Australia Rum Market Size

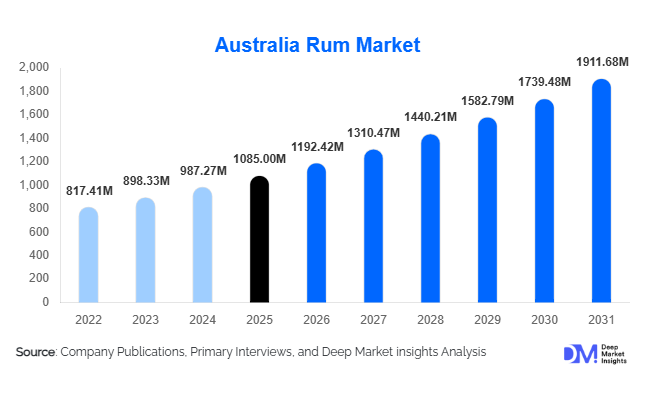

According to Deep Market Insights, the global Australia rum market size was valued at USD 1,085 million in 2025 and is projected to grow from USD 1,192.42 million in 2026 to reach USD 1,911.68 million by 2031, expanding at a CAGR of 9.9% during the forecast period (2026–2031). Market growth is primarily driven by rising global demand for premium spirits, increasing export penetration of Australian craft rum brands, and expanding cocktail culture across developed and emerging economies. Australian rum producers are increasingly gaining international recognition due to innovation in barrel aging, sustainability-led production, and strong provenance branding, positioning the category as a premium alternative to traditional Caribbean rum offerings.

Key Market Insights

- Premium and aged rum categories dominate market revenue, supported by global premiumization trends and growing consumer preference for craft spirits.

- Export-driven demand is accelerating market expansion, particularly across North America, Europe, and Asia-Pacific markets.

- Asia-Pacific leads global consumption, supported by geographic proximity and strong domestic demand within Australia.

- Craft distilleries are reshaping competitive dynamics, introducing small-batch innovation and premium storytelling strategies.

- Cocktail and mixology culture expansion is significantly increasing on-trade consumption worldwide.

- Sustainability-led production and climate-assisted aging advantages are strengthening Australia’s global positioning in premium rum.

What are the latest trends in the Australia rum market?

Premium Craft Rum Becoming a Global Export Category

Australian rum has transitioned from a domestically focused spirits category into an export-oriented premium product. Distilleries are emphasizing authenticity, locally sourced ingredients, and experimental barrel finishes to differentiate their offerings internationally. Limited-edition releases and aged expressions are gaining traction among collectors and premium consumers. Export markets increasingly perceive Australian rum similarly to premium Australian wine—high quality, innovative, and sustainably produced. This trend is encouraging distilleries to scale aging inventories and invest in brand storytelling, packaging innovation, and international distribution partnerships.

Technology and Sustainability Transforming Production

Technological integration within distillation and maturation processes is improving production efficiency and product consistency. Climate-controlled warehouses, AI-supported fermentation monitoring, and renewable-energy distillation systems are increasingly adopted by producers. Sustainability initiatives such as water recycling, waste-to-energy utilization, and eco-certified packaging are becoming core differentiators. These innovations not only reduce operational costs but also attract environmentally conscious consumers and premium retailers globally, reinforcing long-term brand competitiveness.

What are the key drivers in the Australia rum market?

Global Premiumization of Alcohol Consumption

Consumers worldwide are shifting toward higher-quality alcoholic beverages, prioritizing flavor complexity, craftsmanship, and authenticity over volume consumption. Australian rum producers benefit from this trend as most brands operate within premium or super-premium price tiers. Rising disposable income among urban consumers and growing interest in sipping spirits are accelerating demand for aged rum variants, contributing significantly to revenue growth.

Expansion of Cocktail and Hospitality Culture

The global resurgence of cocktail culture is a major growth catalyst. Bars and restaurants increasingly seek distinctive rum profiles for signature cocktails, creating demand for Australian rum’s unique aging characteristics. Hospitality expansion across North America, Europe, and Southeast Asia is strengthening on-trade consumption, while mixologists play a critical role in brand discovery and adoption among younger consumers.

What are the restraints for the global market?

High Production and Operating Costs

Australian rum producers face comparatively higher labor, compliance, and energy costs than Caribbean competitors. These cost structures limit competitiveness in economy segments and require producers to maintain premium pricing strategies. Smaller distilleries particularly face challenges in scaling production while preserving margins.

Export Logistics and Regulatory Complexity

Alcohol taxation differences, shipping costs, and regulatory compliance requirements across international markets present barriers to rapid expansion. Market entry into emerging economies often requires complex licensing and distribution partnerships, slowing penetration for smaller brands.

What are the key opportunities in the Australia rum industry?

Tourism-Driven Distillery Experiences

Experiential tourism presents a significant opportunity for Australian rum producers. Distillery tours, tasting rooms, and regional rum trails are becoming powerful marketing channels that strengthen brand loyalty while generating direct-to-consumer revenue. Government tourism initiatives supporting regional beverage industries are enabling distilleries to integrate hospitality services, creating diversified income streams and enhancing brand visibility among international travelers.

