Alternative Flour Market Size

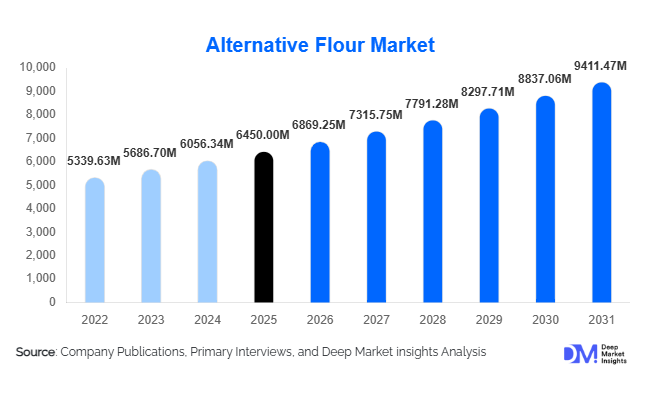

According to Deep Market Insights, the global alternative flour market size was valued at USD 6,450 million in 2025 and is projected to grow from USD 6,869.25 million in 2026 to reach USD 9,411.47 million by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The alternative flour market growth is primarily driven by increasing health consciousness, rising prevalence of gluten intolerance and celiac disease, expansion of plant-based and vegan diets, and growing demand for functional and clean-label bakery and snack products globally.

Key Market Insights

- Health-conscious consumers are driving demand for gluten-free, high-protein, and fiber-rich flours, including almond, chickpea, coconut, and millet-based options.

- Bakery and snack food applications dominate consumption, fueled by innovation in gluten-free bread, cookies, and protein-enriched products targeting both retail and foodservice sectors.

- North America leads the market, with the U.S. and Canada representing the largest share due to rising dietary awareness and premium product adoption.

- Asia-Pacific is the fastest-growing region, driven by increasing urbanization, rising disposable incomes, and adoption of millet-, rice-, and chickpea-based flours in India, China, and Southeast Asia.

- Europe remains a key market for organic and clean-label flours, with Germany, the U.K., and France leading adoption due to strict food regulations and health-focused consumer trends.

- Technological adoption, including advanced milling, enzymatic processing, and hybrid flour formulations, is enabling product innovation and extended shelf life.

What are the latest trends in the alternative flour market?

Rise of Organic and Clean-Label Products

Consumers are increasingly seeking transparency in food ingredients and production practices, leading to strong growth in organic and clean-label alternative flours. Almond, chickpea, and coconut flours are particularly benefiting from this trend, as manufacturers emphasize non-GMO sourcing, minimal processing, and nutrient-rich formulations. Companies investing in sustainable sourcing and organic certification are able to charge premium prices, while building brand loyalty among health-conscious consumers.

Integration of Advanced Processing Technologies

Manufacturers are adopting technologies such as high-pressure milling, enzymatic treatment, and cold-press methods to improve flour digestibility, solubility, and shelf life. These innovations enable hybrid flour blends that combine multiple grains, legumes, and seeds to create functional and nutrient-dense products. Technology also facilitates consistent quality and scalability, allowing producers to meet the growing demands of retail, foodservice, and export markets.

What are the key drivers in the alternative flour market?

Health Awareness and Dietary Restrictions

The increasing prevalence of celiac disease, gluten intolerance, and other dietary sensitivities has led consumers to seek alternative flour options. High-protein and fiber-rich flours such as almond, chickpea, and coconut are widely used in bakery products, snacks, and ready-to-eat meals, supporting the market’s steady expansion. Rising awareness of lifestyle diseases, such as diabetes and obesity, further fuels demand for nutrient-rich, low-GI flours.

Expansion of the Bakery and Packaged Foods Industry

The global bakery and snack sector is increasingly incorporating alternative flours to meet consumer demand for gluten-free, high-protein, and functional products. Product innovations in cookies, cakes, bread, and snack bars have expanded the application of flours like almond, rice, and chickpea, driving market adoption across retail and foodservice channels.

Popularity of Plant-Based and Vegan Diets

Rising interest in plant-based diets has significantly boosted demand for flours derived from legumes, nuts, seeds, and pseudo-cereals. Products like pea flour, chickpea flour, and almond flour are increasingly incorporated into vegan meat substitutes, protein bars, and bakery items, aligning with growing consumer preferences for plant-forward nutrition.

What are the restraints for the global market?

High Production Costs

Alternative flours are more expensive than traditional wheat flour due to lower yields, specialized processing, and sourcing of nuts and legumes. These higher costs can limit adoption in price-sensitive markets and restrict penetration in developing economies.

