Ashwagandha Supplements Market Size

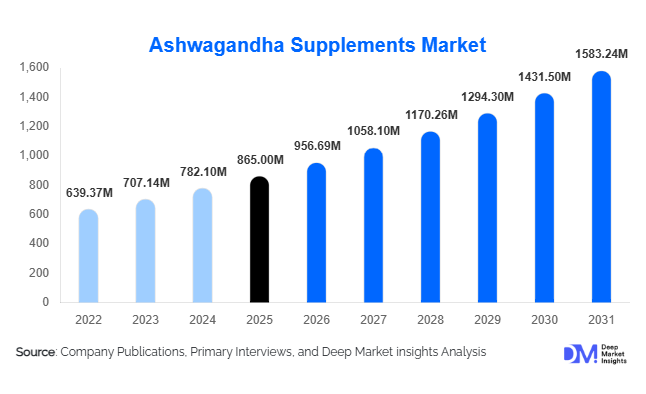

According to Deep Market Insights,The global ashwagandha supplements market size was valued at USD 865 million in 2025 and is projected to grow from USD 956.69 million in 2026 to reach USD 1,583.24 million by 2031, expanding at a CAGR of 10.6% during the forecast period (2026–2031). The market growth is primarily driven by rising global stress levels, increasing consumer preference for plant-based adaptogens, expanding sports nutrition applications, and the growing integration of Ayurvedic ingredients into mainstream nutraceutical formulations. Standardized extracts with defined withanolide content, premium capsule formats, and strong e-commerce penetration are collectively accelerating commercial expansion across developed and emerging economies.

Key Market Insights

- Standardized ashwagandha extracts (≥5% withanolides) dominate the market, accounting for nearly 44% of 2025 revenue due to clinical validation and consistent potency.

- Capsules remain the leading product format, contributing approximately 38% of global sales owing to precise dosing and consumer trust in pharmaceutical-style delivery.

- Stress and anxiety management is the largest application segment, representing around 41% of market share in 2025.

- North America leads global consumption, accounting for nearly 34% of total market share in 2025, driven by high nutraceutical adoption rates.

- Asia-Pacific is the fastest-growing region, supported by rising middle-class income and government-backed herbal medicine initiatives.

- Online retail channels command about 33% of total distribution, reflecting digital-first purchasing behavior and subscription-based supplement models.

What are the latest trends in the ashwagandha supplements market?

Clinical Validation and Premium Standardization

The market is witnessing a strong shift toward clinically validated, standardized extracts. Manufacturers are increasingly investing in human trials to support claims related to cortisol reduction, sleep enhancement, cognitive performance, and testosterone support. Premium extracts with guaranteed withanolide percentages are gaining traction in North America and Europe, where consumers demand transparency and scientific backing. Organic certification, non-GMO labeling, and traceability from farm to capsule are emerging as differentiators, enabling brands to command premium pricing and strengthen consumer trust.

Expansion into Sports Nutrition and Functional Blends

Ashwagandha is rapidly being integrated into sports nutrition, pre-workout blends, and recovery supplements. Scientific evidence linking the herb to improved muscle strength, endurance, and stress recovery has encouraged formulation innovation. Brands are combining ashwagandha with magnesium, L-theanine, melatonin, and vitamin B-complex to create multifunctional stress and sleep formulas. Gummies and ready-to-mix powders are also gaining popularity among younger consumers seeking convenience and taste-enhanced delivery systems.

What are the key drivers in the ashwagandha supplements market?

Rising Global Stress and Mental Wellness Awareness

Increasing work pressure, digital fatigue, and urban lifestyle stress are fueling demand for natural adaptogens. Ashwagandha’s ability to regulate cortisol levels positions it as a preferred herbal supplement for anxiety and stress management. Growing mental health awareness campaigns across the United States, Europe, and parts of Asia have further amplified demand for non-pharmaceutical solutions.

Growth of the Global Nutraceutical Industry

The broader nutraceutical industry, valued at over USD 450 billion globally, continues to expand steadily. Consumers are shifting from reactive healthcare to preventive supplementation. Ashwagandha benefits from this macro trend as it aligns with holistic health, immune resilience, and cognitive wellness. E-commerce platforms have accelerated product accessibility, enabling niche brands to scale globally without reliance on traditional retail channels.

What are the restraints for the global market?

