growth in Europe is strongly driven by increasing consumer preference for clean-label, organic, and sustainably sourced baking mixes, supported by stringent food quality regulations and environmental awareness. Demand for premium and specialty bakery products is rising as consumers shift toward healthier indulgent alternatives and artisanal-style baking solutions.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, supported by rapid urbanization, rising disposable incomes, and the growing influence of Western dietary habits. China and India are the key growth contributors, driven by expanding middle-class populations, increasing adoption of convenience foods, and the rapid expansion of modern retail and e-commerce platforms. Japan and Australia represent mature but stable markets with steady demand for premium baking mixes. Growth in the region is further fueled by the rising café culture, expansion of bakery chains, and strong digital retail penetration, which is significantly improving product accessibility across urban and semi-urban areas.

Latin America

Latin America is an emerging market, led by Brazil and Mexico, where increasing urbanization and evolving consumer lifestyles are driving demand for packaged and convenient food products. The growth of café culture and quick-service restaurants is significantly contributing to baking mix adoption across urban centers. Rising retail modernization and improved distribution networks are enhancing product availability, while growing middle-class populations are supporting demand for affordable and mid-range bakery solutions. The region also shows increasing potential for premium and flavored baking mix categories as consumer preferences diversify.

Middle East & Africa

The Middle East and Africa region is witnessing steady growth, driven by strong demand from Gulf countries such as the UAE and Saudi Arabia, where tourism, hospitality expansion, and high disposable incomes are key growth drivers. The increasing number of hotels, restaurants, and international food chains is boosting demand for standardized baking solutions. In Africa, growth is supported by rapid urbanization, expanding retail infrastructure, and rising consumer exposure to packaged and convenience foods. The region overall is benefiting from demographic expansion, tourism development, and gradual lifestyle shifts toward modern food consumption patterns.

Key Players in the Baking Mix Market

- General Mills

- Conagra Brands

- Dr. Oetker

- Associated British Foods

- Kerry Group

- Puratos

- Cargill

- Archer Daniels Midland (ADM)

- Aryzta

- Dawn Foods

- Bob’s Red Mill

- King Arthur Baking Company

- Simple Mills

- Europastry

- Hain Celestial Group