Apple Juice Concentrate Market Size

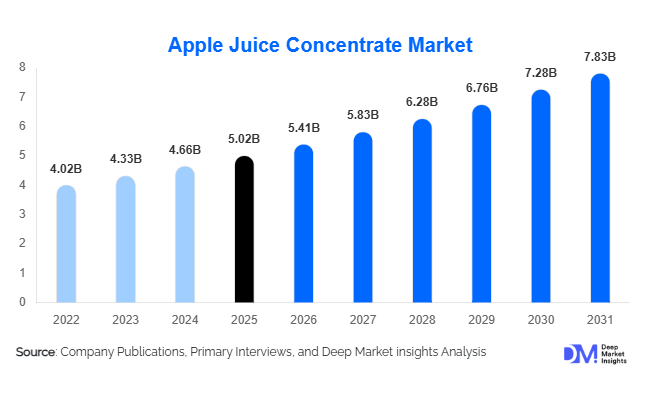

According to Deep Market Insights, the global apple juice concentrate market size was valued at USD 5.02 billion in 2025 and is projected to grow from USD 5.41 billion in 2026 to reach USD 7.83 billion by 2031, expanding at a CAGR of 7.7% during the forecast period (2026–2031). The apple juice concentrate market growth is primarily driven by rising demand for fruit-based beverages, increasing use of natural sweeteners in processed foods, and growing adoption of clean-label ingredients across the food and beverage industry.Apple juice concentrate is widely used in beverage manufacturing due to its long shelf life, ease of transportation, stable flavor profile, and cost efficiency. Beverage producers increasingly utilize apple juice concentrate in ready-to-drink juices, smoothies, flavored water, functional beverages, and sports drinks. The growing global preference for naturally sourced ingredients is accelerating adoption in bakery, confectionery, dairy, and nutraceutical applications.

Asia-Pacific dominates global production and consumption, led by China’s large-scale apple cultivation and export-oriented processing infrastructure. Europe remains a major premium market driven by organic and cloudy concentrate demand, while North America continues to witness strong consumption across health-oriented beverage categories. Technological advancements in vacuum concentration, aseptic packaging, and membrane filtration are improving product quality and operational efficiency. Sustainability initiatives, organic certifications, and traceability requirements are also reshaping procurement strategies across global beverage and food manufacturing industries.

Key Market Insights

- Apple juice concentrate is increasingly being used as a natural sweetening ingredient, replacing refined sugar and artificial additives in beverages and processed foods.

- Cloudy and organic apple juice concentrates are gaining strong traction globally, supported by rising clean-label and minimally processed food trends.

- Asia-Pacific dominates the market, led by China’s large-scale production, processing, and export capabilities.

- Europe remains the fastest-growing premium market, driven by demand for organic beverages and sustainable food ingredients.

- Functional beverages and wellness drinks are emerging as major demand drivers, increasing utilization of fruit concentrates in health-oriented formulations.

- Technological advancements in aseptic packaging and cold concentration are improving flavor preservation, shelf life, and export efficiency.

What are the latest trends in the apple juice concentrate market?

Growing Demand for Clean-Label and Organic Ingredients

Consumers are increasingly preferring natural, minimally processed ingredients across food and beverage products. This trend has significantly boosted demand for organic and cloudy apple juice concentrates, particularly in North America and Europe. Beverage manufacturers are reformulating products to eliminate artificial sweeteners and preservatives while emphasizing natural fruit-based ingredients. Organic certifications, traceability systems, and sustainable sourcing practices are becoming key purchasing criteria for both consumers and multinational beverage companies. Manufacturers are also investing in residue-free cultivation and non-GMO processing techniques to strengthen premium product positioning.

Expansion of Functional and Wellness Beverage Applications

Apple juice concentrate is increasingly being incorporated into functional beverages, immunity drinks, sports hydration products, probiotic beverages, and nutritional supplements. Consumers seeking healthier lifestyles are driving demand for beverages fortified with vitamins, antioxidants, and botanical ingredients. Apple concentrate is widely preferred as a natural flavor base and sweetening ingredient in these products because of its versatility and stable taste profile. Beverage brands are also introducing low-sugar and blended fruit beverages that combine apple concentrate with superfruits and plant-based ingredients. This trend is particularly strong in Asia-Pacific and North America where wellness-focused beverage consumption continues to rise rapidly.

What are the key drivers in the apple juice concentrate market?

