Bakery Inclusions Market Size

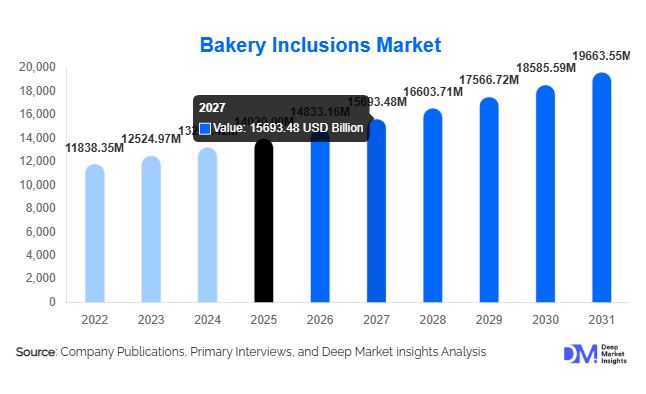

According to Deep Market Insights, the global bakery inclusions market size was valued at USD 14,020 million in 2025 and is projected to grow from USD 14,833.16 million in 2026 to reach USD 19,663.55 million by 2031, expanding at a CAGR of 5.8% during the forecast period (2026–2031). The bakery inclusions market growth is primarily driven by premiumization in baked goods, rising demand for indulgent and clean-label ingredients, and expanding industrial bakery production across emerging economies. Increasing consumption of cookies, muffins, cakes, and artisanal breads containing chocolate chips, fruit pieces, nuts, and seeds continues to strengthen global demand.

Key Market Insights

- Chocolate inclusions dominate the global market, accounting for nearly 34% of total revenue share in 2025, supported by strong cookie and muffin consumption worldwide.

- Commercial bakeries represent over 60% of end-use demand, driven by large-scale industrial procurement and standardized recipes.

- North America leads the global market with approximately 32% share in 2025, owing to high per capita bakery consumption and premium product adoption.

- Asia-Pacific is the fastest-growing region, expanding at over 7% CAGR due to urbanization and rising packaged bakery demand in China and India.

- B2B distribution accounts for over 70% of total sales, reflecting strong reliance on industrial bakeries and QSR chains.

- Heat-stable chocolate and moisture-controlled fruit inclusions are emerging as key technological innovations enhancing product stability.

What are the latest trends in the bakery inclusions market?

Clean-Label and Functional Ingredient Innovation

Consumers are increasingly demanding bakery products made with natural, organic, and minimally processed ingredients. This trend is accelerating the adoption of clean-label fruit pieces, plant-based chocolate inclusions, and non-GMO nut segments. Manufacturers are investing in freeze-drying technologies, natural preservation techniques, and reduced-sugar formulations to meet evolving regulatory and consumer expectations. Functional inclusions enriched with protein, fiber, probiotics, and superfoods such as chia and flax are gaining traction, particularly in North America and Europe. This convergence of indulgence and health is reshaping bakery innovation pipelines globally.

Premiumization and Artisanal Product Growth

Premium bakery products featuring gourmet chocolate chunks, exotic fruit blends, and specialty seeds are expanding shelf presence across supermarkets and specialty stores. Artisanal bakeries are leveraging high-quality inclusions to differentiate offerings and command premium pricing. Social media-driven baking culture and visually appealing inclusions such as colored sugar crystals and decorative shavings are enhancing product aesthetics, further stimulating demand. This trend is especially strong in Europe and North America, where consumers prioritize texture, flavor complexity, and authenticity.

What are the key drivers in the bakery inclusions market?

Expansion of Industrial and Commercial Bakeries

The rapid growth of organized retail and quick-service restaurant (QSR) chains has strengthened industrial bakery production globally. Commercial bakeries account for nearly 61% of overall inclusion demand, driven by standardized recipes and bulk procurement models. Growing urban populations and increased consumption of packaged bakery snacks in Asia-Pacific are reinforcing large-scale inclusion usage.

Rising Snacking Culture and Convenience Demand

Global snacking trends are driving strong consumption of cookies, biscuits, muffins, and breakfast bakery products. Cookies and biscuits alone account for approximately 29% of inclusion applications worldwide. Busy lifestyles and demand for on-the-go products are boosting bakery snack innovation, directly increasing inclusion volumes per unit product.