Supply Chain Limitations

Seasonal availability and limited cultivation of raw materials, such as almonds, millet, and specialty legumes, can create supply chain challenges. Manufacturers must invest in diversified sourcing strategies to ensure consistent production and meet growing global demand.

What are the key opportunities in the alternative flour market?

Expansion in Emerging Economies

Regions like Asia-Pacific and Latin America present significant growth potential due to rising urbanization, disposable incomes, and increasing health awareness. India, China, Brazil, and Mexico are witnessing growing adoption of millet-, chickpea-, and rice-based flours, creating opportunities for market expansion and localized product strategies.

Technological Innovation in Flour Processing

Investment in advanced milling, enzymatic treatments, and hybrid flour formulations allows manufacturers to develop functional, high-value flours with improved digestibility and shelf life. These technologies help address consumer demand for nutrient-enriched, clean-label products while differentiating brands in a competitive landscape.

Government Initiatives and Sustainable Sourcing

Policies promoting local crop cultivation and sustainable food production, such as India’s “Millets Mission” and EU programs for functional foods, provide support for expanding production facilities and securing raw materials. Companies leveraging these initiatives can reduce costs, increase local sourcing, and strengthen sustainability credentials to attract conscious consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6450 Million |

| Market Size in 2026 | USD 6869.25 Million |

| Market Size in 2031 | USD 9411.47 Million |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Almond flour leads the alternative flour market with a 24% share in 2025, making it the single largest product category globally. Its leadership position is primarily driven by strong demand from gluten-free, keto, and high-protein diet consumers, particularly in North America and Europe. Almond flour offers a superior nutritional profile, including high protein, healthy fats, vitamin E, and low carbohydrate content, which aligns with rising demand for low-glycemic and functional food ingredients. Additionally, its favorable texture and flavor compatibility in baked goods make it a preferred substitute for wheat flour in premium bakery formulations. The growth of clean-label and non-GMO certified products has further strengthened almond flour’s premium positioning.

Coconut flour, chickpea flour, rice flour, and millet flour are also experiencing steady expansion. Chickpea flour is gaining traction due to its high protein and fiber content, particularly in plant-based and ethnic food applications. Rice flour remains a staple in gluten-free baking due to its neutral taste and wide availability, especially in the Asia-Pacific region. Millet flour is benefiting from government-backed promotion of climate-resilient grains in emerging markets such as India. Furthermore, hybrid flour blends—combining multiple grains, nuts, and legumes—are emerging as a high-growth segment, enabling manufacturers to offer enhanced nutritional value, improved baking functionality, and differentiated product positioning.

Application Insights

Bakery products dominate applications, accounting for 35% of total market consumption in 2025. The segment’s leadership is supported by rapid innovation in gluten-free bread, cookies, cakes, muffins, and specialty baked goods. Consumer demand for healthier indulgence has pushed bakery manufacturers to reformulate traditional products using almond, chickpea, and oat-based flours. In developed markets, retail bakery chains and artisanal producers are increasingly launching premium gluten-free SKUs, while large packaged food companies are expanding shelf space for alternative flour-based offerings.

Beyond traditional bakery, plant-based meat substitutes, protein bars, breakfast cereals, and ready-to-eat meals represent emerging high-growth applications. Chickpea and pea flours are increasingly used as protein binders in meat alternatives, while almond and coconut flours are incorporated into low-carb snack bars. The expansion of functional snacking, high-protein diets, and fortified foods is expected to significantly increase the penetration of alternative flours across diversified food categories over the forecast period.

Distribution Channel Insights

Supermarkets and hypermarkets account for 42% of global sales in 2025, making them the leading distribution channel. Their dominance is driven by strong consumer trust, extensive shelf space, competitive pricing strategies, and promotional visibility. Large retail chains are increasingly dedicating specialty sections to gluten-free, organic, and plant-based ingredients, which enhances consumer awareness and trial rates. Private-label alternative flour offerings are also expanding within these retail formats, improving affordability and accessibility.

Online channels, including e-commerce marketplaces and direct-to-consumer (D2C) brand websites, represent the fastest-growing distribution segment. Digital platforms provide detailed product information, ingredient transparency, customer reviews, and subscription-based purchasing models, which appeal strongly to health-conscious and niche consumers. The growth of online grocery delivery services, especially in North America, Europe, and urban Asia, is accelerating direct consumer access to specialty flours that may not be widely available in physical retail outlets.