Sustainable and Innovative Aging Techniques

Australia’s warm climate accelerates barrel aging, allowing producers to develop complex flavor profiles faster than colder regions. This natural advantage reduces inventory holding costs while enabling premium positioning. Distilleries experimenting with native wood barrels and sustainable production certifications can access environmentally conscious consumer segments and premium retail channels, creating long-term growth opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1085 Million |

| Market Size in 2026 | USD 1192.42 Million |

| Market Size in 2031 | USD 1911.68 Million |

| CAGR | 9.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Premium and aged rum represents the leading product category, accounting for nearly 32% of the global market share in 2025, supported by the accelerating global premiumization trend within the spirits industry. Consumers are increasingly transitioning from volume-based alcohol consumption toward quality-driven purchasing behavior, favoring aged expressions characterized by longer maturation periods, refined flavor complexity, and artisanal production narratives. Rising disposable incomes, growing appreciation for craft distillation techniques, and the positioning of aged rum as a luxury sipping spirit comparable to whisky and cognac are significantly strengthening demand across developed and emerging markets. Premium rum also benefits from gifting culture expansion, particularly during festive seasons and corporate occasions, where high-value packaging and limited-edition releases enhance brand appeal and revenue realization.Dark and gold rum varieties continue to gain traction due to their versatility across both sipping and cocktail applications. Their rich flavor profiles, influenced by barrel aging and blending techniques, align well with evolving consumer preferences for complex spirits used in premium cocktail programs. Meanwhile, flavored rum is emerging as an important gateway category attracting younger legal-age consumers entering the spirits market. Innovations featuring tropical fruits, spices, and botanical infusions are helping brands expand consumption occasions and diversify portfolios. White rum remains a foundational segment, maintaining consistent demand through its extensive use in mixology, particularly within high-volume hospitality environments where classic cocktails sustain steady consumption patterns.

Application Insights

Direct consumption remains the dominant application segment, contributing approximately 48% of total market demand, driven primarily by the rising popularity of premium sipping spirits and evolving consumer perceptions of rum as a sophisticated standalone beverage. Increasing education around rum aging processes, distillery heritage storytelling, and curated tasting experiences has elevated consumer engagement, encouraging slower consumption patterns focused on quality rather than quantity. The leading driver for this segment is the global shift toward experiential alcohol consumption, where consumers seek authenticity, craftsmanship, and premium sensory experiences.The cocktail and mixology segment represents the fastest-growing application area, supported by the expansion of craft cocktail culture across metropolitan markets. Bars and restaurants are increasingly incorporating rum into innovative beverage menus, leveraging its flavor versatility to create signature drinks. Social media influence, bartender-led experimentation, and premium bar programs are accelerating adoption, particularly among urban millennials and younger professionals. Hospitality and tourism applications are also expanding as luxury hotels, resorts, and cruise operators integrate curated spirits selections to enhance guest experiences and differentiate premium offerings.Duty-free and travel retail channels are gaining strategic importance as international tourism continues to recover and cross-border travel resumes at scale. Travelers increasingly purchase premium spirits as souvenirs or gifting products, benefiting high-margin rum categories. Exclusive travel retail editions and limited-release packaging formats further stimulate impulse purchases and brand discovery in international transit hubs.

Distribution Channel Insights

Off-trade retail channels account for nearly 52% of global sales, supported by the growing accessibility of premium spirits through supermarket liquor chains, specialty alcohol retailers, and organized retail networks. The leading driver for this segment is consumer preference for at-home consumption combined with expanding premium product availability across retail shelves. Retailers are increasingly dedicating shelf space to craft and imported spirits, supported by in-store promotions, tasting programs, and premium merchandising strategies that encourage consumer experimentation.Online retail and direct-to-consumer sales are expanding rapidly as digital transformation reshapes alcohol purchasing behavior. Distilleries and distributors are investing in e-commerce platforms, subscription-based releases, and limited online exclusives that enable direct engagement with consumers. Digital channels also allow brands to communicate product origin stories, production transparency, and tasting education, strengthening brand loyalty while improving margin structures.On-trade distribution continues to play a critical strategic role despite the dominance of off-trade channels. Premium cocktail bars, upscale restaurants, and nightlife venues act as influential discovery platforms where consumers experience new rum brands for the first time. Bartender recommendations and curated drink menus significantly influence downstream retail purchases, reinforcing the importance of on-premise visibility for long-term brand positioning.

End-Use Industry Insights

The hospitality and nightlife industry represents a major demand driver for Australian rum, supported by the rapid globalization of bar culture and the expansion of premium beverage programs within urban entertainment ecosystems. Hotels, fine-dining restaurants, and cocktail lounges increasingly emphasize experiential drinking environments, where premium rum offerings enhance beverage diversity and customer engagement. The leading growth driver within this segment is the recovery and expansion of global tourism combined with rising consumer willingness to spend on premium leisure experiences.Luxury hotels and resorts are integrating craft spirits menus and curated tasting experiences, positioning premium rum alongside established luxury spirits categories. This trend is particularly visible in resort destinations and metropolitan hospitality hubs seeking differentiation through elevated food and beverage offerings. Additionally, the emergence of ready-to-drink (RTD) alcoholic beverages incorporating rum is creating new consumption occasions beyond traditional bar settings. RTD formats appeal to convenience-oriented consumers and outdoor social occasions, broadening demographic reach and increasing overall category penetration.Export-driven demand from international hospitality markets remains a primary long-term growth engine, as global tourism rebounds and premium beverage consumption expands across emerging travel destinations. Partnerships between distilleries and hospitality operators further strengthen international brand visibility and market expansion opportunities.

