Alginate Casing Market Size

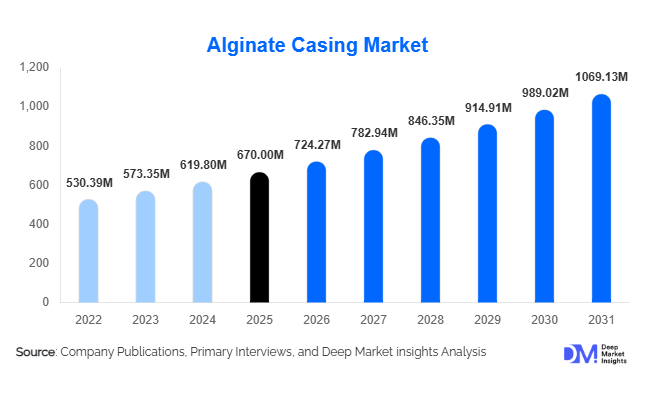

According to Deep Market Insights, the global alginate casing market size was valued at USD 670 million in 2025 and is projected to grow from USD 724.27 million in 2026 to reach USD 1,069.13 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). Market growth is primarily driven by increasing automation in food processing, rising global demand for processed and plant-based protein products, and the transition toward sustainable, seaweed-derived casing alternatives. Alginate casings enable high-speed co-extrusion manufacturing, consistent product quality, and improved food safety compliance, making them increasingly preferred over traditional natural and collagen casings across industrial meat and alternative protein production.

Key Market Insights

- Industrial automation in meat processing is accelerating alginate casing adoption, particularly through co-extrusion technologies that improve efficiency and reduce labor dependence.

- Plant-based and vegan sausage production is emerging as a major growth engine, creating strong demand for non-animal-derived casing solutions.

- Europe dominates global demand due to advanced sausage manufacturing infrastructure and early adoption of automated processing technologies.

- Asia-Pacific is the fastest-growing region, supported by expanding processed food industries in China, India, and Southeast Asia.

- Sustainability and clean-label trends are encouraging manufacturers to adopt seaweed-based ingredients aligned with ESG targets.

- Integrated equipment-and-ingredient supply models are reshaping supplier relationships, enabling long-term industrial contracts.

What are the latest trends in the alginate casing market?

Shift Toward Plant-Based Protein Manufacturing

The rapid expansion of plant-based protein production is significantly influencing the alginate casing market. Food manufacturers are increasingly using alginate casings to replicate traditional sausage textures while maintaining vegan-friendly formulations. Alginate’s neutral taste profile and customizable gel strength allow producers to create consistent products across soy, pea, and mycoprotein bases. This trend is expanding beyond Western markets into Asia-Pacific, where hybrid meat products combining plant and animal proteins are gaining popularity. As alternative protein companies scale production, alginate casings are becoming a core processing component rather than a niche ingredient.

Automation and Continuous Processing Technologies

Food processors are increasingly adopting automated co-extrusion systems capable of continuous high-volume production. Alginate casings enable seamless integration into these systems, eliminating the need for manual casing handling. Manufacturers benefit from improved yield efficiency, reduced contamination risk, and consistent product sizing. Digital monitoring systems and smart processing lines are further enhancing operational control, allowing processors to optimize casing thickness and texture in real time. This technology-driven transformation is positioning alginate casings as a key enabler of next-generation food manufacturing.

What are the key drivers in the alginate casing market?

Expansion of Processed Protein Consumption

Global consumption of processed meat and ready-to-eat foods continues to rise due to urbanization, busy lifestyles, and expanding quick-service restaurant networks. Industrial sausage production requires standardized and scalable casing solutions, driving adoption of alginate systems that allow continuous manufacturing. Large processors are increasingly transitioning away from natural casings to improve consistency and reduce production downtime.

Growing Demand for Food Safety and Hygiene Compliance

Strict food safety regulations across North America and Europe are encouraging processors to adopt controlled, non-biological casing solutions. Alginate casings reduce microbial variability and improve traceability compared with traditional natural casings. Automation also minimizes manual handling, aligning with global hygiene standards and export compliance requirements.

What are the restraints for the global market?

Raw Material Supply Volatility

Alginate production depends on seaweed harvesting, which is influenced by climate conditions and regional cultivation cycles. Variability in seaweed yield can impact pricing stability and supply consistency. Although aquaculture investments are improving supply reliability, raw material fluctuations remain a structural challenge for manufacturers.