Rising Consumption of Fruit-Based Beverages

The growing global demand for fruit juices, smoothies, flavored drinks, and ready-to-drink beverages is a major growth driver for the apple juice concentrate market. Consumers are increasingly shifting away from carbonated soft drinks toward healthier beverage alternatives containing natural fruit ingredients. Apple juice concentrate offers beverage manufacturers cost efficiency, flavor consistency, and extended shelf life, making it one of the most widely used fruit concentrate ingredients globally. Expanding urban populations, rising disposable incomes, and growth in organized retail are further accelerating packaged beverage demand across emerging economies.

Increasing Use of Natural Sweeteners in Food Processing

Food manufacturers are increasingly replacing refined sugar and synthetic sweeteners with fruit-derived ingredients to improve product labeling and align with health-conscious consumer preferences. Apple juice concentrate is widely utilized in bakery products, confectionery, dairy products, cereals, sauces, and infant nutrition products as a natural sweetening and flavoring ingredient. Regulatory pressure on sugar reduction in processed foods is also encouraging manufacturers to adopt fruit concentrates as alternative sweetening solutions. This trend is particularly visible in Europe and North America where clean-label product innovation remains strong.

What are the restraints for the global market?

Volatility in Raw Material Prices

The apple juice concentrate industry is heavily dependent on apple harvest yields, which are vulnerable to climatic fluctuations such as droughts, frost, hailstorms, and irregular rainfall patterns. Variations in apple production across major producing countries including China, Poland, and the United States can significantly affect raw material pricing and supply stability. Rising logistics costs and agricultural input expenses also contribute to pricing volatility, impacting manufacturer profitability and export competitiveness.

Regulatory Pressure on Sugar Consumption

Despite being naturally derived, apple juice concentrate contains high natural sugar levels, creating regulatory challenges in certain markets promoting sugar reduction initiatives. Governments and health authorities are increasingly implementing sugar labeling regulations and beverage taxation policies that may affect demand for concentrate-based beverages. Beverage companies are therefore under pressure to reformulate products with reduced sugar content, potentially limiting concentrate utilization in some applications over the long term.

What are the key opportunities in the apple juice concentrate industry?

Expansion in Emerging Beverage Markets

Rapid urbanization and rising middle-class incomes across Asia-Pacific, Latin America, and the Middle East are creating substantial opportunities for apple juice concentrate manufacturers. Countries such as India, Indonesia, Vietnam, Brazil, and Saudi Arabia are witnessing rising demand for packaged fruit beverages and flavored drinks. Local beverage companies increasingly rely on imported apple juice concentrate for juice blends and ready-to-drink formulations. Growing cold-chain infrastructure and retail modernization are further supporting market expansion across developing economies.

Sustainable and Technology-Driven Processing

Manufacturers investing in advanced concentration technologies, water recycling systems, and energy-efficient production facilities are gaining competitive advantages. Sustainability-focused processing methods are becoming increasingly important as global beverage companies prioritize environmentally responsible sourcing. Technologies such as membrane filtration, aroma recovery systems, and AI-enabled quality control are helping producers improve efficiency, reduce waste, and enhance flavor retention. Companies capable of offering traceable, sustainably produced concentrate products are expected to secure long-term supply contracts with premium beverage brands.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.02 Billion |

| Market Size in 2026 | USD 5.41 Billion |

| Market Size in 2031 | USD 7.83 Billion |

| CAGR | 7.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The clarified apple juice concentrate segment continues to dominate the global apple juice concentrate market, accounting for nearly 46% of total market share in 2025. The segment’s strong leadership position is primarily driven by its extensive application across the global beverage industry, where manufacturers prioritize visual clarity, flavor consistency, extended shelf life, and formulation flexibility. Clarified concentrates are widely utilized in premium fruit juices, flavored beverages, carbonated fruit drinks, ready-to-drink wellness beverages, syrups, and industrial food processing applications because they offer stable color characteristics and improved processing efficiency. The removal of suspended solids during clarification also allows beverage manufacturers to achieve standardized product quality at large production volumes, making clarified concentrate highly preferred among multinational beverage companies.Frozen and aseptic apple juice concentrate variants are also gaining substantial market traction due to their enhanced storage stability and export suitability. Frozen concentrates remain highly preferred in large-scale industrial applications where long-term preservation and bulk international transportation are required. Meanwhile, aseptic concentrate technologies are becoming increasingly important for manufacturers seeking microbiological safety, extended shelf life, and reduced dependency on cold-chain infrastructure. Export-oriented manufacturers in China, Poland, and the United States continue to invest heavily in advanced aseptic processing technologies to improve product quality, reduce wastage, and strengthen international competitiveness.The increasing diversification of beverage formulations globally is expected to create strong opportunities across all product categories over the forecast period. Manufacturers are increasingly focusing on innovation in low-sugar concentrates, blended fruit concentrates, and premium organic variants to address changing consumer dietary preferences and rising demand for healthier beverage alternatives.