Raw Material Price Volatility

Ashwagandha cultivation is largely concentrated in India, making the supply chain vulnerable to climatic conditions and agricultural yield fluctuations. Variability in withanolide concentration and root quality can impact extract pricing, leading to margin pressure for manufacturers. Seasonal supply constraints also influence export pricing dynamics.

Regulatory Variability Across Regions

Regulatory standards for dietary supplements vary significantly across regions. While the United States permits broader supplement claims, European regulations are more restrictive regarding health benefit communication. Such inconsistencies may slow product approvals and limit marketing flexibility, especially for new entrants.

What are the key opportunities in the ashwagandha supplements industry?

Pharmaceutical-Grade Formulations

There is significant opportunity in developing pharmaceutical-grade ashwagandha extracts supported by clinical research. Such products can expand into physician-recommended supplements and integrative medicine channels, enabling higher-margin positioning and stronger institutional adoption.

Expansion in Emerging Markets

Rising disposable incomes in China, Brazil, Southeast Asia, and the Middle East present growth potential. Government-backed traditional medicine programs and increasing consumer awareness are opening new distribution pathways. Localization of branding and culturally aligned product positioning can accelerate regional penetration.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 865 Million |

| Market Size in 2026 | USD 956.69 Million |

| Market Size in 2031 | USD 1583.24 Million |

| CAGR | 10.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

Capsules dominate the global market, accounting for approximately 38% of total revenue in 2025, primarily driven by their leading advantage in precise dosage control, enhanced stability, and extended shelf life. The capsule format is widely preferred by manufacturers due to its compatibility with standardized herbal extracts and encapsulated bioactive compounds, ensuring consistent potency and improved consumer trust. Additionally, vegetarian and plant-based capsule innovations have strengthened appeal among health-conscious and ethically aware consumers, further reinforcing this segment’s leadership position. Powders and tablets collectively represent a substantial mid-range share, supported by their cost efficiency, bulk packaging suitability, and strong adoption among fitness-oriented consumers who prefer customizable serving sizes. Gummies are emerging as one of the fastest-growing delivery formats, particularly in developed markets, as their palatable taste profile, portability, and compliance-friendly nature attract younger demographics and first-time supplement users. Liquid extracts and tinctures, while comparatively niche, continue to gain traction among consumers seeking rapid absorption, flexible dosing, and traditional botanical administration methods.

Application Insights

Stress and anxiety management leads the application landscape with nearly 41% of global market share in 2025, driven by increasing mental health awareness, rising work-related stress, and growing preference for natural adaptogenic solutions over synthetic alternatives. Clinical validation supporting cortisol regulation and mood stabilization has further accelerated adoption within this segment, establishing it as the primary revenue generator. Sports nutrition and performance enhancement represent a rapidly expanding application area, supported by scientific research highlighting improvements in muscle recovery, endurance, and energy metabolism. The expansion of organized fitness culture and preventive wellness lifestyles continues to stimulate demand in this segment. Sleep support applications are also witnessing accelerated growth as consumers increasingly seek non-habit-forming, plant-based alternatives to pharmaceutical sleep aids. Meanwhile, cognitive health and hormonal balance applications are gaining momentum due to aging populations, increased focus on women’s reproductive wellness, and rising awareness of long-term brain health maintenance, collectively broadening the market’s functional scope.

Distribution Channel Insights

Online retail accounts for approximately 33% of global sales, emerging as the leading distribution channel due to the expansion of subscription-based purchasing models, targeted digital marketing strategies, influencer partnerships, and personalized product recommendations powered by consumer data analytics. The convenience of home delivery, broader product assortments, and access to customer reviews further enhance online channel penetration. Pharmacies and specialty health stores remain integral to the distribution ecosystem, particularly in regulated markets where professional guidance and pharmacist recommendations influence purchasing decisions. This channel maintains strong credibility among older demographics and first-time users seeking reassurance regarding product safety and efficacy. Direct-to-consumer platforms are gaining strategic importance as brands leverage proprietary websites to strengthen customer loyalty, implement membership programs, and optimize margins by reducing intermediary costs. The integration of omnichannel strategies continues to reshape distribution dynamics globally.

End-Use Insights

The adult demographic aged 18–40 years contributes approximately 46% of global revenue, supported by heightened stress levels, proactive preventive healthcare spending, and increased engagement in fitness and wellness trends. This age group demonstrates strong responsiveness to digital marketing and subscription-based supplement models, reinforcing its leadership within the end-use landscape. The sports and fitness consumer segment is expanding at above-average growth rates, propelled by rising gym memberships, performance supplementation trends, and broader adoption of active lifestyles across urban populations. The geriatric population segment is steadily increasing its market participation, driven by growing concerns related to cognitive decline, immune resilience, and overall vitality maintenance. Women’s health applications, particularly in hormonal balance and reproductive wellness, are emerging as a promising niche, supported by greater awareness of personalized nutrition and increasing availability of clinically backed botanical formulations tailored to female health needs.

