Antifreeze Protein Market Size

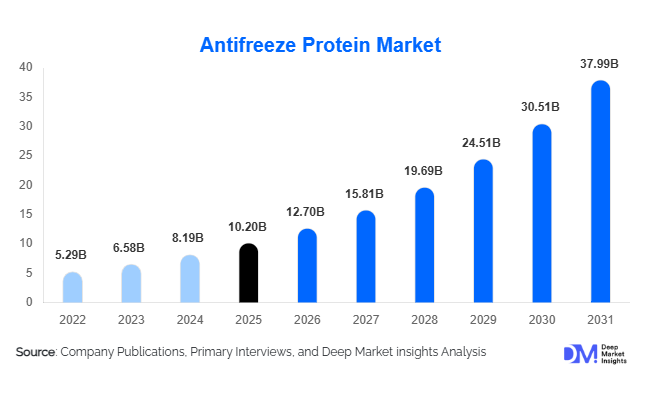

According to Deep Market Insights, the global antifreeze protein market size was valued at USD 10.2 billion in 2025 and is projected to grow from USD 12.70 billion in 2026 to reach USD 37.99 billion by 2031, expanding at a CAGR of 24.5% during the forecast period (2026–2031). The market growth is primarily driven by rising adoption of cryopreservation technologies in healthcare, increasing demand for high-quality frozen foods, and technological advancements in recombinant and synthetic antifreeze proteins, enabling broader industrial applications.

Key Market Insights

- Cryopreservation demand in biomedicine is accelerating, with AFPs playing a key role in stem cell therapies, organ preservation, and regenerative medicine.

- Frozen food industry adoption is increasing, as antifreeze proteins prevent ice recrystallization, improve texture, and enhance the quality of high-value frozen products like seafood and desserts.

- Asia-Pacific is emerging as the fastest-growing region, led by rising middle-class affluence in China and India, increasing demand for premium frozen foods, and expanding biotech research facilities.

- North America dominates the global market in 2025 due to high healthcare expenditure, strong biopharma presence, and established frozen food consumption patterns.

- Recombinant and synthetic AFP technologies are reshaping supply chains, enabling cost-effective production and custom protein variants for pharmaceutical, cosmetic, and industrial applications.

- Integration with cosmetics, agriculture, and specialty industrial applications is expanding opportunities beyond traditional biomedical and food sectors.

What are the latest trends in the antifreeze protein market?

Expansion of Recombinant and Synthetic Production

Recent trends indicate a shift from natural extraction to recombinant expression and synthetic production, offering consistent purity and scalable supply. These innovations allow manufacturers to tailor antifreeze proteins to specific applications, such as customized cryopreservation media or frozen food stabilization, reducing dependency on fish or plant sources. Advances in fermentation, protein engineering, and enzyme-assisted synthesis are improving yield, lowering costs, and enabling new formulations for cosmetics, vaccines, and industrial processes.

Food & Beverage Quality Optimization

Frozen food manufacturers are increasingly using antifreeze proteins to enhance texture and sensory quality, particularly in premium ice cream, seafood, and bakery segments. AFPs prevent ice crystal formation and freeze-thaw damage, allowing brands to maintain superior product quality while extending shelf life. This trend aligns with consumer demand for convenient, high-quality frozen foods with clean-label ingredients.

What are the key drivers in the antifreeze protein market?

Rising Demand in Healthcare and Cryopreservation

The surge in stem cell research, organ transplantation, and fertility treatments is driving demand for AFPs as superior cryoprotectants. These proteins help preserve cellular integrity during freezing, offering higher viability rates post-thaw compared to conventional cryoprotectants. Growing investments in regenerative medicine, tissue banking, and biotech research infrastructure, particularly in North America and Europe, further reinforce this trend.

Frozen Food Industry Growth

Consumer preference for convenient, high-quality frozen foods is fueling AFP adoption. The proteins improve ice crystal control and maintain sensory attributes, benefiting manufacturers of premium frozen desserts, seafood, and bakery products. Expanding cold-chain infrastructure and higher willingness to pay for quality support the growth of AFPs in food applications.

Technological Advancements

Recombinant and synthetic AFP technologies are reducing production costs and expanding application potential. Tailored protein variants for pharmaceuticals, cosmetics, and industrial cold applications are emerging, increasing versatility and stimulating adoption across multiple sectors.

