Alternative Protein Market Size

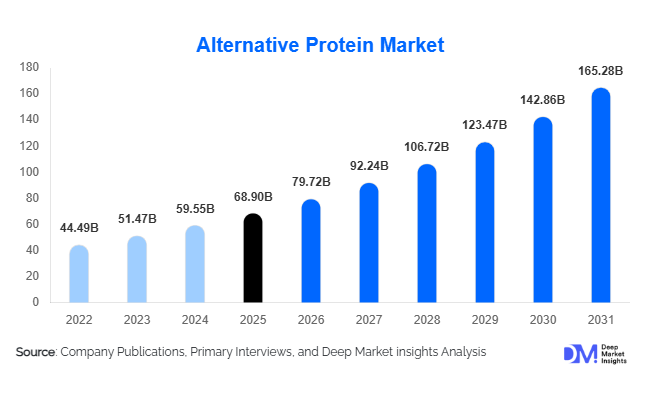

According to Deep Market Insights, the global alternative protein market size was valued at USD 68.9 billion in 2025 and is projected to grow from USD 79.72 billion in 2026 to reach USD 165.28 billion by 2031, expanding at a CAGR of 15.7% during the forecast period (2026–2031). The alternative protein market growth is primarily driven by increasing demand for sustainable food systems, rising consumer adoption of plant-based and flexitarian diets, and rapid advancements in food technology such as fermentation and cellular agriculture. Food manufacturers are increasingly integrating plant-derived, microbial, and cultivated protein ingredients into a wide range of products including meat substitutes, dairy alternatives, protein supplements, and functional foods.

Key Market Insights

- Plant-based proteins dominate the global market, accounting for more than 60% of total demand due to established supply chains and strong consumer familiarity.

- Meat alternatives remain the leading application segment, driven by growing demand for plant-based burgers, sausages, and processed meat substitutes.

- North America leads the global market, supported by strong innovation ecosystems and high consumer adoption of plant-based diets.

- Asia-Pacific is the fastest-growing region, fueled by rising protein demand and government investments in sustainable food technologies.

- Fermentation-based proteins and cultivated meat technologies are gaining significant venture capital and government funding.

- Retail and supermarket channels dominate product distribution, while e-commerce platforms are expanding rapidly for plant-based food brands.

What are the latest trends in the alternative protein market?

Rapid Growth of Plant-Based Food Innovation

Food manufacturers are investing heavily in plant-based product development to replicate the taste, texture, and nutritional profile of traditional meat and dairy products. Technologies such as high-moisture extrusion are enabling manufacturers to produce realistic plant-based meat alternatives with fibrous textures similar to animal meat. Companies are launching plant-based burgers, nuggets, sausages, and dairy alternatives that closely mimic conventional products. Retailers and quick-service restaurant chains are also expanding plant-based menu options to cater to growing consumer demand. The rise of flexitarian diets—where consumers reduce but do not eliminate animal protein consumption—has significantly expanded the consumer base for alternative protein products.

Advancements in Precision Fermentation and Cellular Agriculture

Precision fermentation and cultivated meat technologies are rapidly transforming the alternative protein industry. Precision fermentation enables the production of animal-identical proteins such as whey and casein without traditional livestock farming. These proteins are increasingly used in dairy-free cheese, yogurt, and protein beverages. At the same time, cellular agriculture technologies are advancing toward scalable cultivated meat production. While still in early commercialization stages, several companies are building pilot production facilities and working with regulators to bring lab-grown meat products to market. These innovations are expected to significantly expand the alternative protein market in the coming decade.

What are the key drivers in the alternative protein market?

Growing Consumer Focus on Sustainability and Climate Impact

Environmental sustainability is one of the strongest drivers of alternative protein adoption. Conventional livestock production contributes significantly to greenhouse gas emissions, land use, and water consumption. Alternative protein sources such as plant-based and microbial proteins require substantially fewer natural resources, making them more sustainable options. Governments, environmental organizations, and food companies are increasingly promoting sustainable food systems to reduce climate impact. As consumers become more aware of environmental issues, demand for low-carbon protein sources is accelerating globally.

Increasing Health Awareness and Dietary Shifts

Consumers are increasingly adopting healthier dietary patterns that emphasize plant-based foods. Alternative proteins are often perceived as healthier due to their lower saturated fat levels and absence of cholesterol. Many plant-based proteins also provide additional nutritional benefits such as fiber, vitamins, and antioxidants. The growth of sports nutrition and functional foods has further boosted demand for protein ingredients derived from plants and microbes. Health-conscious consumers are increasingly choosing protein-enriched snacks, beverages, and meal replacements made with alternative protein sources.

