Animal Feed Market Size

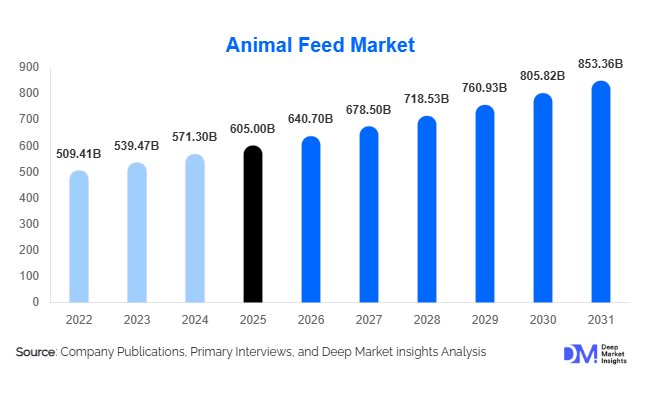

According to Deep Market Insights, the global animal feed market size was valued at USD 605.0 billion in 2025 and is projected to grow from USD 640.70 billion in 2026 to reach approximately USD 853.36 billion by 2031, expanding at a CAGR of 5.9% during the forecast period (2026–2031). The market growth is primarily supported by rising global demand for animal protein, increasing industrialization of livestock farming, and advancements in precision nutrition technologies. Rapid expansion in poultry and aquaculture production, particularly across Asia-Pacific and Latin America, is significantly strengthening feed demand worldwide. Additionally, growing adoption of nutritionally optimized compound feed and performance-enhancing additives is improving livestock productivity, encouraging farmers to transition from traditional feeding practices toward commercial feed solutions.

Key Market Insights

- Poultry feed remains the largest segment globally, driven by cost-efficient meat production and short livestock production cycles.

- Pellet feed dominates feed formats due to higher digestibility, reduced wastage, and improved feed conversion ratios.

- Asia-Pacific leads global consumption, supported by expanding livestock industries in China, India, and Southeast Asia.

- Aquaculture feed is the fastest-growing category, fueled by increasing seafood consumption and declining wild fish supply.

- Feed additives adoption is accelerating, particularly amino acids, enzymes, and probiotics improving animal health and productivity.

- Sustainability and antibiotic-free formulations are reshaping product innovation and regulatory compliance worldwide.

What are the latest trends in the animal feed market?

Precision Nutrition and Functional Feed Development

The animal feed industry is transitioning toward precision nutrition models that optimize feed formulations based on species genetics, lifecycle stages, and environmental conditions. Advanced analytics and AI-based ration formulation tools are enabling producers to maximize nutrient absorption while minimizing feed waste. Functional feed enriched with enzymes, probiotics, and immunity-enhancing additives is gaining strong adoption as livestock producers prioritize animal health and productivity. This trend also supports reduced antibiotic dependency, aligning with global regulatory shifts toward sustainable livestock farming.

Sustainable and Alternative Feed Ingredients

Sustainability concerns are accelerating the adoption of alternative proteins such as insect meal, algae-based nutrients, and fermentation-derived ingredients. These alternatives help reduce reliance on traditional fishmeal and soybean imports while lowering environmental impact. Circular economy practices, including food waste utilization and by-product recycling, are increasingly integrated into feed manufacturing. Feed producers are also investing in methane-reduction additives and low-emission formulations to meet climate targets, particularly in Europe and North America.

What are the key drivers in the animal feed market?

Rising Global Demand for Animal Protein

Growing population, urbanization, and income expansion are significantly increasing consumption of poultry, dairy, and seafood products worldwide. Poultry remains the most affordable protein source, encouraging rapid expansion of commercial poultry farming and sustained feed demand. Emerging economies are witnessing dietary shifts toward protein-rich foods, directly supporting long-term feed market growth.

