B2B Chocolate Market Size

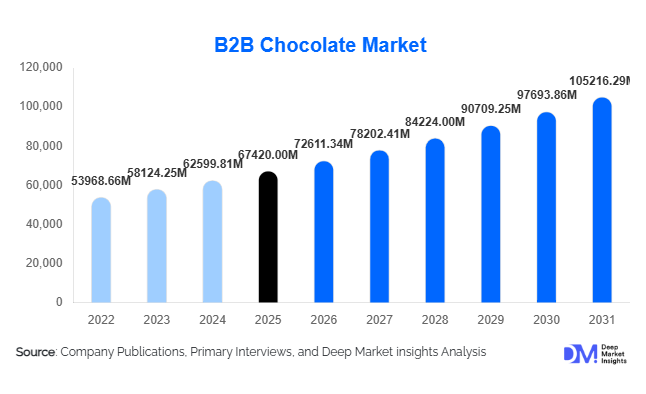

According to Deep Market Insights, the global B2B chocolate market size was valued at USD 67,420 million in 2025 and is projected to grow from USD 72,611.34 million in 2026 to reach USD 105,216.29 million by 2031, expanding at a CAGR of 7.7% during the forecast period (2026–2031). The B2B chocolate market represents the industrial supply chain of chocolate ingredients supplied to food manufacturers, bakeries, confectionery producers, dairy processors, and foodservice operators worldwide. Market growth is driven by increasing demand for premium confectionery, rising bakery consumption, rapid expansion of quick-service restaurants, and growing industrial use of chocolate across snacks, beverages, and desserts.

Key Market Insights

- Industrial chocolate demand is shifting toward premium and sustainable sourcing, with manufacturers adopting certified cocoa and traceable supply chains.

- Compound and couverture chocolate usage is expanding rapidly due to scalability and cost optimization for large-scale food manufacturing.

- Asia-Pacific is emerging as the fastest-growing consumption hub, driven by urbanization and Westernized dietary preferences.

- Private-label and contract manufacturing growth is increasing B2B procurement volumes across bakery and snack categories.

- Automation and smart processing technologies are improving consistency, yield efficiency, and production scalability.

- Foodservice and QSR dessert innovation continues to create stable institutional demand for industrial chocolate inputs.

What are the latest trends in the B2B chocolate market?

Premiumization and Single-Origin Chocolate Demand

Industrial buyers are increasingly sourcing premium couverture and single-origin chocolate to differentiate finished products. Food manufacturers are using origin-specific cocoa profiles to enhance flavor storytelling and brand positioning. Premium chocolate is no longer restricted to luxury confectionery; bakery chains, ice cream brands, and beverage manufacturers are integrating higher cocoa-content formulations. This transition is supported by consumer willingness to pay more for ethically sourced and high-quality chocolate products. Certifications such as Rainforest Alliance and Fairtrade are influencing procurement decisions across multinational food processors.

Functional and Reduced-Sugar Chocolate Innovation

Health-conscious consumption patterns are reshaping industrial chocolate formulations. Manufacturers are introducing reduced-sugar, plant-based, and protein-enriched chocolate variants suitable for snacks, nutrition bars, and dairy alternatives. Sugar reduction technologies, alternative sweeteners, and cocoa intensity optimization are allowing B2B suppliers to maintain taste profiles while meeting regulatory and consumer expectations. Functional chocolate ingredients enriched with fiber, probiotics, or adaptogens are gaining adoption in premium snack manufacturing.

What are the key drivers in the B2B chocolate market?

Expansion of Global Bakery and Confectionery Manufacturing

The rapid expansion of industrial bakery and packaged confectionery production is a primary driver of B2B chocolate demand. Industrial bakeries require stable chocolate inputs for fillings, coatings, inclusions, and decorations. Growth of packaged baked goods across emerging markets has significantly increased bulk chocolate procurement volumes.

Growth of Quick-Service Restaurants and Dessert Chains

Global QSR expansion has created steady institutional demand for chocolate syrups, chips, and compounds used in beverages and desserts. International café chains and dessert franchises increasingly rely on standardized chocolate sourcing contracts, ensuring long-term B2B supply agreements.

Rising Demand for Convenience Snacks

Chocolate-coated snacks, cereal bars, biscuits, and ready-to-eat desserts are expanding rapidly worldwide. Snack manufacturers increasingly utilize compound chocolate due to longer shelf life and cost efficiency, supporting large-scale adoption across emerging economies.

What are the restraints for the global market?

Cocoa Price Volatility

Fluctuating cocoa prices driven by climate variability and supply disruptions in West Africa significantly impact production costs. Industrial buyers face margin pressure, forcing reformulation strategies and long-term hedging contracts.