What are the restraints for the global market?

High Production Costs of Novel Protein Technologies

Despite strong market growth, the production costs of many alternative proteins remain relatively high compared to conventional animal proteins. Technologies such as precision fermentation and cultivated meat require specialized equipment, advanced bioreactors, and highly controlled production environments. These factors increase capital expenditure and operational costs. As a result, many alternative protein products remain priced at a premium, limiting adoption among price-sensitive consumers.

Consumer Acceptance and Regulatory Uncertainty

Consumer perception remains a challenge for some emerging alternative protein technologies, particularly cultivated meat and genetically engineered proteins. Some consumers remain skeptical about the safety and naturalness of lab-grown or engineered food products. Additionally, regulatory approval processes for novel protein technologies vary significantly across countries. Delays in obtaining regulatory approvals can slow market expansion and limit commercialization in certain regions.

What are the key opportunities in the alternative protein industry?

Expansion in Emerging Protein-Deficit Markets

Emerging economies across Asia, Africa, and Latin America represent significant growth opportunities for the alternative protein market. Rapid population growth, rising incomes, and increasing protein consumption are creating strong demand for affordable protein sources. However, conventional livestock production may not be able to meet this demand sustainably. Alternative proteins provide scalable and resource-efficient solutions that can help address global protein shortages while minimizing environmental impact.

Integration into Functional Foods and Sports Nutrition

The global functional food and sports nutrition industries are expanding rapidly, creating new opportunities for alternative protein manufacturers. Plant-based protein isolates such as pea, soy, and rice protein are increasingly used in protein powders, energy bars, ready-to-drink beverages, and meal replacement products. As consumers seek high-protein diets for fitness and health purposes, alternative protein ingredients are becoming essential components of modern nutrition products.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 68.9 Billion |

| Market Size in 2026 | USD 79.72 Billion |

| Market Size in 2031 | USD 165.28 Billion |

| CAGR | 15.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Insights

Plant-based proteins dominate the global alternative protein market, accounting for approximately 63% of total demand in 2025, largely driven by their commercial maturity, cost competitiveness, and strong consumer acceptance across developed and emerging markets. Soy, pea, and wheat proteins remain the most widely used sources due to their high protein content, favorable amino acid profiles, and excellent functional properties such as emulsification, binding, and texture formation. These attributes make them particularly suitable for a wide range of applications including meat analogues, dairy alternatives, bakery products, and protein-enriched snacks. In addition, well-established global agricultural supply chains and scalable processing technologies continue to support the large-scale availability of plant-based protein ingredients. The segment’s leadership is further supported by increasing consumer demand for sustainable and environmentally responsible food options, as plant proteins typically require fewer natural resources and generate lower greenhouse gas emissions compared with conventional animal protein production.

Microbial proteins, including mycoprotein and fermentation-derived proteins, are gaining significant traction as the industry explores next-generation sustainable protein production methods. These proteins are produced through controlled fermentation processes using microorganisms such as fungi, yeast, or bacteria, enabling highly efficient protein production with minimal land and water requirements. Microbial proteins also offer strong nutritional benefits, including high protein concentration and balanced amino acid composition. As biotechnology advances and fermentation infrastructure expands, microbial protein production is expected to become increasingly cost-effective and scalable.

Insect-based proteins remain a relatively niche segment of the alternative protein market but are steadily gaining acceptance, particularly in animal feed, aquaculture, and pet food applications where regulatory barriers and consumer perception challenges are less restrictive. Insects such as black soldier fly larvae and mealworms offer highly efficient feed conversion ratios and require limited land and water resources, making them an attractive sustainable protein source for feed manufacturers seeking to reduce reliance on traditional fishmeal and soy-based ingredients.

Cultivated proteins, produced through cellular agriculture technologies that grow animal cells in controlled bioreactor environments, represent the most technologically advanced segment of the market. Although large-scale commercialization remains in the early stages due to high production costs and regulatory challenges, cultivated proteins have the potential to transform the global protein industry by delivering real animal protein without the need for livestock farming. Continuous innovation in cell culture media, bioprocessing technologies, and production scale-up is expected to gradually improve economic viability and accelerate market adoption in the coming years.

