Bakery Ingredients Market Size

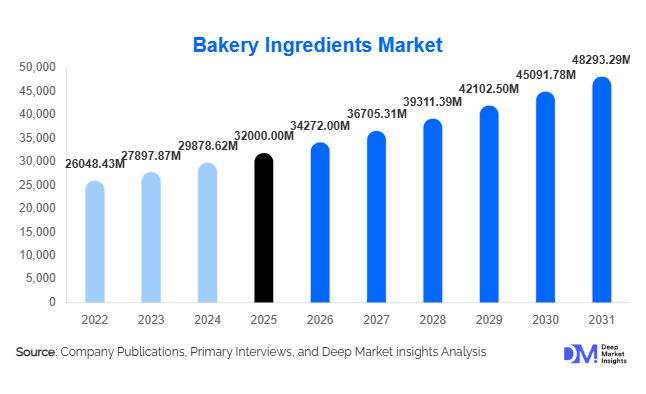

According to Deep Market Insights, the global bakery ingredients market size was valued at USD 32,000 million in 2026 and is projected to grow from USD 34,272 million in 2027 to reach USD 48,293.29 million by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). The bakery ingredients market growth is primarily driven by the rising consumption of packaged bakery products, increasing demand for clean-label and functional ingredients, and the rapid expansion of industrial and automated bakery production across both developed and emerging economies.

Key Market Insights

- Clean-label bakery formulations are becoming a global standard, driving strong demand for natural enzymes, emulsifiers, and plant-based ingredients.

- Industrial bakery expansion is accelerating, particularly in Asia-Pacific and Latin America, boosting bulk ingredient consumption.

- Europe dominates premium bakery ingredient demand, driven by strong artisanal bakery culture and strict regulatory standards.

- Asia-Pacific is the fastest-growing region, supported by urbanization, rising disposable income, and Western dietary influence.

- Functional bakery ingredients are gaining traction, including fiber enrichment, protein fortification, and sugar-reduction systems.

- Enzyme and fermentation technologies are transforming formulation science, improving efficiency and shelf life while reducing chemical additives.

What are the latest trends in the bakery ingredients market?

Clean-Label and Natural Ingredient Transformation

The bakery ingredients industry is undergoing a major transformation toward clean-label formulations, where consumers demand transparency and minimal chemical additives. Manufacturers are increasingly replacing synthetic emulsifiers, preservatives, and stabilizers with natural alternatives such as enzyme-based dough conditioners, plant-derived emulsifiers, and fermentation-based preservatives. This shift is particularly strong in Europe and North America, where regulatory pressure and health-conscious consumers are driving reformulation. Clean-label trends are also pushing innovation in starch modification and natural sweeteners, enabling manufacturers to maintain texture and taste while meeting evolving consumer expectations.

Functional and Health-Oriented Bakery Innovation

Health-focused consumption is reshaping product development across the bakery sector. Demand for gluten-free, high-protein, high-fiber, and low-sugar baked goods is accelerating, especially among urban consumers. This is creating opportunities for functional ingredient systems such as resistant starches, dietary fibers, protein isolates, and sugar substitutes like polyols. The integration of nutrition science into bakery formulation is enabling manufacturers to position bakery products as healthier everyday food options rather than indulgent items. This trend is also expanding into sports nutrition and diabetic-friendly bakery categories, creating new value pools.

What are the key drivers in the bakery ingredients market?

Rising Demand for Packaged and Industrial Bakery Products

The global shift toward convenience food consumption is a major driver of bakery ingredient demand. Urbanization, busy lifestyles, and the growth of organized retail have significantly increased demand for packaged bread, cakes, biscuits, and frozen bakery products. Industrial bakeries rely heavily on emulsifiers, enzymes, and preservatives to ensure consistency, shelf life, and mass production efficiency. The expansion of global QSR chains and café culture is further reinforcing demand for standardized bakery formulations across regions.

Technological Advancements in Ingredient Processing

Innovation in enzyme technology, fermentation systems, and bio-based ingredient production is enhancing bakery formulation efficiency. These advancements allow manufacturers to improve dough stability, reduce processing time, and eliminate synthetic additives. Microbial fermentation-based enzymes and functional starch systems are particularly important in enabling clean-label transformation. Technology adoption is also helping reduce production costs while improving scalability for industrial bakery operations.

