Baking Chocolate Market Size

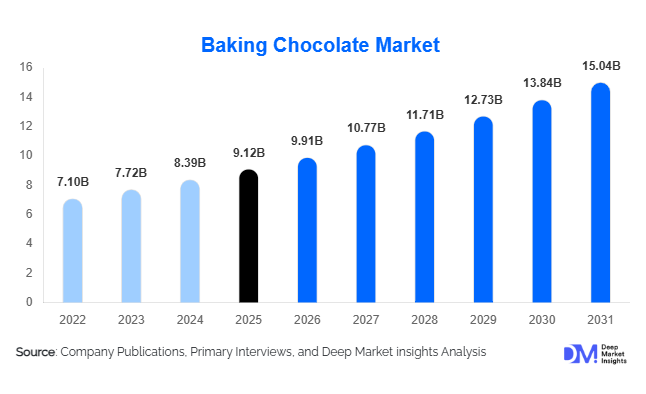

According to Deep Market Insights, theglobal baking chocolate market size was valued at USD 9.12 billion in 2025 and is projected to grow from USD 9.91 billion in 2026 to reach USD 15.04 billion by 2031, expanding at a CAGR of 8.7% during the forecast period (2026–2031). The baking chocolate market growth is primarily driven by the increasing consumption of premium bakery products, rising demand for artisanal confectionery, expanding café culture, and growing popularity of home baking activities across developed and emerging economies.

Key Market Insights

- Dark baking chocolate is increasingly dominating premium bakery applications, supported by consumer preference for high-cocoa-content and lower-sugar formulations.

- Industrial bakery manufacturers are expanding premium dessert portfolios, accelerating demand for couverture chocolate, chocolate chips, and specialty fillings.

- Europe dominates the global baking chocolate market due to advanced chocolate processing infrastructure and strong artisanal baking traditions.

- Asia-Pacific remains the fastest-growing region, driven by urbanization, westernized food consumption, and rapid expansion of café chains in China and India.

- Plant-based and sugar-free baking chocolate categories are emerging rapidly, supported by growing health consciousness and vegan dietary adoption.

- Technological advancements in chocolate refining, tempering, and sustainable cocoa sourcing are reshaping product innovation and manufacturing efficiency globally.

baking chocolate market latest trends

Premium and Artisanal Chocolate Products Gaining Momentum

The baking chocolate industry is witnessing strong growth in premium and artisanal product categories as consumers increasingly seek indulgent, high-quality dessert experiences. Premium couverture chocolate, single-origin cocoa products, and high-cocoa-content dark chocolate are becoming increasingly popular among professional bakers, cafés, and gourmet confectionery manufacturers. Artisanal bakeries are differentiating products using ethically sourced chocolate and unique cocoa flavor profiles, particularly in Europe and North America. Consumers are also showing growing interest in handcrafted desserts, premium pastries, and luxury bakery products that incorporate specialty chocolate ingredients. This trend is encouraging manufacturers to invest in small-batch processing, sustainable sourcing certifications, and advanced flavor development technologies to strengthen premium positioning.

Growth of Vegan and Clean-Label Baking Chocolate

Demand for vegan, dairy-free, and clean-label baking chocolate is expanding rapidly across global markets. Food manufacturers are introducing plant-based formulations using oat milk, almond milk, and coconut-based ingredients to meet evolving dietary preferences. Sugar-reduced and organic chocolate products are also gaining traction due to increasing consumer focus on healthier indulgence. Clean-label positioning, including non-GMO ingredients, reduced additives, and traceable cocoa sourcing, is becoming an important competitive differentiator. E-commerce platforms and specialty ingredient retailers are helping smaller brands expand visibility among health-conscious consumers. This trend is especially strong in North America, Western Europe, and urban Asia-Pacific markets, where younger consumers are driving demand for sustainable and wellness-oriented bakery ingredients.

baking chocolate market drivers

Rising Consumption of Premium Bakery and Dessert Products

The global expansion of premium bakery and dessert consumption is a major growth driver for the baking chocolate market. Consumers are increasingly spending on gourmet pastries, cakes, brownies, cookies, and confectionery products made using premium chocolate ingredients. Rapid expansion of café chains, bakery franchises, and dessert-focused foodservice outlets has further strengthened industrial demand for baking chocolate globally. Premium dessert culture is especially strong in North America, Europe, China, South Korea, and the Middle East, where consumers are willing to pay higher prices for luxury and indulgent bakery products. The growing influence of social media-driven food trends is also encouraging demand for visually appealing chocolate-based desserts.