Application Insights

Meat alternatives represent the largest application segment within the alternative protein market, accounting for nearly 38% of total demand in 2025. The growth of this segment is primarily driven by increasing consumer demand for healthier, environmentally sustainable, and ethically produced food options. Plant-based burgers, sausages, nuggets, and processed meat substitutes have gained widespread acceptance among flexitarian, vegetarian, and vegan consumers who are seeking alternatives to conventional meat products without compromising taste, texture, or nutritional value. Continuous innovation in food processing technologies, flavor enhancement, and texturization techniques has significantly improved the sensory profile of meat analogues, enabling manufacturers to replicate the mouthfeel and cooking behavior of traditional meat products more effectively.

Dairy alternatives represent another rapidly expanding application segment, encompassing products such as plant-based milk, yogurt, cheese, cream, and ice cream. Growing lactose intolerance prevalence, rising vegan dietary adoption, and increased consumer awareness regarding the environmental footprint of dairy production are contributing to strong demand for plant-based dairy substitutes. Innovations in plant protein formulations and processing technologies are enabling improved texture, taste, and nutritional performance, which is further accelerating adoption among mainstream consumers.

Beyond meat and dairy substitutes, alternative proteins are increasingly incorporated into a wide range of food and beverage categories including sports nutrition products, functional foods, bakery products, snacks, and ready-to-eat meals. In these applications, protein enrichment has become a key product differentiation strategy as consumers seek foods that provide enhanced nutritional value, support muscle health, and promote overall wellness. As the global health and wellness trend continues to expand, demand for high-protein and protein-fortified food products is expected to further support growth across multiple application segments.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channels for alternative protein products, accounting for approximately 42% of global sales. The leading position of this segment is driven by the extensive product availability, strong brand visibility, and established retail infrastructure offered by large-scale retail chains. These stores provide consumers with easy access to a broad range of plant-based meat alternatives, dairy substitutes, and protein-enriched packaged foods, enabling brands to reach a wide consumer base and build strong market presence. In addition, in-store promotions, product sampling, and strategic shelf placement have played an important role in increasing consumer awareness and encouraging trial purchases.

Online retail platforms are emerging as one of the fastest-growing distribution channels for alternative protein products as consumers increasingly prefer the convenience of e-commerce and home delivery services. Digital grocery platforms allow consumers to explore a wider assortment of plant-based brands and specialty products that may not always be available in physical retail stores. The growth of direct-to-consumer sales strategies, subscription-based product delivery models, and targeted digital marketing campaigns is further accelerating online sales growth within the alternative protein market.

Foodservice establishments such as restaurants, cafes, and quick-service restaurant chains are also playing an increasingly important role in expanding consumer exposure to alternative protein products. Many global and regional restaurant brands are incorporating plant-based burgers, dairy-free beverages, and meat-free menu items into their offerings in response to evolving consumer preferences. The expansion of plant-based menu options across casual dining, fast food, and institutional catering sectors is significantly contributing to the mainstream adoption of alternative protein ingredients.

Explore more data points, trends and opportunities Download Free Sample Report

Alternative Protein Market Segmentations

By Source

- Plant-Based Proteins

- Microbial / Fermentation-Based Proteins

- Insect-Based Proteins

- Cultivated / Cell-Based Proteins

By Product Format

- Protein Concentrates

- Protein Isolates

- Protein Hydrolysates

- Textured Proteins (TVP/TPP)

- Ready-to-Consume Alternative Protein Foods

- Powdered Protein Ingredients

By Application

- Meat Alternatives

- Dairy Alternatives

- Bakery & Confectionery

- Functional Foods & Nutritional Products

- Sports Nutrition

- Infant Nutrition

- Animal Feed & Pet Food

- Ready-to-Eat Processed Foods

By Distribution Channel

- Retail (Supermarkets & Hypermarkets)

- Convenience Stores

- Online Retail / E-Commerce

- Foodservice (Restaurants & QSR Chains)

- Direct-to-Consumer Brands

By Technology Platform

- Extrusion Processing

- Fermentation Technology

- Cellular Agriculture / Tissue Culture

- Enzymatic Protein Processing

- Bioengineering & Synthetic Biology

Regional Insights

North America

North America holds the largest share of the global alternative protein market, accounting for approximately 36% of global demand in 2025. The region’s market leadership is driven by strong consumer awareness regarding health, sustainability, and animal welfare, which has accelerated the adoption of plant-based and alternative protein products. The United States represents the dominant market within the region, supported by a robust ecosystem of food technology startups, significant venture capital investment, and continuous product innovation by leading food manufacturers. The presence of major plant-based food brands, well-developed retail distribution networks, and strong demand from flexitarian consumers has further strengthened market expansion.