High Initial Equipment Investment

The adoption of alginate casings often requires co-extrusion machinery upgrades and process optimization. Small and mid-sized processors may face financial barriers when transitioning from conventional casing systems. Capital intensity slows adoption in fragmented markets despite long-term efficiency benefits.

What are the key opportunities in the alginate casing industry?

Integration with Sustainable Food Production Systems

Alginate casings derived from renewable seaweed biomass align strongly with sustainability goals across the food industry. Manufacturers seeking to reduce dependence on animal-derived inputs are incorporating alginate-based materials into product development strategies. ESG reporting requirements and sustainability labeling initiatives are expected to accelerate adoption globally.

Emerging Markets Industrialization

Rapid modernization of food processing industries in Asia-Pacific and Latin America presents significant growth opportunities. Governments promoting domestic food manufacturing are supporting automation investments, indirectly boosting demand for alginate casing technologies. New entrants can benefit from partnerships with equipment suppliers and regional processors transitioning toward export-grade production standards.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 670 Million |

| Market Size in 2026 | USD 724.27 Million |

| Market Size in 2031 | USD 1069.13 Million |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global alginate casing market is strongly led by edible alginate casings, which account for nearly 68% of total demand and continue to expand their dominance due to shifting consumer preferences toward convenience foods, clean-label ingredients, and sustainable alternatives to traditional animal-derived casings. Edible alginate casings are widely utilized in ready-to-eat sausages, emulsified meat products, and rapidly growing plant-based protein applications because they provide uniform shape, controlled texture, and improved moisture retention while eliminating the need for peeling during consumption. Their compatibility with co-extrusion technology enables high-speed industrial production, significantly improving operational efficiency for large manufacturers. Continuous innovation in formulation technologies has resulted in improved elasticity, enhanced bite performance, and better thermal stability, allowing manufacturers to replicate the sensory experience of natural casings while maintaining scalability. The leading segment growth is primarily driven by rising demand for processed and alternative protein products, increasing automation in food processing, and consumer preference for allergen-free and vegetarian-friendly ingredients. Non-edible alginate casings continue to hold importance in industrial applications where structural integrity and product uniformity are prioritized, particularly in high-volume processing environments and specialized meat formulations. However, the transition toward edible formats is accelerating globally as manufacturers aim to reduce waste, streamline production processes, and align with sustainability goals.

Application Insights

Sausages and processed meat products represent the largest application segment, contributing approximately 57% of global market demand, supported by the continued expansion of industrial meat processing and rising global consumption of convenience-based protein foods. The leading segment driver is the growing reliance on automated co-extrusion systems that require consistent, high-performance casing materials capable of maintaining uniformity across large production volumes. Alginate casings provide precise diameter control, improved cooking stability, and enhanced shelf-life performance, making them highly suitable for standardized industrial production. Alongside traditional meat products, plant-based sausage applications are witnessing the fastest growth as alternative protein manufacturers increasingly adopt alginate casings to achieve realistic texture and appearance comparable to conventional sausages. This shift is reinforced by rising vegan and flexitarian consumer bases across developed and emerging markets. Seafood applications, particularly surimi and fish sausages in Asia-Pacific countries, are expanding steadily due to increased demand for structured seafood products that require stable casing solutions during processing and freezing. Additionally, the pet food sector is emerging as a promising application area, driven by premiumization trends and growing consumer willingness to purchase nutritionally enhanced and visually appealing pet products. As product diversification continues across protein categories, alginate casings are becoming a versatile solution supporting innovation across multiple food segments.

Distribution Channel Insights

Direct industrial supply contracts dominate distribution channels, accounting for nearly 64% of global sales, reflecting the highly technical and performance-driven nature of alginate casing procurement. Large food manufacturers typically establish long-term partnerships with casing suppliers to ensure consistent product quality, uninterrupted supply chains, and access to technical expertise for equipment optimization. The leading driver for this segment is the increasing integration of casing solutions with automated processing systems, which requires close collaboration between suppliers and processors during installation, calibration, and scaling of production lines. Ingredient distributors continue to play an important role in serving small and medium-sized processors, regional meat manufacturers, and emerging plant-based brands that rely on flexible purchasing models and localized technical support. Equipment-integrated supply agreements are gaining traction as casing manufacturers collaborate with co-extrusion machinery providers to deliver bundled solutions combining equipment, formulation expertise, and after-sales services. This integrated approach reduces operational complexity for processors while accelerating adoption of alginate technologies, particularly in developing markets transitioning toward industrialized food production.