Growth of Health-Conscious Consumption Patterns

Consumers are increasingly prioritizing health and wellness, leading to higher demand for fortified and functional bakery products. This includes high-fiber breads, protein-enriched snacks, and sugar-reduced baked goods. As a result, bakery ingredient manufacturers are investing in nutrition-based innovation, creating value-added ingredients that enhance both functionality and nutritional profile.

What are the restraints for the global market?

Volatility in Raw Material Prices

The bakery ingredients market is highly dependent on agricultural commodities such as wheat, sugar, dairy, and vegetable oils. Price fluctuations in these raw materials directly impact production costs and profit margins. Climate change, supply chain disruptions, and geopolitical instability further contribute to pricing volatility, making cost management a key challenge for manufacturers.

Stringent Regulatory and Compliance Requirements

The bakery ingredients industry faces strict regulatory oversight, particularly in developed markets such as Europe and North America. Regulations related to food safety, labeling transparency, and permissible additive limits can slow product innovation and increase compliance costs. Smaller manufacturers often struggle to meet evolving regulatory standards, limiting market entry and expansion.

What are the key opportunities in the bakery ingredients industry?

Expansion of Clean-Label and Organic Product Lines

The growing consumer shift toward natural and organic foods presents a strong opportunity for ingredient manufacturers. Companies investing in plant-based emulsifiers, natural preservatives, and fermentation-derived enzymes are well positioned to capture premium market segments. Organic bakery ingredients are gaining strong traction in developed economies, offering higher margins and strong brand differentiation.

Rapid Industrialization in Emerging Economies

Emerging markets such as India, China, Indonesia, and Brazil are witnessing rapid expansion of industrial bakeries and food processing industries. Government initiatives supporting food manufacturing infrastructure are increasing demand for scalable ingredient systems. This creates significant opportunities for global ingredient suppliers to establish regional production hubs and distribution networks.

Digitalization and Precision Formulation Technologies

The adoption of AI-driven formulation systems, predictive baking models, and digital supply chain platforms is transforming bakery ingredient optimization. These technologies help manufacturers develop customized ingredient blends for specific applications, improving efficiency and reducing waste. This digital shift is expected to redefine product development and supply chain management across the industry.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 32000.00 Million |

| Market Size in 2026 | USD 34272.00 Million |

| Market Size in 2031 | USD 48293.29 Million |

| CAGR | 7.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The bakery ingredients market is characterized by a highly diversified product landscape, where each ingredient category plays a distinct functional and commercial role in shaping product quality, texture, shelf life, and nutritional profile. Among these, emulsifiers continue to dominate the market, accounting for approximately 22% of the overall share. Their leadership is primarily driven by their indispensable role in stabilizing complex dough systems, improving aeration, enhancing softness, and extending the freshness of baked goods. Emulsifiers such as mono- and diglycerides, lecithin, and DATEM are extensively used across industrial bakery operations because they ensure consistent product quality even under large-scale, high-speed production environments. The leading growth driver for emulsifiers is the rising demand for processed and packaged bakery products that require extended shelf life without compromising sensory attributes, especially in urban retail and export-oriented supply chains.Starches also play a foundational role in bakery ingredient systems, particularly in applications requiring moisture retention, texture enhancement, and structural consistency. Modified starches are widely used in cakes, breads, and frozen bakery products where freeze-thaw stability is critical. The key driver for starch demand is the expansion of convenience and frozen bakery categories, where product stability over extended storage and transportation cycles is essential. Sweeteners, both nutritive and non-nutritive, remain essential for taste modulation and browning reactions in baked goods. However, their market dynamics are increasingly influenced by sugar reduction initiatives and health-driven reformulations, making low-calorie and natural sweeteners a rapidly evolving sub-segment.Fats and shortenings continue to be vital for providing richness, mouthfeel, and structural integrity in bakery formulations. Although their growth is relatively mature in developed markets, demand remains strong in emerging economies where bakery consumption is expanding. The leading driver for fats and shortenings is product indulgence positioning, particularly in cakes, pastries, and laminated dough products. Meanwhile, fibers and functional ingredients represent the fastest-growing category within the product type segment. This growth is strongly driven by increasing consumer awareness of digestive health, obesity management, and the rising demand for fortified bakery products that offer added nutritional benefits such as protein enrichment, dietary fiber enhancement, and micronutrient fortification.