What are the restraints for the global market?

High Production Costs

Despite technological advances, commercial-scale production of high-purity AFPs remains expensive, particularly for recombinant and synthetic variants. This cost barrier limits adoption in cost-sensitive applications, such as commodity frozen foods and large-volume industrial processes.

Regulatory and Safety Challenges

Antifreeze proteins are biologically active, requiring rigorous regulatory approval in pharmaceutical and food applications. Regional differences in safety standards, labeling requirements, and testing protocols can slow adoption and increase compliance costs, particularly for newer synthetic AFP variants.

What are the key opportunities in the antifreeze protein industry?

Biomedical Expansion

Opportunities lie in the growing demand for AFPs in the cryopreservation of cells, tissues, and organs. Partnerships with biotech companies and hospitals can create high-value applications, especially as stem cell therapy and regenerative medicine expand globally. AFPs enable enhanced survival rates and functional preservation, making them critical for advanced medical procedures.

Frozen Food Innovation

AFP integration into frozen food manufacturing presents opportunities to enhance texture, reduce ice damage, and extend shelf life. Collaborations between AFP producers and premium food brands can lead to product differentiation, particularly in ice cream, bakery, and seafood segments. This aligns with growing consumer preference for convenience and quality.

Cosmetics and Specialty Applications

AFPs offer functional benefits in cosmetics, personal care, and agricultural frost-protection products. Climate-resilient crops and premium winter skincare products are emerging applications, allowing companies to command higher value and explore cross-industry integration beyond traditional markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 10.2 Billion |

| Market Size in 2026 | USD 12.70 Billion |

| Market Size in 2031 | USD 37.99 Billion |

| CAGR | 24.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Type I antifreeze proteins (AFPs) dominate the global market, accounting for approximately 35% of total revenue in 2025. Their leadership position is primarily driven by strong ice recrystallization inhibition properties, relatively simpler molecular structure, and cost-efficient production compared to other AFP variants. Type I AFPs are widely adopted in both biomedical cryopreservation and premium frozen food stabilization, making them the most commercially versatile segment. In healthcare, they are extensively used in stem cell storage, reproductive medicine, and tissue preservation due to their ability to maintain cellular membrane integrity during freeze–thaw cycles. In food applications, their ability to control ice crystal growth ensures superior texture and mouthfeel, particularly in frozen desserts and seafood.

Type II and Type III AFPs collectively represent nearly 30% of the market, primarily serving high-value biomedical applications such as organ preservation and advanced research. These variants demonstrate higher specificity to ice crystal surfaces and are often preferred in specialized pharmaceutical formulations. Antifreeze glycoproteins (AFGPs) account for around 15% of the market, driven by niche applications in organ transplantation research and vaccine stabilization.

Application Insights

Cryopreservation remains the leading application segment, accounting for nearly 40% of the global market value in 2025. Growth is primarily fueled by rising demand for stem cell banking, regenerative medicine, fertility preservation, organ transplantation research, and vaccine stabilization. Increasing healthcare expenditure in developed economies and the rapid expansion of biopharmaceutical pipelines are major growth drivers. Antifreeze proteins are increasingly replacing conventional cryoprotectants due to their superior ability to reduce ice crystal damage and enhance post-thaw cell viability.

Frozen food applications represent approximately 30% of the market, driven by expanding global consumption of ready-to-eat and premium frozen products. AFPs significantly improve texture stability, reduce recrystallization, and extend shelf life, making them valuable for ice cream, seafood, processed meats, and bakery items. Rising urbanization, dual-income households, and improved cold-chain logistics in Asia-Pacific and Latin America are further supporting segment expansion.

Distribution Channel Insights

Direct B2B supply channels dominate, accounting for more than 60% of global sales, particularly in pharmaceutical, biotechnology, and large-scale food manufacturing sectors. Long-term procurement contracts, customized formulations, and regulatory compliance requirements favor direct manufacturer-to-end-user relationships. Major AFP producers collaborate closely with biopharma companies to develop application-specific cryopreservation media, strengthening strategic partnerships and recurring revenue streams.