Health-Oriented Reformulations

Manufacturers are incorporating nuts, seeds, and fruit inclusions to enhance perceived nutritional value. The inclusion of protein-enriched and fiber-rich ingredients aligns with wellness-focused consumer preferences. This driver is particularly visible in North America and Western Europe, where better-for-you bakery options are gaining shelf space.

What are the restraints for the global market?

Volatility in Raw Material Prices

Cocoa, sugar, dairy, and nut prices are subject to global commodity fluctuations. Cocoa price volatility significantly impacts chocolate inclusion costs, affecting manufacturer margins and pricing stability. Sudden supply disruptions in producing regions can further amplify cost pressures.

Technical and Shelf-Life Challenges

Moisture migration from fruit inclusions and heat sensitivity of chocolate components can compromise bakery shelf life. Advanced stabilization technologies increase production costs, posing operational challenges for small and mid-sized manufacturers.

What are the key opportunities in the bakery inclusions industry?

Emerging Market Penetration

Asia-Pacific and Latin America present high-growth opportunities as middle-class incomes rise and Western-style bakery consumption increases. Establishing local manufacturing facilities can reduce logistics costs and enhance market responsiveness. India and Southeast Asia are witnessing strong growth in packaged bakery demand, creating significant inclusion sourcing potential.

Customization and Technology Integration

Technological advancements such as heat-resistant chocolate, controlled particle sizing, and sugar-reduced confectionery bits enable tailored solutions for bakery manufacturers. Customized inclusion blends designed for specific baking temperatures and product textures are strengthening supplier–client partnerships and long-term contracts.

Product Type Insights

Chocolate inclusions continue to dominate the global bakery inclusions market, accounting for approximately 34% of total revenue share in 2025. The segment’s leadership is primarily driven by strong and consistent demand across cookies, muffins, brownies, and premium cake applications. Consumer preference for indulgent, cocoa-rich flavors, combined with the rising popularity of premium and artisanal baked goods, supports sustained growth. Additionally, innovation in dark, sugar-reduced, and sustainably sourced chocolate inclusions is strengthening appeal among health-conscious and ethically aware consumers. Fruit inclusions represent the second-largest segment, benefiting from clean-label positioning, natural flavor enhancement, and premium pastry applications. The growing demand for organic, freeze-dried, and low-sugar fruit variants further supports segment expansion. Nut and seed inclusions are gaining traction due to increasing demand for protein-rich, high-fiber, and functional bakery products. Rising awareness of plant-based nutrition and healthy snacking trends is accelerating their adoption. Dairy-based and confectionery inclusions maintain steady demand, particularly in decorative, filled, and indulgent baked goods, where texture contrast and flavor layering are critical product attributes.

Form Insights

Solid pieces such as chips, chunks, flakes, and nut fragments account for nearly 41% of total market share in 2025, making them the leading form segment. Their dominance is largely driven by superior visual appeal, enhanced texture, portion control efficiency, and ease of standardized dosing in automated production lines. Industrial bakeries prefer solid inclusions due to minimal processing complexity and consistent baking performance under high-temperature conditions. Pastes and fillings are witnessing steady growth, particularly in premium pastries, croissants, and filled cakes across Europe and North America. Their growth is supported by rising demand for multi-layered desserts, customized flavor combinations, and value-added bakery offerings. Additionally, advancements in heat-stable and low-sugar filling formulations are improving shelf life and product stability, further enhancing adoption.

Application Insights

Cookies and biscuits dominate application demand with nearly 29% share in 2025, supported by the global snacking culture and rising consumption of convenient, packaged baked goods. The segment’s leadership is driven by high inclusion loading capacity, flavor customization flexibility, and strong retail penetration. Premiumization trends, including double-chocolate, fruit-filled, and protein-enriched variants, continue to drive higher inclusion usage per unit. Cakes and pastries follow closely, fueled by premium dessert consumption, celebration culture, and café-style bakery expansion. Bread and rolls increasingly incorporate seeds, whole grains, and specialty inclusions to cater to functional and health-oriented consumers. Growth in fortified, multigrain, and plant-based bread categories is further strengthening inclusion demand within this segment.

Distribution Channel Insights

The B2B channel accounts for approximately 72% of total market revenue, reflecting the dominance of industrial and commercial bakery procurement models. Large-scale bakeries secure inclusions through long-term supply agreements to ensure pricing stability, consistent quality, and uninterrupted supply chains. The scale of packaged bakery production globally continues to reinforce B2B channel strength. Meanwhile, retail channels are expanding steadily, supported by rising home baking trends, increased consumer experimentation, and the growth of specialty ingredient sales via e-commerce platforms. Digital grocery platforms and direct-to-consumer ingredient brands are further improving accessibility to premium inclusion products.

