Baking Ingredients Market Size

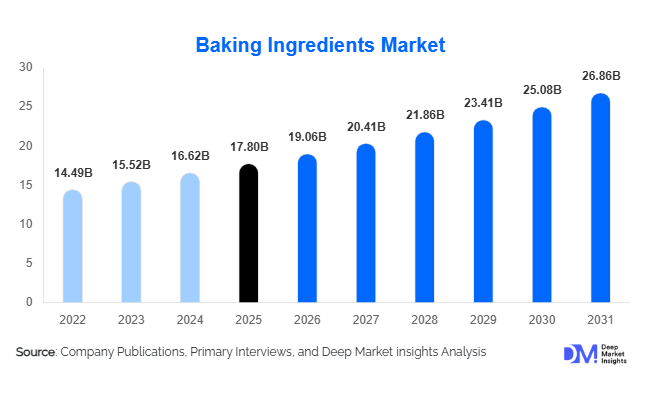

According to Deep Market Insights, the global baking ingredients market size was valued at USD 17.8 billion in 2025 and is projected to grow from USD 19.06 billion in 2026 to reach USD 26.86 billion by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). The baking ingredients market growth is driven by rising consumption of packaged and frozen bakery products, expanding industrial bakery capacity, and increasing demand for clean-label, organic, and functional baking formulations across global food systems.

Key Market Insights

- Industrial bakeries dominate global demand, accounting for the largest share of ingredient consumption due to large-scale, standardized production.

- Flour remains the backbone of the market, supported by consistent global consumption of bread and staple baked goods.

- Europe leads global market share, driven by strong bakery traditions and high per-capita bread consumption.

- Asia-Pacific is the fastest-growing region, supported by urbanization, rising incomes, and westernization of diets.

- Clean-label and enzyme-based ingredients are gaining traction as manufacturers reformulate products to meet regulatory and consumer demands.

- Frozen and ready-to-bake formats are accelerating demand for specialty baking ingredients with enhanced shelf-life performance.

What are the latest trends in the baking ingredients market?

Clean-Label and Natural Ingredient Reformulation

The baking ingredients market is undergoing a structural shift toward clean-label formulations, as consumers increasingly scrutinize ingredient lists for artificial additives and preservatives. Enzymes, natural emulsifiers, and plant-based fats are replacing chemical dough conditioners and synthetic stabilizers. This trend is particularly strong in North America and Europe, where regulatory frameworks and consumer advocacy have accelerated adoption. Manufacturers are investing heavily in R&D to maintain product texture, volume, and shelf life while reducing artificial inputs.

Growth of Frozen and Ready-to-Bake Bakery Products

Demand for frozen dough, par-baked bread, and ready-to-bake bakery items is rising rapidly across retail and foodservice channels. These formats require specialized baking ingredients that enhance freeze-thaw stability, fermentation control, and moisture retention. As global QSR chains and modern retail expand, ingredient suppliers offering application-specific blends are gaining a competitive advantage.

What are the key drivers in the baking ingredients market?

Rising Global Consumption of Packaged Bakery Products

Urban lifestyles, longer working hours, and demand for convenient foods are driving increased consumption of packaged bread, biscuits, cakes, and pastries. Industrial bakeries rely heavily on standardized baking ingredients to maintain consistency across large volumes, directly supporting sustained market growth.

Expansion of Foodservice and QSR Chains

The rapid expansion of quick-service restaurants, bakery cafés, and pizza chains is significantly boosting demand for yeast, flour blends, emulsifiers, and functional ingredients. Asia-Pacific and Latin America are witnessing the fastest growth in foodservice-driven baking ingredient demand.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in wheat, sugar, dairy, and vegetable oil prices pose margin pressure for both ingredient suppliers and bakery manufacturers. Climate variability and geopolitical disruptions continue to impact agricultural supply chains.

Stringent Regulatory and Labeling Requirements

Regulatory compliance related to food additives, allergens, and organic certifications increases formulation complexity and cost, particularly in developed markets.

What are the key opportunities in the baking ingredients industry?

Clean-Label and Functional Ingredient Innovation

Growing demand for healthier baked goods presents opportunities for enzyme-based solutions, sugar-reduction systems, and fiber-enriched formulations. Suppliers that offer multifunctional ingredients can command premium pricing and secure long-term supply contracts.

Emerging Market Expansion

Asia-Pacific, the Middle East, and Africa offer strong growth opportunities due to rising bakery consumption and government support for food processing infrastructure under initiatives such as Make in India and Vision 2030.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 17.8 Billion |

| Market Size in 2026 | USD 19.06 Billion |

| Market Size in 2031 | USD 26.86 Billion |

| CAGR | 7.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Flour dominates the global baking ingredients market, accounting for approximately 34% of global demand in 2025, driven by its indispensable role as the primary structural component in bread, biscuits, cakes, and other baked goods. The segment’s leadership is reinforced by consistent consumption of staple bakery products across both developed and emerging economies, along with rising demand for fortified and specialty flours such as whole wheat, multigrain, and gluten-free variants.Sweeteners represent a significant market share, supported by their extensive use in confectionery, cakes, pastries, and indulgent bakery formulations. Growing consumer preference for premium and flavor-enhanced baked products continues to sustain demand, while the shift toward natural sweeteners and reduced-sugar formulations is reshaping product innovation within this segment.

Fats and oils are increasingly transitioning toward plant-based, non-hydrogenated, and specialty lipid systems, driven by clean-label preferences and regulatory pressure to reduce trans fats. These ingredients play a critical role in improving texture, mouthfeel, and shelf life, making them essential for both industrial and artisan bakery applications.Enzymes and emulsifiers, although smaller in volume, are among the fastest-growing product segments. Their growth is primarily driven by clean-label reformulation trends, as manufacturers seek functional solutions to replace chemical additives while maintaining dough stability, volume, and consistency.