Expansion of Home Baking and DIY Dessert Preparation

Home baking has become a mainstream consumer activity globally, significantly increasing retail demand for baking chocolate products. Consumers are increasingly purchasing chocolate chips, baking bars, cocoa ingredients, and ready-to-use chocolate fillings through supermarkets and online retail channels. Digital cooking tutorials, baking influencers, and social media recipe content have accelerated participation in household baking activities. The trend is particularly strong among younger demographics and urban households seeking personalized dessert experiences. Manufacturers are responding with smaller packaging formats, premium retail baking products, and easy-to-use chocolate solutions targeted at amateur bakers.

global market restraints

Volatility in Cocoa Bean Prices

The baking chocolate market remains highly vulnerable to fluctuations in cocoa bean prices, which significantly impact manufacturing costs and profitability. Cocoa production is concentrated in West African countries such as Côte d’Ivoire and Ghana, making global supply sensitive to climate variability, crop diseases, geopolitical risks, and labor-related issues. Sharp increases in cocoa prices directly affect chocolate manufacturers, especially small and medium-sized producers operating with limited pricing flexibility. Persistent raw material inflation can also reduce affordability for bakery manufacturers and retail consumers, limiting volume growth in price-sensitive markets.

Regulatory Pressure on Sugar and Sustainability Standards

Governments and regulatory agencies across Europe and North America are imposing stricter regulations related to sugar consumption, nutritional labeling, and sustainable sourcing practices. Manufacturers are increasingly required to reformulate products with reduced sugar content while maintaining taste and texture quality. In addition, concerns regarding deforestation, unethical labor practices, and environmental sustainability in cocoa farming are compelling companies to invest heavily in traceability systems and ethical sourcing programs. Compliance with sustainability certifications and environmental regulations is increasing operational costs across the global baking chocolate supply chain.

baking chocolate industry key opportunities

Expansion of Plant-Based and Functional Desserts

The rapid growth of plant-based foods and functional desserts is creating major opportunities for baking chocolate manufacturers. Vegan bakery products, dairy-free desserts, protein-enriched snacks, and reduced-sugar confectionery are becoming increasingly popular among health-conscious consumers. Manufacturers that develop innovative chocolate formulations using alternative sweeteners, functional ingredients, and plant-based dairy substitutes are expected to gain strong market traction. Premium dark chocolate products with high antioxidant positioning are also benefiting from growing consumer interest in wellness-oriented indulgence categories.

Growth of Emerging Market Café and Bakery Infrastructure

Rapid urbanization and rising disposable incomes in Asia-Pacific, Latin America, and the Middle East are accelerating investments in bakery cafés, premium dessert stores, and quick-service restaurant chains. Countries such as India, China, Indonesia, Vietnam, Saudi Arabia, and the UAE are witnessing strong growth in modern bakery retail formats, significantly increasing commercial demand for baking chocolate ingredients. International bakery brands are also expanding aggressively into emerging economies, creating long-term procurement opportunities for global chocolate manufacturers. Online ingredient retailing and food delivery platforms are further supporting demand growth across smaller urban markets.

Product Type Insights

Dark baking chocolate dominates the global baking chocolate market, accounting for nearly 34% of total demand, primarily driven by rising consumer preference for premium, high-cocoa-content products that offer rich flavor profiles and perceived health benefits. The growing popularity of antioxidant-rich dark chocolate among health-conscious consumers, coupled with increasing demand for indulgent premium desserts, continues to strengthen segment growth globally. Dark baking chocolate is extensively utilized across artisanal pastries, gourmet brownies, premium cookies, luxury cakes, and handcrafted confectionery products, particularly within upscale bakery and café chains seeking product differentiation and premium positioning. In addition, rising consumer willingness to pay higher prices for organic, ethically sourced, and high-quality chocolate ingredients is further accelerating demand for dark chocolate applications.Compound baking chocolate remains highly popular in cost-sensitive commercial bakery manufacturing due to its affordability, ease of handling, and lower dependency on tempering processes. Industrial food manufacturers continue to utilize compound chocolate extensively across mass-produced bakery products, frozen desserts, coatings, and snack applications to optimize production efficiency and reduce operational costs. The segment is particularly strong across emerging economies where manufacturers prioritize cost-effective ingredient solutions while maintaining product consistency.Meanwhile, vegan, sugar-free, and clean-label baking chocolate categories are emerging as some of the fastest-growing niches within the global market. Rising health awareness, increasing diabetic populations, growing demand for low-sugar diets, and expanding adoption of plant-based lifestyles are encouraging manufacturers to introduce dairy-free, organic, and naturally sweetened chocolate formulations. The increasing popularity of functional foods and healthier indulgence trends is expected to further accelerate innovation within these specialty product categories throughout the forecast period.