Specialized distributors and life-science suppliers represent nearly 25% of sales, primarily serving research institutions and mid-sized industrial buyers. Meanwhile, online procurement platforms are expanding rapidly, especially for laboratory-grade AFPs and small-volume purchases. Digital marketplaces improve accessibility and streamline purchasing processes, particularly in emerging markets. The increasing digitization of procurement systems and global supply chain optimization is expected to further strengthen distribution efficiency across regions.

Explore more data points, trends and opportunities Download Free Sample Report

Antifreeze Protein Market Segmentations

By Product Type

- Type I Antifreeze Proteins

- Type II Antifreeze Proteins

- Type III Antifreeze Proteins

- Antifreeze Glycoproteins (AFGPs)

- Synthetic / Recombinant Antifreeze Proteins

By Application

- Cryopreservation

- Frozen Food Processing

- Cosmetics & Personal Care

- Agriculture & Crop Frost Protection

- Research & Industrial Applications

By Distribution Channel

- Direct B2B Sales

- Life Science & Specialty Distributors

- Online Procurement Platforms

- Contract Manufacturing & Custom Supply Agreements

Regional Insights

North America

North America accounts for approximately 40% of global market demand in 2025, making it the largest regional market. The United States leads regional growth due to its advanced biopharmaceutical industry, high healthcare expenditure, and extensive research infrastructure supporting stem cell therapies and organ transplantation programs. Strong regulatory clarity from health authorities and significant funding for regenerative medicine further drive adoption. Additionally, North America has one of the world’s largest frozen food consumption markets, supporting AFP demand in food stabilization. Canada contributes through active research institutions, cryobiology labs, and agricultural frost-protection initiatives. Government grants for biotech innovation and increasing investment in cell therapy manufacturing facilities are key drivers sustaining regional dominance.

Europe

Europe holds approximately 25% of the global market share, led by Germany, France, and the United Kingdom. Regional growth is driven by strong regulatory frameworks supporting advanced biologics, increasing funding for stem cell research, and widespread adoption of organ preservation technologies. The European Union’s emphasis on biotechnology innovation and sustainable food systems further accelerates AFP integration. Germany leads in biopharma R&D, while France and the U.K. show strong demand in frozen food and cosmetic applications. Increasing investments in cold-chain logistics and vaccine storage infrastructure across Eastern Europe are also contributing to steady regional growth.

Asia-Pacific

Asia-Pacific is the fastest-growing region, projected to expand at a CAGR exceeding 27% during the forecast period. The region currently accounts for nearly 22% of global revenue. China leads growth due to the rapid expansion of its biopharmaceutical manufacturing base, government-backed biotech initiatives, and rising frozen food consumption. India is emerging as a key growth engine with increasing stem cell banking services, expanding pharmaceutical production, and growing demand for processed foods. Japan and South Korea contribute through advanced medical research and high adoption of specialty cosmetic formulations. Expanding cold-chain infrastructure, urbanization, and rising disposable incomes are major regional growth drivers.

Latin America

Latin America represents approximately 7% of the global market, with Brazil and Argentina leading demand. Growth is supported by expanding food processing industries and rising exports of frozen meat and seafood products. Improvements in cold storage logistics and the gradual adoption of biotechnology research are contributing to increased AFP usage. While healthcare applications remain limited compared to developed regions, increasing investment in pharmaceutical manufacturing and vaccine storage capacity is expected to support moderate growth over the forecast period.

Middle East & Africa

The Middle East & Africa region accounts for nearly 6% of global demand. The UAE and Saudi Arabia are investing heavily in biotechnology infrastructure and advanced healthcare systems, driving adoption in cryopreservation and pharmaceutical applications. South Africa leads in regional frozen food processing and agricultural research. Additionally, climate variability in parts of Africa is creating opportunities for AFP-based agricultural frost protection solutions. Government diversification strategies, particularly in Gulf Cooperation Council (GCC) countries, are encouraging biotech investments, supporting gradual regional expansion.

Key Players in the Antifreeze Protein Market

- Lucas Biotech

- Sigma-Aldrich

- Enzo Life Sciences

- Proteon Pharmaceuticals

- Biocryo Solutions

- Fisher Biotech

- RayBiotech

- AdipoGen Life Sciences

- Abcam

- Creative Biolabs

- BioVision

- OriGene Technologies

- ProSpec-Tany TechnoGene

- GenScript

- Takara Bio