Industrialization of Livestock Production

The shift from small-scale farming to integrated commercial livestock operations is a major growth catalyst. Large farms require standardized compound feed to ensure productivity, disease control, and consistent output quality. Vertical integration across poultry and dairy sectors is strengthening long-term supply contracts between feed manufacturers and livestock producers, stabilizing demand volumes globally.

What are the restraints for the global market?

Volatility in Raw Material Prices

Animal feed production heavily depends on commodities such as corn, wheat, and soybean meal. Climate disruptions, geopolitical uncertainties, and fluctuating global trade conditions frequently impact raw material prices, compressing profit margins for feed manufacturers and livestock producers.

Regulatory and Environmental Compliance Challenges

Increasing restrictions on antibiotic growth promoters and stricter environmental standards require manufacturers to reformulate products and invest in compliance systems. These regulatory pressures increase operational costs and may slow adoption in cost-sensitive developing markets.

What are the key opportunities in the animal feed industry?

Aquaculture Feed Expansion

Rapid growth in aquaculture production presents one of the largest opportunities for feed manufacturers. As global seafood demand rises, specialized aquafeed formulations offering optimized protein efficiency and water stability are gaining importance. Investment in sustainable fish feed alternatives is opening new revenue streams for producers targeting coastal and export-driven markets.

Government-Led Livestock Modernization Programs

Governments worldwide are investing in food security initiatives aimed at boosting domestic meat and dairy production. Programs encouraging commercial farming, feed mill expansion, and livestock productivity improvements are creating stable long-term demand for compound feed. Emerging markets in Asia, Africa, and Latin America offer strong growth potential for new entrants and global manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 605 Billion |

| Market Size in 2026 | USD 640.70 Billion |

| Market Size in 2031 | USD 853.36 Billion |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Livestock Type Insights

The poultry feed segment continues to dominate the global animal feed market, accounting for nearly 38% of total market share in 2025, supported by structural shifts in global protein consumption patterns and the economic efficiency of poultry production systems. Poultry remains the most affordable and widely consumed animal protein worldwide, particularly across emerging economies where urbanization and rising disposable incomes are accelerating dietary transitions toward animal-based protein sources. The shorter production cycles of broilers, combined with superior feed conversion ratios, enable faster returns for producers, encouraging continuous investments in nutritionally optimized feed formulations. Increasing adoption of precision feeding technologies and fortified feed additives further enhances growth prospects for poultry feed manufacturers.Ruminant feed represents the second-largest livestock segment, driven primarily by stable demand from the global dairy industry and consistent consumption of milk and dairy-derived products. Countries such as India maintain strong growth momentum due to expanding organized dairy farming, government support programs, and improvements in livestock productivity. In Europe, modernization of dairy operations and sustainability-focused feeding practices continue to sustain demand. Nutritional balancing aimed at improving milk yield, reproductive performance, and methane emission reduction is encouraging innovation within ruminant feed formulations.

Swine feed demand remains robust, particularly across China and Southeast Asia, where pork continues to serve as a staple protein source. Recovery of herd populations following disease-related disruptions, coupled with increasing biosecurity measures and commercial farming consolidation, is driving adoption of high-quality compound feed. Producers are increasingly focusing on feed efficiency, gut health solutions, and antibiotic alternatives, which is contributing to the expansion of value-added feed products within the swine segment.Aquaculture feed is emerging as the fastest-growing livestock category, supported by rising global seafood consumption, declining wild fish stocks, and rapid expansion of commercial aquaculture systems. Controlled fish and shrimp farming operations require specialized, nutritionally dense feed solutions designed for optimal growth and water stability. Technological advancements in feed extrusion and functional ingredient incorporation are accelerating adoption, positioning aquaculture feed as a key future growth engine within the global animal feed industry.