Canada also plays an important role in the regional market, particularly as a major producer and exporter of plant protein ingredients such as pea protein. Favorable agricultural conditions, government support for plant-based food innovation, and investments in large-scale protein processing facilities have positioned Canada as a global hub for plant protein supply. Additionally, increasing partnerships between food technology companies and research institutions across North America are accelerating innovation in fermentation-based proteins and cultivated meat technologies.

Europe

Europe accounts for approximately 29% of the global alternative protein market and represents one of the most mature regions for plant-based food adoption. The region’s strong growth is driven by increasing environmental awareness, supportive government policies promoting sustainable food systems, and a growing shift toward plant-forward dietary patterns. Countries such as Germany, the United Kingdom, and the Netherlands are among the leading adopters of alternative protein products, supported by strong retail penetration and active product innovation from both multinational food companies and emerging startups.

European regulatory frameworks encouraging carbon footprint reduction and sustainable agriculture are also supporting the expansion of plant-based and fermentation-derived protein solutions. In addition, the region has become a key center for research and development in cellular agriculture and fermentation technologies, which is expected to support long-term innovation and commercialization of next-generation protein sources.

Asia-Pacific

Asia-Pacific represents the fastest-growing region in the alternative protein market, with projected growth exceeding 18% CAGR during the forecast period. Rapid population growth, increasing urbanization, and rising disposable incomes are driving higher demand for protein-rich food products across the region. China represents the largest market within Asia-Pacific due to its large population base and growing focus on food security and dietary diversification. Government initiatives promoting sustainable food production and investments in food technology innovation are also supporting the development of alternative protein solutions.

Japan and South Korea are emerging as early adopters of advanced protein technologies, particularly cultivated meat and fermentation-derived proteins, supported by strong biotechnology capabilities and consumer openness to innovative food products. Meanwhile, Southeast Asian countries are witnessing rising demand for plant-based protein products as international brands expand their regional presence and retail distribution networks continue to develop. The rapid expansion of modern retail infrastructure and e-commerce platforms across Asia-Pacific is further accelerating market growth.

Latin America

Latin America is gradually emerging as a promising market for alternative proteins, supported by increasing consumer awareness regarding health, nutrition, and environmental sustainability. Brazil and Mexico represent the largest markets within the region, driven by growing demand for plant-based food products and expanding availability of alternative protein offerings in major retail chains. The region’s strong agricultural sector also provides favorable conditions for the production of plant-based protein ingredients such as soy and other legumes, which can support local manufacturing and reduce reliance on imports.

In addition, increasing investment by international plant-based food brands and regional food manufacturers is helping to expand product availability and consumer exposure to alternative protein products across urban markets in Latin America.

Middle East & Africa

The Middle East and Africa region is witnessing gradual but steady growth in alternative protein adoption, driven by rising food security concerns, water scarcity challenges, and the need to develop sustainable food production systems. Governments and private investors across the region are increasingly supporting the development of food technology innovations that can reduce dependence on traditional livestock farming.

Countries such as the United Arab Emirates and Israel are emerging as important innovation hubs for alternative protein technologies. Significant investments in cultivated meat research, fermentation-based protein production, and vertical farming solutions are helping to position these countries at the forefront of food technology development in the region. At the same time, increasing urbanization, expanding modern retail infrastructure, and growing consumer interest in healthier dietary choices are contributing to the gradual expansion of the alternative protein market across the Middle East and Africa.

The alternative protein market is moderately consolidated, with the top five companies collectively accounting for approximately 35% of global market share. Leading companies are focusing on product innovation, strategic partnerships, and geographic expansion to strengthen their market positions.

Key Players in the Alternative Protein Market

- Beyond Meat

- Impossible Foods

- Oatly Group

- Ingredion Incorporated

- Kerry Group

- Archer Daniels Midland

- Cargill Incorporated

- Roquette Frères

- DSM-Firmenich

- Tyson Foods

- Nestlé

- Danone

- Quorn Foods

- SunOpta

- Bühler Group