Application Insights

Bakery products represent the largest application segment within the global baking chocolate market, supported by consistently strong worldwide demand for cakes, pastries, muffins, cookies, brownies, croissants, dessert bars, and other chocolate-based baked goods. The dominance of the bakery segment is primarily driven by the rapid expansion of premium bakery chains, café franchises, and in-store bakery operations that increasingly utilize high-quality chocolate ingredients to enhance taste, texture, and visual appeal. Rising consumer preference for indulgent desserts, celebration cakes, and premium bakery snacks continues to fuel segment expansion across both developed and emerging markets. In addition, the growing popularity of artisanal baking and gourmet dessert culture is significantly increasing the consumption of premium baking chocolate products globally.Beverage applications including hot chocolate, mocha beverages, specialty coffees, milkshakes, and ready-to-drink chocolate beverages are witnessing rising popularity, particularly across urban café-driven markets. Increasing café culture penetration, rising coffee consumption, and growing demand for premium beverage experiences are supporting the integration of high-quality chocolate ingredients within beverage formulations.Snack applications such as protein bars, cereal snacks, granola bars, nutritional products, and chocolate-coated healthy snacks are emerging as rapidly expanding consumption categories worldwide. The growing demand for convenient on-the-go snacks, functional nutrition products, and protein-enriched food items is encouraging food manufacturers to incorporate baking chocolate into innovative snack formulations that combine indulgence with health-oriented positioning.

Distribution Channel Insights

Direct B2B sales dominate the global baking chocolate market due to long-term procurement relationships between chocolate manufacturers and large industrial bakery and confectionery producers. The leading position of the direct sales segment is driven by the need for consistent ingredient quality, stable pricing structures, customized formulations, and uninterrupted bulk supply for large-scale food manufacturing operations. Industrial bakery companies and multinational confectionery brands rely heavily on direct contractual agreements with chocolate suppliers to ensure production efficiency, product standardization, and supply chain reliability.Online retail is emerging as the fastest-growing distribution channel, supported by increasing home-baking participation, rising e-commerce penetration, and expanding digital grocery infrastructure globally. Consumers are increasingly purchasing premium baking ingredients through online platforms due to wider product availability, convenience, subscription-based delivery models, and access to specialty imported chocolate products. Direct-to-consumer brand websites and specialty baking ingredient platforms are further strengthening global accessibility for premium and niche chocolate offerings.

End-User Insights

Industrial food manufacturers account for the largest share of the global baking chocolate market due to extensive usage across packaged bakery, confectionery, snack, frozen dessert, and ready-to-eat food manufacturing operations. The dominance of this segment is primarily driven by rising global consumption of packaged baked goods and chocolate-based convenience foods, which require large-scale procurement of chocolate ingredients for automated production lines. Large manufacturers increasingly demand customized chocolate formulations that improve production efficiency, shelf stability, texture consistency, and flavor standardization across mass-market retail products.Foodservice operators including cafés, restaurants, hotels, dessert chains, and quick-service restaurant operators are increasingly incorporating premium chocolate desserts and bakery products into menus to improve customer engagement, menu innovation, and profit margins. The rapid expansion of café culture, premium dining experiences, and international dessert franchises is supporting greater utilization of high-quality baking chocolate ingredients across foodservice applications globally.Household consumers are also contributing significantly to overall market expansion due to rising participation in home baking, social media-driven baking trends, and growing interest in DIY dessert preparation activities. Consumers increasingly purchase baking chocolate products for homemade cakes, cookies, brownies, pastries, and festive desserts, particularly through online retail channels and modern supermarkets. The influence of digital cooking content, baking tutorials, and premium home baking kits is expected to further support segment growth during the forecast period.

| By Product Type | By Application | By Distribution Channel | By End User |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 27% of the global baking chocolate market, supported by strong demand from industrial bakery manufacturers, premium dessert brands, foodservice operators, and household baking consumers. The United States dominates regional consumption due to its large packaged bakery industry, strong café culture, high per-capita chocolate consumption, and extensive retail penetration of premium baking ingredients. Regional market growth is being driven by increasing consumer demand for premium desserts, dark chocolate products, organic cocoa ingredients, and clean-label bakery formulations. The growing popularity of home baking, coupled with the expansion of artisanal bakery chains and specialty dessert cafés, continues to stimulate market demand across the region. In addition, rising health consciousness is encouraging manufacturers to introduce sugar-free, vegan, and functional chocolate products that cater to evolving dietary preferences. Canada is also witnessing growing demand for ethically sourced and plant-based chocolate products, particularly across urban retail markets where consumers increasingly prioritize sustainability and premium ingredient quality.