End-Use Insights

The food and bakery industry remains the dominant end-use segment, contributing over 60% of total consumption in 2025. The segment’s growth is closely tied to expansion in gluten-free packaged foods, premium baked goods, and functional snack products. Large-scale food processors are increasingly integrating alternative flours into mainstream product portfolios to capture health-focused consumer segments.

Rapidly growing end-use industries include plant-based protein manufacturing, nutritional supplements, and ready-to-eat meal producers. The global plant-based food industry’s expansion is creating sustained demand for legume-based flours as protein sources and binding agents. Export-driven demand is particularly strong in the United States, Germany, the United Kingdom, and Japan, where specialty flours such as almond, chickpea, and coconut are imported for high-value food manufacturing. International trade flows are supported by rising consumer preference for premium, organic, and certified gluten-free products.

Explore more data points, trends and opportunities Download Free Sample Report

Alternative Flour Market Segmentations

By Product Type

- Almond Flour

- Coconut Flour

- Chickpea Flour

- Rice Flour

- Millet Flour

- Oat Flour

- Other Legume & Nut-Based Flours

- Hybrid/Blended Functional Flours

By Application

- Bakery Products

- Snacks & Confectionery

- Plant-Based Meat & Protein Products

- Ready-to-Eat & Convenience Foods

- Nutritional Supplements & Health Foods

By Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail & Direct-to-Consumer

- Specialty Health & Organic Stores

- Convenience Stores

- Foodservice & B2B Supply

By Nature

- Organic

- Conventional

Regional Insights

North America

North America leads the global alternative flour market with a 32% share in 2025, supported primarily by the United States and Canada. Regional growth is driven by high awareness of gluten intolerance, widespread adoption of keto and plant-based diets, and strong purchasing power for premium organic products. The presence of well-established health food brands, advanced food processing infrastructure, and a mature retail ecosystem accelerates product availability and innovation. Additionally, rising investments in clean-label reformulations by major packaged food companies are strengthening regional demand. E-commerce penetration and subscription-based health food platforms further contribute to sustained market expansion in this region.

Europe

Europe accounts for 28% of the global market, with Germany, the United Kingdom, and France serving as major contributors. Growth in the region is driven by stringent food safety regulations, high consumer preference for organic and non-GMO certified products, and increasing demand for functional and allergen-free foods. Germany is the fastest-growing country within Europe due to strong consumer acceptance of nutrient-dense grains and innovative bakery alternatives. Government support for sustainable agriculture and plant-based nutrition strategies also supports local production of alternative grains such as millet and legumes, further strengthening regional supply chains.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at a CAGR of approximately 8%. Growth is fueled by rising urbanization, increasing disposable incomes, and expanding middle-class populations in India, China, Japan, and Southeast Asia. In India, government-backed millet promotion programs are encouraging the adoption of traditional grains in modern packaged foods. China’s growing interest in functional health foods and imported premium ingredients is accelerating almond and chickpea flour demand. Additionally, rice flour remains a staple ingredient in many Asian cuisines, supporting a strong domestic production base. The region’s rapidly expanding food processing sector and modern retail penetration are expected to sustain long-term growth.

Latin America

Latin America, led by Brazil and Mexico, demonstrates moderate growth with a CAGR of approximately 6%. Regional expansion is supported by increasing urbanization, growth in the packaged bakery industry, and rising consumer awareness regarding healthier dietary options. Brazil’s expanding middle class and Mexico’s strong bakery culture provide opportunities for gluten-free and fortified flour products. Imports of almond and specialty nut flours are gradually increasing to meet premium product demand in urban retail centers. Government initiatives to improve food security and diversify crop production also contribute to long-term growth prospects.

Middle East & Africa

The Middle East & Africa region accounts for nearly 10% of the global market share. Growth is primarily driven by rising health awareness, expanding modern retail infrastructure in GCC countries, and increasing demand for gluten-free bakery products. The UAE and Saudi Arabia are key markets due to high disposable incomes and strong demand for imported premium food ingredients. In Africa, urbanization and growth in local bakery industries are supporting the gradual adoption of alternative flours. Intra-regional trade and government initiatives promoting diversified grain cultivation are expected to enhance supply chain resilience and stimulate further demand across the region.

Key Players in the Alternative Flour Market

- General Mills

- Archer Daniels Midland (ADM)

- Bob’s Red Mill

- Ingredion Incorporated

- Nestlé

- Cargill

- Puratos

- Kingsmill

- Kellogg Company

- Conagra Brands

- Nisshin Seifun Group

- Anthony’s Goods

- Manna Foods

- Shan Foods

- ADM Milling Co.