Application Insights

Bread and rolls represent the largest application segment, contributing nearly 41% of global market value in 2025. This dominance is driven by high daily consumption, particularly in Europe, Asia-Pacific, and the Middle East, as well as rising demand for packaged and nutritionally enhanced bread products.Cakes and pastries follow as a major application area, supported by premiumization trends in emerging economies. Increased disposable incomes, urban lifestyles, and the growing popularity of celebration-oriented bakery items have strengthened demand for specialty ingredients used in cakes and desserts.

Cookies and biscuits maintain stable demand due to their long shelf life, affordability, and strong export volumes. These products benefit from sustained consumption across both developed and price-sensitive markets, making them a key revenue contributor for ingredient suppliers.Frozen and ready-to-bake bakery products are the fastest-growing application segment, particularly in North America and Asia-Pacific. Growth is fueled by convenience-driven consumption, rising adoption of frozen dough solutions by foodservice operators, and advancements in cold-chain infrastructure.

Distribution Channel Insights

B2B distribution channels dominate the global baking ingredients market, accounting for approximately 68% of total sales. This dominance is driven by bulk procurement by industrial bakeries, foodservice operators, and quick-service restaurant (QSR) chains seeking cost efficiency, consistent quality, and standardized ingredient formulations.

B2C retail channels, including home baking ingredients, are growing steadily through e-commerce expansion, private-label product launches, and rising consumer interest in premium and specialty baking ingredients. Digital retail platforms have significantly improved product accessibility and variety for end consumers.Foodservice supply chains remain a key growth avenue, supported by increasing demand for customized ingredient solutions tailored to large-scale kitchens, cafés, and bakery chains operating across multiple locations.

End-Use Insights

Industrial bakeries lead global demand with nearly 46% market share, driven by large-scale production, private-label bakery growth, and strong partnerships with retail chains and foodservice operators. Automation and process optimization further enhance ingredient consumption in this segment.Artisan bakeries maintain a strong presence in Europe and North America, supported by consumer preference for fresh, handcrafted, and locally produced baked goods. Demand for specialty flours, premium fats, and natural enzymes is particularly high within this segment.

Foodservice and QSR chains represent the fastest-growing end-use segment, driven by menu expansion, standardization of bakery offerings, and rising global consumption of baked snacks and breakfast items.Household baking continues to expand, supported by digital retail platforms, social media influence, and premium home-baking trends that encourage experimentation with professional-grade ingredients.

Explore more data points, trends and opportunities Download Free Sample Report

Baking Ingredients Market Segmentations

By Ingredient Type

- Flour

- Sweeteners

- Fats & Oils

- Leavening Agents

- Emulsifiers

- Preservatives & Shelf-Life Enhancers

- Colors & Flavors

- Dairy Ingredients

By Product Nature

- Conventional Baking Ingredients

- Organic Baking Ingredients

- Clean-Label & Non-GMO Ingredients

By Application

- Bread & Rolls

- Cakes & Pastries

- Cookies & Biscuits

- Pizza & Flatbreads

- Muffins & Cupcakes

- Frozen & Ready-to-Bake Products

By Form

- Dry

- Liquid

- Semi-Solid

By Distribution Channel

- B2B (Industrial & Artisan Bakeries)

- B2C (Retail & Home Baking)

- Foodservice Supply Chains

By End Use

- Industrial Bakeries

- Artisan & Craft Bakeries

- Foodservice & QSR Chains

- Household / Home Baking

Regional Insights

Europe

Europe accounted for approximately 32% of global baking ingredients market share in 2025, led by Germany, France, the U.K., and Italy. High per-capita bread consumption, deeply rooted bakery traditions, and strong demand for clean-label and organic bakery products drive sustained regional growth. Additionally, stringent food quality regulations encourage the adoption of premium and functional ingredients.

Asia-Pacific

Asia-Pacific represented nearly 29% of global demand and is the fastest-growing region, led by China and India. Rapid urbanization, increasing consumption of packaged bakery products, and the expansion of modern retail chains are key growth drivers. India is projected to grow at over 9% CAGR, supported by rising disposable incomes, westernization of diets, and growing investments in industrial baking capacity.

North America

North America held around 24% market share, driven by a highly developed industrial baking sector, strong penetration of frozen and ready-to-bake products, and widespread presence of QSR chains in the U.S. and Canada. Innovation in specialty ingredients, including gluten-free and clean-label solutions, further supports market growth.

Latin America

Latin America is witnessing steady growth, with Brazil and Mexico leading regional demand. Expansion of retail bakeries, rising consumption of packaged bread and sweet baked goods, and increasing foodservice activity are key growth drivers. Improving cold-chain logistics is also supporting the adoption of frozen bakery products.

Middle East & Africa

The Middle East and Africa represent emerging growth markets, supported by rapid population growth, rising urbanization, and increasing imports of baking ingredients. Investments in food processing infrastructure, along with growing demand for packaged and halal-certified bakery products, are strengthening regional market expansion.

Key Players in the Baking Ingredients Market

- Archer Daniels Midland Company

- Cargill, Incorporated

- Kerry Group

- DSM-Firmenich

- Tate & Lyle PLC

- Ingredion Incorporated

- Puratos Group

- Lesaffre Group

- Associated British Foods plc

- International Flavors & Fragrances (IFF)

- Corbion N.V.

- Novozymes

- DuPont (Nutrition & Biosciences)

- Lallemand Inc.

- Roquette Frères