Application Insights

The application landscape of bakery ingredients is broad and continuously evolving, with bread remaining the most dominant segment globally. Bread accounts for the largest consumption of bakery ingredients due to its status as a staple food across both developed and emerging economies. The leading driver for this dominance is the consistent daily consumption pattern of bread products, combined with large-scale industrial production systems that require standardized ingredient solutions to maintain quality and efficiency across global supply chains.Cakes and pastries represent a high-value application segment, driven by premiumization trends and increasing consumer inclination toward indulgent and celebratory food experiences. The primary growth driver for this segment is rising disposable income and changing lifestyle patterns, particularly in urban centers where bakery products are increasingly associated with luxury, gifting, and special occasions. Cookies and biscuits also maintain strong global demand due to their affordability, long shelf life, and convenience, making them a preferred snacking option across age groups and income levels. Their leading driver is the expansion of retail distribution channels and increasing penetration of packaged snack foods.Frozen bakery products are emerging as one of the fastest-growing application areas, supported by the rapid expansion of modern retail infrastructure, quick-service restaurants, and convenience-driven consumption habits. The leading driver in this segment is the increasing demand for ready-to-bake and ready-to-eat products that reduce preparation time while maintaining freshness and quality. Specialty bakery applications, including gluten-free, vegan, organic, and fortified products, are witnessing significant innovation activity. The primary driver for these niche categories is the global shift toward health-conscious consumption and dietary customization, which is reshaping product development strategies across bakery manufacturers worldwide.

Distribution Channel Insights

The distribution structure of bakery ingredients is heavily influenced by industrial supply chain dynamics and the scale of production requirements. Direct B2B sales dominate the market, as large industrial bakeries and food manufacturers prefer long-term supply agreements with ingredient producers to ensure consistency, cost efficiency, and customized formulations. The leading driver for this channel is the need for operational reliability and quality standardization in high-volume production environments, where ingredient performance directly impacts product consistency.Distributors and ingredient wholesalers play a crucial role in bridging the gap between manufacturers and mid-sized bakery businesses, particularly in emerging markets where fragmented supply chains require intermediaries for efficient distribution. Their growth is driven by expanding regional bakery industries and increasing demand for diversified ingredient portfolios across small and medium enterprises. Online B2B platforms are gaining momentum as digital procurement becomes more prevalent in the food ingredients industry. The primary driver for this shift is the need for pricing transparency, faster procurement cycles, and easier access to global suppliers, especially for smaller bakery operators seeking competitive sourcing options.Strategic partnerships between ingredient manufacturers and large bakery chains are also becoming increasingly significant. These collaborations are driven by the need for customized ingredient systems tailored to specific product lines, enabling manufacturers to secure stable, long-term demand while allowing bakery chains to differentiate their offerings in highly competitive retail environments.

End-Use Insights

Industrial bakeries represent the largest end-use segment in the bakery ingredients market, driven by their high-volume production capabilities and reliance on standardized, efficient ingredient systems. The leading driver for this segment is the globalization of packaged food supply chains, which requires consistent product quality across multiple geographies and retail formats. Industrial bakeries depend heavily on emulsifiers, enzymes, and functional blends to achieve scalability and uniformity.Artisanal bakeries are experiencing steady growth, fueled by consumer demand for fresh, premium, and locally crafted bakery products. The key driver for this segment is the rising preference for authenticity, craftsmanship, and clean-label formulations, which has encouraged smaller bakeries to adopt high-quality natural ingredients. The HoReCa sector also contributes significantly to market demand, particularly in urban and tourism-driven economies where cafes, hotels, and restaurants integrate bakery items into diversified menus. The leading driver here is the expansion of foodservice culture and experiential dining trends.Food manufacturers are increasingly incorporating bakery ingredients into cross-category applications such as breakfast bars, meal replacements, protein snacks, and ready-to-eat convenience foods. This diversification is driven by the growing demand for multifunctional food products that combine nutrition, convenience, and indulgence, expanding the scope of bakery ingredients beyond traditional baked goods.