Application Insights

Fruit juice beverages continue to represent the largest application segment within the global apple juice concentrate market, accounting for approximately 38% of total market demand in 2025. The segment’s dominance is primarily supported by the widespread use of apple juice concentrate as a natural sweetening and flavor-enhancing ingredient across blended fruit juices, flavored drinks, smoothies, and wellness beverages. Apple juice concentrate provides beverage manufacturers with significant cost advantages while maintaining natural fruit labeling claims, making it one of the most widely used fruit concentrate ingredients globally.The leading driver supporting this segment is the rapidly expanding global demand for ready-to-drink fruit beverages and naturally sweetened drink formulations. Consumers increasingly prefer beverages that contain recognizable fruit ingredients and reduced artificial additives, encouraging beverage producers to replace synthetic sweeteners with fruit-based concentrate solutions. Apple juice concentrate is particularly attractive because of its mild flavor profile, versatility, and compatibility with multiple fruit combinations, including berry, citrus, tropical, and exotic fruit beverages.The sauces, frozen desserts, and nutraceutical sectors are also contributing to market expansion. Frozen dessert manufacturers are incorporating apple concentrate into sorbets, fruit ice creams, and yogurt-based desserts, while nutraceutical companies are utilizing concentrate in botanical beverages, herbal tonics, and wellness supplements. Growing product innovation across multiple food categories is expected to sustain strong long-term application growth for apple juice concentrate globally.

Distribution Channel Insights

Direct B2B sales continue to dominate the global apple juice concentrate market, particularly among large beverage manufacturers, dairy processors, and industrial food production companies. Major multinational beverage corporations typically procure apple juice concentrate through long-term supply contracts that ensure pricing stability, quality consistency, and uninterrupted raw material availability. The leading driver supporting the dominance of this distribution channel is the growing industrial-scale demand for bulk concentrate procurement among global beverage manufacturers.Retail and e-commerce sales of packaged apple juice concentrate products are also witnessing gradual growth among household consumers. Rising consumer demand for convenient beverage preparation solutions, particularly in urban households, is encouraging retailers to expand concentrate product availability. E-commerce growth is further supporting consumer access to premium and specialty concentrate products that may not be widely available through traditional retail channels.Private-label manufacturing partnerships are becoming increasingly important as supermarket chains and retail beverage brands expand their private-label fruit beverage offerings. Retailers are collaborating with concentrate suppliers to develop cost-effective beverage products while strengthening brand differentiation strategies. This trend is expected to accelerate further as retailers seek higher-margin beverage categories and increased control over product sourcing.

End-Use Industry Insights

The beverage manufacturing industry remains the largest end-use segment in the global apple juice concentrate market, contributing approximately 52% of total demand in 2025. The segment’s dominance is primarily driven by the rapid expansion of ready-to-drink beverages, flavored waters, juice blends, sports drinks, and wellness beverages across both developed and emerging markets. The leading driver supporting this segment is the continuous rise in global consumption of convenient packaged beverages among urban consumers.Nutraceutical and wellness beverage manufacturers are increasingly incorporating apple juice concentrate into immunity beverages, botanical drinks, herbal formulations, and plant-based nutritional products. Growing global awareness regarding preventive healthcare and wellness-oriented nutrition is accelerating product innovation within the functional beverage industry. Manufacturers are actively developing fortified drinks containing antioxidants, vitamins, probiotics, and plant extracts combined with natural fruit concentrates.The processed food manufacturing industry is also creating substantial growth opportunities for concentrate suppliers. Apple juice concentrate is increasingly utilized in breakfast cereals, snack products, sauces, marinades, frozen desserts, bakery items, and confectionery products due to rising demand for natural ingredient alternatives. Continued diversification of processed food applications is expected to support long-term expansion across the end-use landscape.

Explore more data points, trends and opportunities Download Free Sample Report

Apple Juice Concentrate Market Segmentations

By Product Type

- Clarified Apple Juice Concentrate

- Cloudy Apple Juice Concentrate

- Organic Apple Juice Concentrate

- Conventional Apple Juice Concentrate

- Frozen Apple Juice Concentrate

- Aseptic Apple Juice Concentrate

- Reduced Sugar Apple Juice Concentrate

By Application

- Fruit Juice Beverages

- Functional & Wellness Beverages

- Dairy Products

- Bakery & Confectionery

- Alcoholic Beverages & Cider

- Nutraceuticals & Dietary Supplements

- Sauces, Dressings & Processed Foods

By End-Use Industry

- Beverage Manufacturing

- Food Processing Industry

- Dairy Industry

- Alcoholic Beverage Industry

- Nutraceutical Industry

- HoReCa Sector

- Retail & Household Consumption

By Distribution Channel

- Direct B2B Sales

- Food Ingredient Distributors

- Online Ingredient Platforms

- Specialty Beverage Ingredient Suppliers

- Retail Stores

- E-commerce Platforms

By Packaging Type

- Drums

- Intermediate Bulk Containers (IBCs)