Europe

Europe remains the largest regional market, contributing nearly 36% of global market share in 2025. Countries including Germany, Belgium, Switzerland, France, Italy, and the Netherlands are global leaders in chocolate manufacturing, cocoa processing, and bakery innovation. The region benefits from deeply established artisanal baking traditions, strong premium confectionery demand, advanced food manufacturing infrastructure, and high consumer spending on gourmet desserts and luxury bakery products. Regional growth is strongly supported by rising demand for sustainable cocoa sourcing, fair-trade certifications, organic chocolate products, and premium couverture chocolate applications. European consumers continue to demonstrate strong preference for high-quality chocolate ingredients with authentic flavor profiles and ethical sourcing transparency. Germany and Belgium remain major export hubs for premium baking chocolate ingredients, supported by their advanced chocolate production capabilities and strong international trade networks. In addition, the expansion of premium café chains, luxury hospitality establishments, and artisanal dessert boutiques continues to support long-term regional market growth.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and is expected to register a CAGR exceeding 10.5% during the forecast period. China, India, Japan, South Korea, Indonesia, Thailand, and other Southeast Asian countries are driving rapid regional demand growth through urbanization, rising disposable incomes, westernized dietary habits, and expanding bakery café culture. The strong growth of the regional market is primarily fueled by increasing middle-class spending on premium desserts, rapid expansion of organized bakery chains, and growing youth consumption of chocolate-based snacks and confectionery products. China remains the largest market within Asia-Pacific due to rising premium dessert consumption, increasing café penetration, and rapid growth of modern retail and e-commerce platforms. India is emerging as a major growth hub because of increasing bakery penetration, expanding foodservice infrastructure, rising demand for celebration cakes and confectionery products, and strong growth in urban consumer spending. Japan and South Korea continue to demonstrate strong demand for premium, artisanal, and aesthetically innovative chocolate applications, supported by mature café cultures and consumer preference for high-quality dessert products. The rapid expansion of international bakery franchises and premium dessert chains across Southeast Asia is also contributing significantly to regional market growth.

Latin America

Latin America is witnessing steady growth in baking chocolate demand, particularly across Brazil and Mexico, supported by rising urbanization, improving disposable incomes, and expanding consumer interest in premium bakery and confectionery products. Brazil benefits from strong domestic cocoa production, established food processing capabilities, and increasing dessert consumption across both retail and foodservice sectors. Mexico is experiencing growing demand from café chains, premium bakery outlets, and quick-service dessert operators as western-style bakery products gain popularity among urban consumers. Regional market growth is further supported by increasing investment in value-added chocolate applications, export-oriented bakery manufacturing, and modern retail expansion. Consumers across Latin America are increasingly adopting premium confectionery products, gourmet pastries, and indulgent dessert snacks, creating strong long-term opportunities for baking chocolate manufacturers.

Middle East & Africa

The Middle East & Africa region is emerging as a high-potential market for premium baking chocolate products due to rising disposable incomes, expanding hospitality infrastructure, and rapid urban foodservice development. The UAE and Saudi Arabia are leading regional demand growth through strong expansion of luxury hotels, premium cafés, international bakery franchises, and upscale dessert outlets. Increasing tourism activity and growing consumer preference for premium western-style desserts are significantly supporting baking chocolate consumption across the Gulf region. South Africa remains an important regional market due to its established bakery industry, modern retail infrastructure, and growing consumer demand for premium confectionery and dessert products. Regional growth is also being driven by increasing investments in organized retail, international foodservice brands, and café culture development across major urban centers. The rising popularity of gourmet pastries, imported chocolate ingredients, artisanal desserts, and premium celebration cakes is expected to further accelerate market expansion throughout the forecast period.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Baking Chocolate Market

- Barry Callebaut AG

- Cargill Incorporated

- Olam Food Ingredients

- Puratos Group

- Fuji Oil Holdings Inc.

- Blommer Chocolate Company

- Guittard Chocolate Company

- The Hershey Company

- Nestlé S.A.

- Mondelez International

- Valrhona

- Lindt & Sprüngli

- Meiji Holdings Co., Ltd.

- Aalst Chocolate Pte Ltd

- Ghirardelli Chocolate Company