Sustainability Compliance Costs

Traceability requirements, deforestation regulations, and ethical sourcing standards increase operational complexity and procurement expenses for manufacturers. Smaller processors face challenges meeting evolving sustainability benchmarks.

What are the key opportunities in the B2B chocolate industry?

Emerging Market Industrialization

Rapid food manufacturing expansion in Southeast Asia, India, and Latin America offers significant opportunities for B2B chocolate suppliers. Localized production facilities reduce logistics costs while supporting regional flavor customization.

Plant-Based and Dairy-Free Applications

The growth of vegan confectionery and dairy alternatives is opening new demand channels for cocoa-based formulations without milk solids. Industrial chocolate manufacturers investing in plant-based innovation can capture expanding alternative protein markets.

Automation and Smart Manufacturing Integration

Digitalized chocolate processing, AI-driven quality control, and energy-efficient tempering technologies are improving yield efficiency and reducing waste. Suppliers offering customized industrial solutions gain competitive advantages through operational partnerships with food manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 67420 Million |

| Market Size in 2026 | USD 72611.34 Million |

| Market Size in 2031 | USD 105216.29 Million |

| CAGR | 7.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global B2B chocolate market demonstrates strong segmentation across product types, with couverture chocolate emerging as the dominant category, accounting for approximately 34% of the global market share in 2025. The leadership of couverture chocolate is fundamentally linked to its high cocoa butter content, superior viscosity control, and excellent tempering characteristics, which are essential for premium confectionery and high-end bakery manufacturing. Industrial confectioners increasingly prioritize consistency, gloss, snap quality, and flavor release-technical attributes that couverture chocolate delivers more effectively than standard chocolate formulations. As global consumers continue shifting toward premium indulgence and artisanal-quality products, manufacturers are upgrading ingredient standards, directly reinforcing couverture chocolate demand across large-scale production environments.Premiumization trends in developed markets such as Europe and North America, combined with rising aspirational consumption in emerging economies, have encouraged food manufacturers to incorporate higher-quality chocolate bases into their product portfolios. The growing popularity of filled pralines, molded chocolates, enrobed snacks, and luxury desserts has significantly expanded industrial procurement volumes. Additionally, technological improvements in cocoa butter fractionation and controlled crystallization processes have improved manufacturing efficiency, enabling couverture chocolate to scale beyond niche premium applications into broader industrial usage.Compound chocolate represents the second-largest product category and continues to play a critical role in cost-sensitive applications. Unlike couverture chocolate, compound chocolate replaces cocoa butter partially or entirely with vegetable fats, allowing manufacturers to achieve price stability while maintaining desirable texture and flavor properties. Its resistance to temperature fluctuations and simplified processing requirements make it particularly suitable for large-scale snack coatings, bakery fillings, biscuits, and molded confectionery produced in warm-climate regions. The rapid expansion of mass-market packaged foods in Asia-Pacific, Latin America, and parts of Africa strongly supports compound chocolate adoption, as manufacturers balance quality expectations with operational cost management.Overall, the leading segment driver across product types remains the global shift toward premium yet scalable chocolate applications, where manufacturers seek ingredients that deliver both sensory quality and operational efficiency. Continuous innovation in cocoa processing, fat composition engineering, and flavor customization is expected to further strengthen product diversification and sustain long-term growth within the B2B chocolate market.

Application Insights

Confectionery manufacturing remains the largest application segment in the global B2B chocolate market, accounting for nearly 38% of total demand in 2025. This dominance is driven by sustained consumer demand for chocolate-based indulgence products, seasonal gifting traditions, and continuous innovation in filled chocolates, pralines, truffles, and molded confectionery. Industrial confectionery producers rely heavily on bulk chocolate sourcing to ensure consistency in taste, texture, and production efficiency across large volumes. Increasing product launches centered on premium flavors, reduced sugar formulations, and functional ingredients are further expanding procurement requirements.The leading driver for this segment is the rapid evolution of global confectionery innovation cycles. Manufacturers frequently introduce limited-edition flavors, regionally inspired variants, and personalized chocolate formats to maintain consumer engagement. Such innovation requires stable ingredient supply chains, encouraging long-term partnerships between chocolate producers and confectionery manufacturers. Automation within confectionery plants has also increased throughput capacity, further elevating ingredient consumption levels.Bakery applications represent one of the fastest-expanding segments, supported by the industrialization of bread, pastry, and dessert production worldwide. Chocolate is increasingly used in croissants, muffins, cakes, cookies, donuts, and filled pastries as bakery chains expand globally. Urbanization and changing consumption patterns have accelerated demand for convenient bakery snacks, encouraging manufacturers to integrate chocolate as both a flavor and value-enhancing ingredient. Industrial bakeries increasingly favor ready-to-use chocolate formats that reduce preparation time and improve consistency across production batches.Dairy and frozen dessert applications are gaining notable traction due to innovation in premium ice creams, flavored milk beverages, yogurt desserts, and hybrid dairy-confectionery products. Chocolate-based coatings, ripples, and inclusions enhance sensory appeal while enabling product differentiation in highly competitive dairy markets. The expansion of premium ice cream brands and the rising popularity of indulgent desserts among younger consumers continue to strengthen demand from this segment.Foodservice and beverage applications are also expanding, particularly as cafés and quick-service restaurants introduce chocolate-based drinks, desserts, and seasonal menu offerings. The convergence of beverage culture and dessert innovation has created new demand streams for industrial chocolate suppliers. Overall, application growth is strongly influenced by evolving consumer indulgence trends combined with industrial-scale food innovation.

