Artificial Meat Market Size

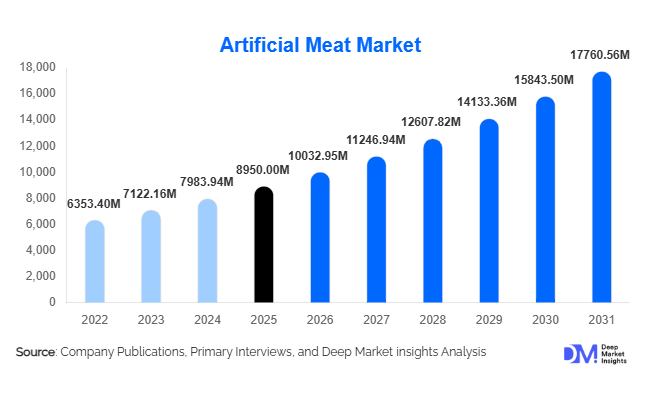

According to Deep Market Insights, the global artificial meat market size was valued at USD 8,950 million in 2025 and is projected to grow from USD 10,032.95 million in 2026 to reach USD 17,760.56 million by 2031, expanding at a CAGR of 12.1% during the forecast period (2026–2031). The artificial meat market growth is primarily driven by rising flexitarian consumption patterns, sustainability-driven food innovation, increasing regulatory approvals for cultivated meat, and strong investments in alternative protein technologies. As global food systems shift toward climate-conscious and resource-efficient protein production, artificial meat, including plant-based, cultivated (cell-based), and hybrid formats, is gaining structural relevance in retail and foodservice channels worldwide.

Key Market Insights

- Plant-based meat dominates the market with nearly 78% share in 2025, supported by established retail distribution and improving product texture realism.

- Cultivated meat is the fastest-growing segment, driven by regulatory approvals in the U.S. and Singapore and heavy venture capital investments.

- North America leads the global market with approximately 38% share, supported by technological leadership and early commercialization.

- Asia-Pacific is the fastest-growing region, expanding at nearly 15% CAGR due to protein demand growth and food security strategies.

- Retail channels account for over 64% of global sales, reflecting strong supermarket penetration and private-label expansion.

- Hybrid meat innovations combining plant protein and cultivated fat are emerging as cost-efficient, taste-enhancing solutions.

What are the latest trends in the artificial meat market?

Hybrid and Precision Fermentation Integration

One of the most prominent trends in the artificial meat market is the integration of hybrid formulations and precision fermentation technologies. Companies are blending plant-based proteins with cultivated animal fat to enhance flavor authenticity while reducing overall production costs. Precision fermentation is also being used to produce functional ingredients such as heme proteins and animal-identical fats, significantly improving sensory performance. These advancements are narrowing the taste gap between artificial and conventional meat, increasing repeat purchase rates, and accelerating foodservice adoption.

Private Label and Mainstream Retail Penetration

Retailers are expanding private-label plant-based meat offerings, making artificial meat more price-competitive. Supermarkets across North America and Europe are dedicating shelf space to alternative protein sections, normalizing consumption beyond vegan consumers. Price parity strategies, improved cold-chain logistics, and cross-merchandising alongside traditional meat are driving mainstream acceptance. This shift indicates the market’s transition from niche specialty products to mass-market protein alternatives.

What are the key drivers in the artificial meat market?

Sustainability and Carbon Reduction Targets

Livestock production contributes significantly to global greenhouse gas emissions and land degradation. Artificial meat offers up to 90% lower land use and significantly reduced water consumption compared to conventional livestock farming. Governments and multinational food companies pursuing net-zero commitments are integrating alternative proteins into procurement strategies, directly boosting market demand.

Rise of Flexitarian Consumers

Approximately 35–40% of urban consumers in developed markets identify as flexitarian, reducing meat intake without eliminating it. Artificial meat products are positioned as convenient substitutes, expanding the addressable market beyond strict vegetarians and vegans. Foodservice chains offering plant-based menu options further normalize consumption, contributing to sustained double-digit growth.

What are the restraints for the global market?

High Production Costs for Cultivated Meat

Despite technological improvements, cultivated meat production remains capital-intensive due to expensive growth media and bioreactor infrastructure. Scaling to industrial volumes while achieving price competitiveness remains a significant challenge.

Consumer Perception and Labeling Regulations

Skepticism surrounding “lab-grown” meat and regulatory debates over product labeling create uncertainty in some markets. Transparent communication, regulatory harmonization, and nutritional validation are essential to overcoming adoption barriers.

What are the key opportunities in the artificial meat industry?

Government-Backed Protein Innovation

Countries including Singapore, Israel, the U.S., and members of the EU are investing heavily in alternative protein research. Public funding for cellular agriculture infrastructure and food security initiatives creates opportunities for early-stage companies to scale operations and secure export advantages.

Emerging Market Expansion in Asia-Pacific

Rapid urbanization and protein demand growth in China, India, and Southeast Asia present significant opportunities. Localization strategies, such as artificial meat for dumplings, kebabs, and regional dishes, can accelerate adoption and open new revenue streams.

Product Type Insights

Plant-based meat continues to dominate the artificial meat market, accounting for nearly 78% of the total 2025 market revenue. Its leadership is largely driven by consumer familiarity, retail penetration, and cost competitiveness compared to cultivated meat. Health-conscious and flexitarian consumers prefer plant-based alternatives due to their lower environmental impact and allergen-friendly properties. Cultivated (cell-based) meat, although currently smaller in share, is the fastest-growing category, fueled by regulatory approvals in the U.S., Singapore, and parts of Europe, as well as premium positioning among early adopters seeking authentic taste experiences. Hybrid meat products, which blend plant-based proteins with cultivated fat, are emerging as a commercially viable middle ground, offering enhanced taste and mouthfeel while maintaining scalable production economics. Innovation in taste, texture, and functional nutrients is driving product differentiation across all sub-segments, reinforcing adoption in both retail and foodservice channels.