Feed Form Insights

Pellet feed holds approximately 46% of global market share, making it the preferred feed form worldwide due to its operational efficiency and nutritional advantages. Pelletization enhances digestibility by improving nutrient availability and minimizing feed wastage, while also ensuring uniform nutrient distribution across rations. The ability to improve storage stability and transportation efficiency further strengthens pellet feed adoption, particularly among large-scale commercial livestock operations seeking consistent performance outcomes. Growing automation in feed mills and expanding industrial livestock production continue to reinforce the dominance of pellet feed globally.Crumbles maintain strong demand within poultry production, especially for starter and grower phases where smaller particle sizes improve intake among young birds. The segment benefits from increasing poultry farming intensification and growing awareness regarding early-stage nutrition optimization. Mash feed continues to serve small and medium-scale farmers due to its lower production cost and minimal processing requirements, particularly across developing regions where price sensitivity remains high.Extruded feed is gaining increasing traction, particularly within aquaculture and specialty livestock applications. The extrusion process enhances water stability, digestibility, and nutrient density, making it ideal for aquatic species requiring slow-sinking or floating feed characteristics. Rising investments in aquaculture infrastructure and premium pet and specialty animal nutrition are supporting long-term growth of extruded feed solutions.

Ingredient Type Insights

Cereals and grains account for nearly 41% of total feed ingredient value, serving as the primary energy source in animal diets due to their high carbohydrate content and widespread availability. Corn, wheat, and barley remain essential components of feed formulations, supported by established global supply chains and relatively stable production volumes. Increasing demand for energy-dense feed formulations to enhance livestock productivity continues to reinforce the dominance of grain-based ingredients.Oilseed meals, particularly soybean meal, remain critical protein inputs for livestock nutrition, providing essential amino acids required for growth and productivity. Expanding global soybean cultivation and improved processing technologies support consistent supply, while rising protein requirements in poultry and aquaculture diets sustain demand. Feed manufacturers are increasingly optimizing protein inclusion levels to balance cost efficiency with performance outcomes.Feed additives represent the fastest-growing ingredient category as producers prioritize efficiency optimization, disease prevention, and animal welfare improvements. Enzymes, probiotics, prebiotics, amino acids, and phytogenic additives are increasingly incorporated to enhance nutrient absorption and reduce reliance on antibiotic growth promoters. Regulatory pressure and consumer preference for sustainable and residue-free animal products are accelerating adoption of functional additives globally.Alternative protein sources, including insect-based and algae-derived ingredients, are emerging as sustainable substitutes addressing supply chain volatility and environmental concerns. These novel ingredients support circular economy initiatives while reducing dependence on conventional protein sources, positioning them as long-term innovation drivers within feed formulation strategies.

End-Use Industry Insights

The meat production industry represents the largest end-use segment, contributing approximately 52% of global feed demand. Rising global population levels, expanding middle-class consumption, and increasing preference for protein-rich diets continue to drive large-scale livestock production. Industrialization of meat processing and integration of supply chains are encouraging adoption of scientifically formulated compound feed designed to maximize growth rates and production efficiency.The dairy industry remains a stable and essential contributor to feed demand, particularly across Asia and Europe where milk consumption continues to expand alongside value-added dairy product markets. Improvements in herd genetics, nutritional management, and farm mechanization are increasing reliance on specialized feed formulations aimed at improving milk yield and animal health.Aquaculture represents the fastest-growing end-use sector, expanding at over 7% annually due to strong seafood export demand and controlled farming systems that require nutritionally precise feed inputs. Government support for sustainable seafood production and technological advancements in aquaculture farming are strengthening long-term feed consumption growth.Export-oriented livestock industries in countries such as Brazil, the United States, and Thailand significantly influence global feed consumption patterns. International trade dynamics, food security strategies, and efficiency-driven livestock production models continue to shape feed demand across global markets.