Explore more data points, trends and opportunities Download Free Sample Report

Australia Rum Market Segmentations

By Product Type

- White Rum

- Gold Rum

- Dark Rum

- Spiced Flavored Rum

- Premium Aged Rum

- Overproof Specialty Rum

By Application

- Direct Consumption

- Cocktails Mixology

- Hospitality Tourism Industry

- Ready-to-Drink (RTD) Beverages

- Duty-Free Travel Retail

By istribution Channel

- Off-Trade Retail;

- On-Trade

- Online Direct-to-Consumer Sales

- Specialty Alcohol Retailers

- Travel Retail Duty-Free Stores

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest share of the Australia rum market, accounting for approximately 34% of global demand in 2025, driven by strong regional trade connectivity and rising premium alcohol consumption across developed and emerging economies. Australia continues to serve as both the primary production and consumption hub, benefiting from a mature craft distillation ecosystem and strong domestic appreciation for locally produced spirits. Regional growth is supported by rising disposable incomes, expanding middle-class populations, and increasing Western lifestyle influence shaping alcohol preferences.Japan and South Korea demonstrate particularly strong demand for premium imported spirits due to sophisticated consumer tastes and established cocktail cultures. High-end bars and luxury hospitality venues actively promote aged rum as a premium alternative to whisky, supporting category expansion. China is emerging as a high-growth market fueled by luxury consumption trends, rapid urbanization, and growing interest in imported craft spirits among affluent consumers. E-commerce penetration and premium gifting culture further accelerate regional market expansion.

North America

North America represents nearly 27% market share, led by the United States, where strong cocktail culture and premium spirits adoption continue to drive sustained growth. The primary regional growth driver is the premiumization movement reshaping consumer alcohol purchasing patterns, with consumers increasingly exploring craft and imported spirits categories. The expansion of mixology-focused bars, experiential dining concepts, and premium retail channels has significantly enhanced rum visibility across the market.The United States remains the fastest-growing country market, supported by double-digit import growth and rising consumer experimentation beyond traditional whisky and tequila categories. Growth is further reinforced by the expansion of e-commerce alcohol sales, craft beverage festivals, and bartender-led consumer education initiatives that promote rum versatility and heritage storytelling.

Europe

Europe accounts for approximately 21% of global demand, with the United Kingdom, Germany, and France serving as key consumption centers. Regional growth is primarily driven by consumer preference for aged, artisanal, and sustainably produced spirits. European consumers increasingly value provenance, environmental responsibility, and craftsmanship, aligning strongly with Australian rum producers emphasizing sustainable distillation and premium quality positioning.The region’s mature cocktail culture and strong retail infrastructure support consistent category growth, while specialty spirits retailers and premium supermarket chains enhance accessibility. Additionally, tourism-driven consumption across major European cities contributes to on-trade demand, reinforcing premium rum adoption within hospitality venues.

Middle East & Africa

Demand within the Middle East & Africa region is concentrated in luxury hospitality-driven markets, particularly in destinations such as the United Arab Emirates, where premium imported spirits are widely consumed in hotels, resorts, and high-end dining establishments. Regional growth is primarily supported by expanding luxury tourism, international events, and large-scale hospitality investments aimed at attracting global travelers.Premium beverage programs within five-star hotels and entertainment venues play a central role in driving consumption, as regulatory frameworks limit retail availability in certain markets. Rising expatriate populations and increasing demand for luxury lifestyle experiences further strengthen market expansion opportunities for premium Australian rum brands.

Latin America

Latin America represents a smaller but steadily emerging market, with Brazil and Chile demonstrating growing interest in premium imported rum categories. Regional growth is driven by expanding urban middle-class populations, increasing exposure to international craft spirits, and the rapid development of modern nightlife and cocktail culture across major cities.While locally produced rum remains dominant in several countries, consumers are increasingly exploring differentiated imported offerings positioned within the premium and super-premium segments. Rising tourism, international bar culture influence, and growing participation in global beverage trends are expected to gradually accelerate adoption across the region over the forecast period.

Key Players in the Australia Rum Market

- Bundaberg Rum

- Beenleigh Artisan Distillers

- Husk Distillers

- Brix Distillers

- Inner Circle Rum

- Killik Handcrafted Rum

- Capricorn Distilling Co.

- Nil Desperandum Rum

- JimmyRum Distillery

- Sydney Rum Distillery

- Tin Shed Distilling

- Lord Byron Distillery

- Cabarita Spirits

- Reef Distillers

- Black Gate Distillery