Form Insights

Burgers and patties lead the form segment, contributing approximately 32% of the global market in 2025. Their dominance is attributed to compatibility with QSR menu formats, consumer familiarity, and ease of mass production. Standardization of burger and patty formats allows for rapid scaling across retail and foodservice channels, while frozen and chilled offerings improve shelf life and accessibility. Nuggets, strips, and minced formats are also gaining traction, particularly in frozen retail categories and institutional catering, due to versatility in recipe applications and integration into ready-to-eat meals. This growth is driven by innovation in processing technologies that enhance texture, juiciness, and protein content, catering to a broader consumer base.

Source Ingredient Insights

Pea protein dominates the plant-based ingredient segment with an estimated 36% share within plant-based products. Its growth is propelled by allergen-friendly positioning, neutral taste profile, non-GMO sourcing, and strong investor focus on scalable production. Soy protein remains significant, especially in Asia-Pacific markets, due to established processing infrastructure and cost efficiency. Mycoprotein and fava bean proteins are expanding in Europe, driven by demand for sustainable protein alternatives and consumer preference for high-fiber, nutrient-dense options. Innovation in protein blends is enabling manufacturers to improve functional properties such as water retention, chewiness, and flavor absorption, further boosting adoption across multiple form segments.

Distribution Channel Insights

Retail channels are the backbone of the artificial meat market, accounting for approximately 64% of total global revenue in 2025. Supermarkets and hypermarkets dominate due to their ability to provide mass-market visibility and consistent product supply. Online grocery platforms are experiencing double-digit growth, accelerated by consumer convenience, subscription models, and digital marketing campaigns promoting sustainability. Foodservice is the fastest-growing channel, primarily through QSR partnerships and menu diversification strategies. Restaurants and institutional caterers are increasingly adopting artificial meat to meet consumer demand for sustainable, high-protein alternatives. Investments in cold-chain logistics, packaging innovations, and digital ordering platforms are key drivers enabling broader penetration of artificial meat across multiple channels.

End-Use Insights

Household consumption remains the largest end-use segment, representing roughly 48% of the market. Chilled and frozen retail products, meal kits, and ready-to-cook formats drive adoption in homes, supported by rising flexitarian and health-conscious consumer behavior. Quick service restaurants (QSRs) are the fastest-growing end-use segment, expanding at nearly 15% CAGR through 2031, fueled by menu innovation, sustainability commitments, and increased consumer exposure to plant-based and hybrid alternatives. Institutional catering, including airlines, schools, and corporate cafeterias, and the food processing industry, is integrating artificial meat into ready-to-eat, frozen meals and prepared foods, expanding the market’s reach. Growth in these segments is driven by cost-efficiency, operational convenience, and alignment with ESG initiatives in corporate procurement.

| By Product Type | By Form | By Source Ingredient | By Distribution Channel | By End-Use Industry |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 38% of the global artificial meat market in 2025, with the U.S. dominating regional demand. Growth is primarily driven by early regulatory approvals for cultivated meat, high consumer awareness of sustainability, and extensive retail infrastructure. Canada contributes through plant-protein manufacturing hubs and innovative start-ups focusing on hybrid products. North America benefits from a strong investor ecosystem, technological leadership in food processing, and robust adoption of QSRs and retail channels that accelerate product commercialization.

Europe

Europe holds nearly 29% market share, led by Germany, the U.K., and the Netherlands. Key growth drivers include strong government policies promoting sustainable diets, high consumer environmental consciousness, and significant R&D investment in alternative proteins. Flexitarian and health-focused consumer segments are expanding, creating higher demand for pea protein, mycoprotein, and hybrid formats. Established retail chains and foodservice operators support market expansion, while regulatory harmonization around labeling and safety enhances consumer trust and adoption.

Asia-Pacific

Asia-Pacific accounts for around 23% of global revenue and is the fastest-growing region, with a CAGR of roughly 15%. China is a major long-term growth driver due to rising middle-class protein demand, urbanization, and increasing awareness of health and sustainability. Singapore is the regional leader in cultivated meat commercialization, supported by government-backed pilot programs and export-oriented production. India is emerging as a key plant-based innovation hub, driven by vegetarian dietary patterns, growing disposable income, and domestic start-ups creating culturally adapted meat alternatives. Regional growth is further supported by e-commerce expansion, rising QSR adoption, and partnerships between local food manufacturers and global alternative protein companies.

Latin America

Latin America contributes approximately 6% of global demand, with Brazil and Mexico leading adoption. Market growth is moderate due to the dominance of conventional meat industries, but increasing urbanization, awareness of health and sustainability, and expansion of modern retail chains are driving incremental adoption. Investment in local production capabilities, particularly in plant-based proteins, is expected to support steady growth in the coming years.

Middle East & Africa

This region accounts for about 4% of global revenue. Israel is a global innovation hub for cultivated meat R&D, while the UAE leverages food security initiatives to adopt artificial meat solutions. Growth is fueled by government support for sustainable protein production, rising consumer income, and awareness of environmental impact. Partnerships with multinational food companies and the establishment of production and research facilities further drive market adoption.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Artificial Meat Market

- Beyond Meat

- Impossible Foods

- Quorn Foods

- Eat Just

- Upside Foods

- Maple Leaf Foods

- Nestlé

- Tyson Foods

- Vivera

- Sunfed

- Meatable

- Aleph Farms

- GOOD Meat

- Moving Mountains

- Future Meat Technologies