Explore more data points, trends and opportunities Download Free Sample Report

Animal Feed Market Segmentations

By Livestock Type

- Poultry

- Ruminants

- Swine

- Aquaculture

- Others

By Feed Form

- Pellets

- Mash Feed

- Crumbles

- Extruded Feed

By Ingredient Type

- Cereals & Grains

- Oilseed Meals

- Feed Additives

- Alternative Proteins

- Others

By End-Use Industry

- Meat Production Industry

- Dairy Production Industry

- Aquaculture Farming

- Companion Animal Nutrition

- Commercial Livestock Operations

Regional Insights

Asia-Pacific

Asia-Pacific accounted for nearly 41% of global market share in 2025, making it the dominant regional market for animal feed. China leads regional consumption through its extensive pork and poultry industries, supported by ongoing modernization of commercial farming operations and recovery in swine production capacity. India’s expanding dairy and poultry sectors, driven by population growth, rising protein consumption, and government-backed livestock productivity initiatives, further strengthen regional demand. Southeast Asian countries including Vietnam and Indonesia are witnessing rapid adoption of aquaculture feed due to expanding seafood exports and investments in intensive farming systems. Rapid urbanization, increasing disposable income levels, and growing awareness of animal nutrition efficiency collectively serve as major drivers supporting sustained regional growth.

North America

North America holds approximately 21% market share, led by the technologically advanced livestock industry in the United States. High adoption of precision nutrition, automated feeding systems, and data-driven livestock management practices supports demand for premium and performance-enhancing feed solutions. Increasing focus on animal health, antibiotic reduction, and sustainability standards encourages continuous innovation in feed additives and formulation technologies. Canada contributes significantly through strong cattle and swine production sectors, while export-oriented meat production and stable grain supply chains reinforce regional feed manufacturing expansion.

Europe

Europe represents a mature yet innovation-driven animal feed market characterized by strict regulatory frameworks and sustainability-focused production models. Countries such as Germany, France, Spain, and the Netherlands lead adoption of environmentally sustainable and antibiotic-free feed solutions. Regulatory emphasis on emissions reduction, animal welfare, and traceability is accelerating development of alternative proteins and functional feed additives. Growing consumer demand for organic and responsibly sourced animal products continues to reshape feed formulation strategies, encouraging innovation despite moderate livestock population growth.

Latin America

Latin America’s animal feed market growth is primarily driven by export-oriented livestock industries and abundant agricultural resources. Brazil and Argentina remain key contributors, benefiting from large-scale grain production and competitive feed manufacturing costs. Brazil represents a significant share of regional feed consumption due to strong poultry and beef export performance, which encourages continuous expansion of feed milling capacity. Increasing global demand for affordable meat exports, favorable climatic conditions, and investments in commercial farming infrastructure are strengthening long-term regional growth prospects.

Middle East & Africa

The Middle East & Africa region is emerging as the fastest-growing animal feed market, supported by rising investments in food security and livestock self-sufficiency programs. Countries such as Saudi Arabia, Egypt, and South Africa are expanding poultry production to reduce dependence on imports, driving consistent feed demand growth. Government-backed agricultural modernization initiatives, improving farming practices, and increasing adoption of commercial feed solutions are transforming traditionally fragmented livestock sectors. Rapid population growth, changing dietary preferences, and expanding retail food supply chains are further accelerating regional market expansion.

Company Market Share

The global animal feed market is moderately consolidated, with the top five companies collectively accounting for approximately 24–26% of global market share. Competition focuses on formulation expertise, ingredient sourcing efficiency, geographic expansion, and development of high-value specialty nutrition solutions. Over recent years, companies have increasingly invested in acquisitions, digital nutrition platforms, and sustainable feed innovation to maintain competitive advantages.

Key Players in the Animal Feed Market

- Cargill Incorporated

- Archer Daniels Midland Company

- New Hope Group

- Charoen Pokphand Foods

- Land O’Lakes (Purina Animal Nutrition)

- Nutreco N.V.

- Alltech Inc.

- ForFarmers N.V.

- De Heus Animal Nutrition

- Tyson Foods

- Japfa Ltd.

- BRF S.A.

- Wen’s Food Group

- Kent Nutrition Group

- Godrej Agrovet Ltd.