Explore more data points, trends and opportunities Download Free Sample Report

Bakery Ingredients Market Segmentations

By Ingredient Type

- Enzymes

- Emulsifiers

- Leavening Agents

- Dough Conditioners

- Starches

- Sweeteners

- Fats & Shortenings

- Preservatives

- Flavors & Colorants

- Fibers & Functional Ingredients

By Form

- Dry

- Powder

- Liquid

- Semi-solid / Paste

By Source

- Natural Ingredients

- Synthetic Ingredients

- Bio-based

- Fermentation-derived Ingredients

By Application

- Bread

- Cakes & Pastries

- Cookies & Biscuits

- Frozen Bakery Products

- Pizza & Dough Bases

- Specialty Bakery Products

By End-Use

- Industrial Bakeries

- Artisanal & In-store Bakeries

- HoReCa

- Food Manufacturers & Private Labels

Regional Insights

Europe

Europe holds the largest share of the global bakery ingredients market, accounting for approximately 32% of total demand. The region’s leadership is strongly supported by its deep-rooted bakery culture, particularly in countries such as Germany, France, Italy, and the United Kingdom, where bread, pastries, and artisanal baked goods form an integral part of daily consumption. The primary driver of regional growth is the strong consumer preference for high-quality, clean-label, and natural ingredients, reinforced by stringent food safety and labeling regulations. Additionally, Europe leads in technological innovation in enzyme systems, fermentation technologies, and plant-based emulsifier development, further strengthening its market dominance. Increasing demand for premium bakery products and the rise of health-conscious consumers are also accelerating the adoption of functional bakery ingredients across the region.

North America

North America accounts for approximately 28% of the global market and is characterized by highly industrialized bakery production systems and strong retail penetration. The United States and Canada dominate regional demand, driven by large-scale packaged food consumption and the expansion of quick-service restaurant chains. The leading driver in this region is the increasing demand for functional and health-oriented bakery products, including protein-enriched, low-sugar, and high-fiber formulations. Additionally, technological advancements in food processing and strong R&D investment by ingredient manufacturers continue to support innovation in clean-label and performance-enhancing bakery ingredients.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, contributing approximately 30% of global demand. Rapid urbanization, rising disposable incomes, and changing dietary habits are key factors fueling market expansion in countries such as China, India, Japan, and Australia. The leading driver for regional growth is the increasing influence of Western dietary patterns, which has significantly boosted demand for packaged bakery products in urban centers. Expansion of modern retail infrastructure, growing café culture, and rising youth consumption are also contributing to strong market momentum. Additionally, increasing investments in industrial bakery manufacturing are enabling large-scale production and distribution of bakery products across emerging economies.

Latin America

Latin America is witnessing steady growth in bakery ingredient consumption, led by Brazil and Mexico. The region’s growth is primarily driven by the expansion of industrial bakery operations and increasing demand for affordable packaged foods. The leading driver is urban population growth combined with rising middle-class consumption, which is expanding the retail bakery sector. Additionally, gradual adoption of fortified and functional bakery products is creating new growth opportunities, particularly in health-conscious urban markets.

Middle East & Africa

The Middle East & Africa region is emerging as a promising growth market due to rapid urbanization, population growth, and expanding tourism and hospitality sectors. Gulf countries such as the UAE and Saudi Arabia are key demand centers for premium bakery products, driven by high expatriate populations and strong foodservice infrastructure. The leading driver in this region is the expansion of hospitality-driven consumption and increasing reliance on imported food ingredients. In Africa, rising industrial bakery development supported by urban population growth and improving retail infrastructure is gradually strengthening regional demand for bakery ingredients.

Key Players in the Bakery Ingredients Market

- Cargill Inc.

- Archer Daniels Midland (ADM)

- International Flavors & Fragrances (IFF)

- Kerry Group

- DSM-Firmenich

- Ingredion Incorporated

- Tate & Lyle

- Corbion N.V.

- Puratos Group

- Lesaffre Group

- Lallemand Inc.

- AB Mauri

- Novonesis

- Givaudan

- Dawn Foods