Explore more data points, trends and opportunities Download Free Sample Report

Ashwagandha Supplements Market Segmentations

By Product Form

- Capsules

- Tablets

- Powder

- Gummies

- Liquid Extracts/Tinctures

- Softgels

By Extract Type

- Root Extract

- Leaf Extract

- Full-Spectrum Extract

- Standardized Extract

- Organic Certified Extract

By Application

- Stress & Anxiety Management

- Sleep Support

- Cognitive & Memory Enhancement

- Sports Nutrition & Performance

- Immunity Support

- Hormonal Balance & Reproductive Health

By Distribution Channel

- Online Retail/E-commerce

- Pharmacies & Drug Stores

- Health & Specialty Stores

- Supermarkets/Hypermarkets

- Direct-to-Consumer (D2C) Platforms

By End-Use

- Adults

- Geriatric Population

- Women’s Health Segment

- Sports & Fitness Consumers

Regional Insights

North America

North America holds approximately 34% of the global market share in 2025, with the United States representing the largest consumption base. Regional dominance is supported by high per capita nutraceutical spending, advanced e-commerce infrastructure, strong presence of established supplement brands, and widespread consumer awareness of adaptogenic and plant-based formulations. The growing prevalence of stress-related disorders, coupled with preventive health adoption trends, significantly drives product demand. Canada contributes meaningfully through rising organic supplement preferences, clean-label demand, and supportive regulatory clarity that encourages premium product positioning. Continuous product innovation and influencer-driven wellness culture further accelerate regional growth.

Europe

Europe accounts for nearly 27% of global market share, led by Germany, the United Kingdom, France, and Italy. Regional growth is primarily driven by strong consumer preference for clean-label, sustainably sourced botanical supplements and heightened regulatory standards that reinforce product quality and safety. Increasing aging populations and preventive healthcare initiatives across Western Europe contribute to stable long-term demand. Additionally, rising adoption of standardized herbal extracts and clinically validated formulations supports premiumization trends within the region. Expanding online health retail networks and growing interest in plant-based lifestyles further stimulate market expansion.

Asia-Pacific

Asia-Pacific contributes approximately 25% of global demand, emerging as one of the fastest-growing regions. India plays a dual role as a major producer and expanding domestic consumer market, supported by its strong herbal heritage and expanding middle-class income levels. China and Japan are experiencing accelerated growth due to increasing health awareness, rapid urbanization, and government-supported traditional medicine initiatives. Rising disposable incomes, expanding e-commerce ecosystems, and integration of traditional botanical practices with modern nutraceutical formulations collectively drive robust regional expansion. Preventive healthcare awareness and growing demand for stress management solutions further reinforce growth momentum across metropolitan populations.

Latin America

Latin America represents approximately 7% of global demand, with Brazil and Mexico leading regional consumption. Market expansion is driven by increasing fitness culture, rising middle-class populations, and growing awareness of preventive healthcare practices. Urbanization and expanding digital retail infrastructure are facilitating wider access to nutraceutical products. Additionally, increasing penetration of international supplement brands and localized botanical formulations tailored to regional health preferences are strengthening market development across key economies.

Middle East & Africa

The Middle East & Africa account for roughly 7% of the global market, with the United Arab Emirates and South Africa serving as prominent demand centers. Growth in this region is supported by expanding high-income consumer segments, rising expatriate populations, and increasing demand for premium imported supplements. Greater awareness of preventive health measures, improving retail infrastructure, and expanding pharmacy chains contribute to gradual yet steady market development. Government initiatives promoting healthcare modernization and growing interest in lifestyle-related wellness products further enhance long-term growth prospects across the region.

Key Players in the Ashwagandha Supplements Market

- Himalaya Wellness Company

- Dabur India Ltd.

- Patanjali Ayurved Ltd.

- NOW Foods

- Nature’s Way Products LLC

- Gaia Herbs

- Organic India

- Herbalife Nutrition Ltd.

- GNC Holdings

- Life Extension

- Jarrow Formulas

- Banyan Botanicals

- NutraHerb USA

- KSM-66 Ashwagandha

- Sensoril