End-Use Insights

Commercial bakeries hold around 61% of overall demand, supported by industrial-scale production, private-label manufacturing, and large retail distribution networks. The segment’s leadership is driven by high-volume output, standardized formulations, and increasing demand for packaged bakery goods across supermarkets and convenience stores. Artisanal bakeries are growing at a faster CAGR of 6–7%, particularly in Europe and North America, where consumers prioritize freshness, clean-label ingredients, and premium handcrafted products. Foodservice chains and quick-service restaurant bakery menus are expanding rapidly in Asia-Pacific, increasing demand for customized inclusions in muffins, dessert buns, and specialty baked snacks. The expansion of café chains and in-store bakery formats further strengthens institutional consumption.

| By Product Type | By Form | By Application | By Distribution Channel | By End-Use Industry |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America leads the global bakery inclusions market with approximately 32% share in 2025. The United States dominates regional demand due to high per capita consumption of cookies, brownies, and muffins, alongside a well-established industrial bakery infrastructure. Strong presence of large packaged food manufacturers, continuous product innovation, and premium dessert trends further support market expansion. Growth is also driven by rising demand for clean-label, gluten-free, and protein-enriched baked goods. Canada contributes steady growth through artisanal bakery expansion, organic ingredient adoption, and increasing multicultural flavor influences. Advanced cold chain logistics and strong retail penetration provide additional structural support for sustained regional growth.

Europe

Europe accounts for nearly 28% of global revenue share, led by Germany, France, Italy, and the UK. The region’s strong artisanal baking heritage drives consistent demand for fruit, nut, and specialty inclusions. Growth is supported by premium patisserie culture, increasing demand for organic and sustainably sourced ingredients, and strict food quality regulations that encourage high-value inclusion usage. Clean-label preferences, reduced-sugar reformulation initiatives, and plant-based bakery innovation are accelerating segment expansion. Additionally, sustainability certifications and ethical cocoa sourcing play a critical role in purchasing decisions, particularly in Western Europe. Eastern Europe is emerging as a growth pocket due to rising disposable income and expanding supermarket bakery sections.

Asia-Pacific

Asia-Pacific represents the fastest-growing region, expanding at over 7% CAGR. Rapid urbanization, rising middle-class income, and increasing westernization of diets are major growth drivers. China leads in production scale and packaged bakery output, supported by expanding domestic bakery chains and strong e-commerce penetration. India is one of the fastest-growing consumption markets, driven by increasing demand for affordable packaged snacks, urban café culture expansion, and growing youth demographics. Japan and Australia maintain stable demand for premium and functional bakery products, while Southeast Asian markets are witnessing rising demand for chocolate and fruit inclusions in convenience bakery items. Expanding modern retail infrastructure and growing investment in food processing capacity further strengthen regional growth prospects.

Latin America

Brazil and Mexico are the primary markets in Latin America, supported by strong demand for packaged bread, sweet bakery products, and filled snacks. Growth is driven by expanding supermarket penetration, increasing private-label bakery production, and rising consumer preference for indulgent yet affordable treats. Urbanization and improving distribution networks are enhancing inclusion accessibility across mid-sized cities. Additionally, regional flavor preferences, including chocolate and tropical fruit variants, are encouraging localized product innovation.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth, supported by expanding industrial bakery capacity and premium product imports. The UAE and Saudi Arabia lead Middle Eastern demand due to strong presence of premium bakery chains, high expatriate populations, and growing café culture. Rising tourism and hospitality sector expansion further stimulate demand for decorative and premium inclusions. In Africa, South Africa dominates regional demand, supported by organized retail growth and increasing investment in packaged bakery manufacturing. Gradual urbanization, improving cold storage infrastructure, and rising disposable income levels are expected to create additional growth opportunities across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Bakery Inclusions Market

- Barry Callebaut

- Cargill Incorporated

- ADM

- Puratos

- Dawn Foods

- Tate & Lyle

- Sensient Technologies

- Kerry Group

- Olam Food Ingredients

- Taura Natural Ingredients

- TreeHouse Foods

- Griffith Foods

- AGRANA Beteiligungs-AG

- AAK AB

- Ingredion Incorporated