Distribution Channel Insights

Distribution within the B2B chocolate market is primarily dominated by direct industrial contracts, contributing more than 55% of global transactions. Large food manufacturers increasingly prefer direct sourcing agreements with chocolate producers to ensure price stability, consistent quality, and secure long-term supply. These contractual relationships allow manufacturers to mitigate cocoa price volatility while enabling suppliers to plan production capacity efficiently. Integrated supply agreements also facilitate collaborative product development, where chocolate formulations are customized to meet specific processing or sensory requirements.The leading driver for this segment is supply chain reliability. As chocolate serves as a critical input ingredient rather than a finished product, production interruptions can significantly impact downstream manufacturing operations. Consequently, multinational food companies prioritize dependable procurement partnerships supported by logistics integration and quality assurance systems.Specialized ingredient distributors continue to play a vital role in serving mid-sized and regional manufacturers that require flexible order volumes and technical support. These distributors often provide formulation guidance, application testing, and localized warehousing solutions, enabling smaller processors to access premium chocolate products without maintaining extensive procurement infrastructure.Digital B2B procurement platforms are emerging as transformative distribution channels. Online sourcing ecosystems enable smaller manufacturers and artisanal producers to compare suppliers, access transparent pricing, and streamline ordering processes. Digitalization is improving supply chain efficiency while expanding market accessibility, particularly in emerging economies where traditional distribution networks remain fragmented.

Form Insights

Liquid chocolate leads the market by form, accounting for nearly 41% of total market share, primarily due to its compatibility with automated production systems. Industrial manufacturers increasingly favor liquid chocolate because it eliminates melting stages, reduces processing time, and ensures uniform viscosity during manufacturing. Continuous production lines in confectionery and bakery facilities benefit significantly from liquid chocolate’s operational efficiency, allowing higher throughput and reduced labor costs.The primary driver behind liquid chocolate dominance is manufacturing optimization. As food producers invest heavily in automation and smart factory technologies, ingredients that integrate seamlessly into automated systems gain competitive advantage. Liquid chocolate supports precise dosing, improved hygiene control, and minimized material waste, making it highly attractive for large-scale industrial operations.Solid chocolate blocks remain widely used by artisanal producers and mid-scale manufacturers who require formulation flexibility. Blocks allow customized melting, blending, and flavor adjustments, supporting niche product innovation and small-batch production. Despite slower growth compared to liquid formats, solid chocolate maintains relevance across specialty confectionery segments.Chocolate chips and drops represent the fastest-growing form category, driven by global bakery innovation and snack product diversification. Their standardized shape enables consistent baking performance, while their convenience reduces preparation complexity. Growth in packaged cookies, muffins, breakfast bars, and ready-to-bake products continues to expand demand for this segment.

End-Use Industry Insights

Industrial food manufacturers constitute the largest end-use industry, contributing approximately 52% of total demand. These companies rely on bulk chocolate sourcing to support large-scale production of confectionery, baked goods, dairy desserts, and snack foods distributed across global retail networks. Increasing consolidation within the food manufacturing sector has amplified procurement volumes, as multinational brands centralize ingredient sourcing strategies.The leading driver for this segment is large-scale food industrialization combined with global brand expansion. Manufacturers continuously scale production capacities to meet rising consumption levels in emerging markets while maintaining consistent product quality worldwide.Quick-service restaurants and café chains represent one of the fastest-growing end-use categories. Expansion of dessert-focused menus, specialty beverages, and seasonal offerings has increased demand for ready-to-use chocolate solutions. Chocolate-based beverages, brownies, pastries, and dessert toppings have become essential menu components for modern café culture, particularly in urban markets.Export-oriented confectionery hubs across Europe and Asia are also increasing procurement volumes. Manufacturers in these regions produce chocolate-based products for international markets, reinforcing cross-border trade flows and strengthening the global B2B chocolate supply ecosystem.