- Bag-in-Box Packaging

- Aseptic Tanks

- Retail Bottles & Pouches

Regional Insights

North America

North America accounts for approximately 21% of the global apple juice concentrate market, supported by strong beverage consumption patterns, advanced food processing infrastructure, and growing consumer demand for healthier beverage alternatives. The United States and Canada remain the primary contributors to regional market growth due to their large-scale beverage manufacturing industries and increasing preference for natural fruit ingredients.The United States continues to represent a major importer, processor, and consumer of apple juice concentrate due to its highly developed beverage sector and large-scale retail distribution network. Growing investments in organic beverages, plant-based wellness drinks, and immunity-support formulations are further driving market expansion. Additionally, the region’s advanced cold-chain infrastructure and strong retail penetration continue to support stable concentrate demand across both commercial and consumer markets.

Europe

Europe represents nearly 29% of the global apple juice concentrate market in 2025 and remains one of the world’s largest premium consumption regions. Germany, France, the United Kingdom, and Poland are major markets contributing significantly to regional demand and production activity. Poland plays a particularly important role within the global supply chain due to its strong apple cultivation capacity and well-established processing infrastructure.Government regulations focused on sugar reduction and healthier food formulations are also significantly influencing regional market trends. Beverage manufacturers are increasingly reformulating products using natural fruit concentrates instead of artificial sweeteners to comply with evolving regulatory standards and changing consumer expectations. Sustainability initiatives across Europe are further encouraging investments in environmentally responsible packaging, organic farming, and carbon-efficient processing technologies.

Asia-Pacific

Asia-Pacific dominates the global apple juice concentrate market with approximately 41% market share in 2025. China remains the world’s largest producer and exporter due to extensive apple cultivation, competitive manufacturing costs, and strong export infrastructure. India is emerging as one of the fastest-growing consumption markets, while Japan and South Korea continue to import premium concentrate products for high-quality beverage manufacturing.China continues to strengthen its global leadership through investments in large-scale processing facilities, export-oriented manufacturing, and agricultural modernization. India is witnessing exceptionally strong market growth due to rising middle-class populations, expanding organized retail infrastructure, and increasing demand for fruit-based wellness beverages. Southeast Asian markets are also benefiting from rapid retail modernization, growing foodservice industries, and increasing youth-driven consumption of packaged drinks.

Latin America

Latin America is experiencing gradual but steady expansion within the apple juice concentrate market, particularly across Brazil, Mexico, and Argentina. Rising urbanization and increasing consumption of packaged fruit beverages are supporting stronger concentrate imports and local beverage production activity.Growing retail penetration, improving cold-chain logistics, and rising investments in food manufacturing infrastructure are expected to strengthen long-term market development. Economic growth across several regional economies is also encouraging increased consumer spending on convenience beverages and processed food products.

Middle East & Africa

The Middle East & Africa region is emerging as a promising growth market for apple juice concentrate due to rising urbanization, expanding tourism activity, and increasing consumption of packaged beverages. Saudi Arabia, the UAE, and South Africa represent key regional markets driving concentrate imports and beverage production growth.Saudi Arabia and the UAE continue to experience rising demand for imported fruit concentrates due to limited domestic fruit cultivation and growing consumer preference for premium packaged beverages. South Africa serves as an important regional processing and distribution hub because of its comparatively advanced food manufacturing infrastructure. Increasing investments in beverage manufacturing facilities, supermarket expansion, and modern retail chains are expected to further accelerate regional market growth during the forecast period.

Key Players in the Apple Juice Concentrate Market

- Ingredion Incorporated

- AGRANA Beteiligungs-AG

- Döhler Group

- China Haisheng Juice Holdings Co., Ltd.

- Tree Top Inc.

- SVZ International B.V.

- Lassonde Industries Inc.

- Sunsweet Growers Inc.

- Louis Dreyfus Company

- Rauch Fruchtsäfte GmbH & Co OG

- Kanegrade Ltd.

- SunOpta Inc.

- Yantai North Andre Juice Co., Ltd.

- Ve.Ba. Cooperativa Ortofrutticola S.C.

- Milne Fruit Products Inc.