Explore more data points, trends and opportunities Download Free Sample Report

B2B Chocolate Market Segmentations

By Product Type

- Cocoa Liquor

- Industrial Dark Chocolate

- Industrial Milk Chocolate

- Industrial White Chocolate

- Compound Chocolate & Coatings

- Chocolate Chips, Chunks & Inclusions

- Chocolate Fillings & Creams

By Application

- Bakery & Pastry Manufacturing

- Confectionery Production

- Dairy & Frozen Desserts

- Beverages & Cocoa Drinks

- Snacks & Cereals

- Foodservice & HoReCa Manufacturing

- Nutraceutical & Functional Foods

By Distribution Channel

- Direct Industrial Supply Contracts

- Ingredient Distributors & Wholesalers

- Food Ingredient Platforms

- Private Label Manufacturing Partnerships

By Form

- Liquid Chocolate

- Blocks & Slabs

- Drops & Chips

- Powdered Chocolate

By Source Type

- Conventional Cocoa

- Certified Sustainable Cocoa

- Organic Cocoa Chocolate

- Single-Origin & Specialty Cocoa

Regional Insights

North America

North America accounts for nearly 24% of the global B2B chocolate market in 2025, led primarily by the United States, where advanced food manufacturing infrastructure and strong consumer demand for premium snacks drive industrial chocolate consumption. The region benefits from highly automated production facilities that require standardized, high-quality chocolate inputs. Growth is supported by innovation in protein snacks, bakery hybrids, and premium confectionery products targeting health-conscious yet indulgence-seeking consumers.Key regional growth drivers include rising demand for premium and clean-label chocolate products, increasing investment in automation technologies, expansion of private-label confectionery manufacturing, and strong retail innovation cycles. Additionally, e-commerce-driven snack consumption and the popularity of seasonal chocolate products continue to stimulate bulk ingredient procurement.

Europe

Europe dominates global production and consumption, holding approximately 32% market share, supported by its long-standing chocolate manufacturing heritage. Countries such as Germany, Belgium, Switzerland, France, and the Netherlands serve as global hubs for chocolate processing and export-oriented confectionery production. European manufacturers emphasize high cocoa content, sustainability certifications, and premium craftsmanship, reinforcing strong demand for industrial chocolate ingredients.Regional growth is driven by advanced cocoa processing technologies, strong export demand, innovation in premium confectionery formats, and increasing adoption of sustainable sourcing practices. Regulatory emphasis on quality standards and traceability further strengthens Europe’s position as a global leader in B2B chocolate manufacturing.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, led by China, India, Japan, and Indonesia. Rapid urbanization, rising disposable incomes, and westernization of dietary habits are transforming chocolate from an occasional indulgence into a mainstream snack category. Expansion of bakery chains, café culture, and modern retail infrastructure significantly increases industrial chocolate demand.Key regional drivers include expansion of domestic food processing industries, increasing youth demographics, growing penetration of international confectionery brands, and strong investment in cold-chain logistics supporting chocolate distribution. India, in particular, demonstrates strong double-digit growth potential as organized bakery manufacturing and packaged dessert consumption expand rapidly across urban and semi-urban markets.

Latin America

Latin America, led by Brazil and Mexico, is experiencing steady growth driven by expanding packaged confectionery industries and improving food manufacturing capabilities. The region benefits from proximity to cocoa-producing countries, enabling cost advantages in raw material sourcing and processing.Regional growth drivers include increasing middle-class consumption, expansion of modern retail channels, rising domestic snack production, and investment in local cocoa grinding facilities. Manufacturers are increasingly focusing on value-added chocolate products tailored to regional taste preferences.

Middle East & Africa

The Middle East & Africa region presents a dual growth dynamic. The Middle East demonstrates strong premium chocolate consumption growth, particularly in the UAE and Saudi Arabia, where gifting culture and luxury food consumption drive demand for high-quality chocolate ingredients. Expansion of hospitality and tourism sectors further accelerates procurement by foodservice operators.Africa remains globally significant as a major cocoa-producing region while gradually increasing local processing and value addition capacity. Investments in domestic chocolate manufacturing, government support for agro-processing industries, and improving supply chain infrastructure are expected to strengthen regional participation in the global B2B chocolate value chain over the forecast period.

Key Players in the B2B Chocolate Market

- Barry Callebaut AG

- Cargill Incorporated

- Olam Food Ingredients (OFI)

- Fuji Oil Holdings Inc.

- Puratos Group

- Blommer Chocolate Company

- Guittard Chocolate Company

- Clasen Quality Chocolate

- IRCA Group

- Republica del Cacao

- Meiji Holdings Co., Ltd.

- Ezaki Glico Co., Ltd.

- Ferrero Group

- Mondelez International

- Nestlé S.A.