End-Use Industry Insights

The meat processing industry remains the largest end-use sector, contributing around 61% of global market demand, primarily driven by expanding processed meat consumption, rising global protein demand, and increasing export-oriented production activities. The leading segment driver is the growing adoption of automated processing technologies aimed at improving production efficiency, reducing labor dependency, and ensuring consistent product quality across international markets. Alginate casings support these objectives by enabling high-speed manufacturing while maintaining uniform product dimensions and texture. Plant-based food manufacturers represent the fastest-growing end-use segment, recording double-digit growth rates globally as food companies invest heavily in alternative protein innovation to meet evolving dietary preferences and sustainability targets. Seafood processors are increasingly adopting alginate casings for structured seafood products that require enhanced stability during freezing and transportation. Meanwhile, premium pet food manufacturers are expanding usage as they introduce visually differentiated and nutritionally fortified products targeting high-income consumer segments. Export-driven food production continues to encourage large-scale adoption of advanced casing technologies, particularly among manufacturers seeking compliance with international quality and safety standards.

Explore more data points, trends and opportunities Download Free Sample Report

Alginate Casing Market Segmentations

By Product Type

- Edible Alginate Casings

- Non-Edible Alginate Casings

- Co-Extrusion Alginate Casings

- Customized Functional Alginate Casings

By Application

- Processed Meat Sausages

- Plant-Based & Vegan Sausages

- Seafood & Surimi Products

- Pet Food Products

- Convenience & Ready-to-Eat Foods

By Distribution Channel

- Direct Industrial Supply Contracts

- Ingredient Distributors

- Integrated Equipment & Ingredient Supply

- Food Processing Solution Providers

By End-Use Industry

- Meat Processing Industry

- Plant-Based Protein Manufacturers

- Seafood Processing Industry

- Pet Food Manufacturing

- Foodservice & Private Label Production

Regional Insights

North America

North America accounts for approximately 23% of global demand, led primarily by the United States, where advanced food processing infrastructure and strong consumption of processed protein products support steady market expansion. Regional growth is driven by increasing automation investments among large meat processors seeking to address labor shortages and improve production efficiency. The rapid expansion of plant-based meat brands across retail and foodservice channels has significantly accelerated demand for edible alginate casings capable of delivering consistent texture and appearance. Additionally, strong research and development ecosystems encourage innovation in alternative protein processing technologies, while consumer demand for clean-label and allergen-free food ingredients further strengthens adoption. High penetration of ready-to-eat meals and frozen food products also contributes to sustained casing utilization across industrial production facilities.

Europe

Europe dominates the global market with nearly 34% share in 2025, supported by well-established sausage manufacturing traditions and technologically advanced food processing industries. Countries such as Germany, Spain, Denmark, and the Netherlands function as key production hubs due to their expertise in processed meat manufacturing and export-oriented operations. Regional growth is driven by stringent food safety regulations that encourage standardized and hygienic casing solutions, along with strong sustainability initiatives promoting alternatives to animal-derived materials. Increasing consumer preference for transparent ingredient labeling and environmentally responsible production methods further accelerates adoption of alginate-based solutions. The region’s expanding plant-based food sector, combined with innovation in specialty sausages and gourmet processed foods, continues to create new application opportunities for alginate casings.

Asia-Pacific

Asia-Pacific holds around 29% market share and represents the fastest-growing regional market, fueled by rapid urbanization, rising disposable incomes, and modernization of food processing infrastructure. China drives the majority of regional demand through large-scale industrialization of meat and convenience food production, while Japan and South Korea contribute significantly through advanced seafood processing industries utilizing alginate casings in surimi and fish sausage applications. India and Southeast Asian countries are emerging growth engines as expanding middle-class populations increase consumption of packaged and ready-to-cook foods. Regional growth is further supported by government initiatives promoting domestic food manufacturing, increasing investment in automated processing equipment, and growing adoption of Western-style processed food products. The expansion of plant-based protein startups across Asia-Pacific also contributes to accelerating demand for edible casing technologies.

Latin America

Latin America contributes roughly 8% of global demand, led by Brazil and Mexico, where strong livestock industries and growing processed meat exports are driving modernization of food production facilities. Regional growth is supported by rising investments in automated processing technologies aimed at improving product consistency and meeting international export standards. Increasing urbanization and expanding retail distribution networks are encouraging consumption of packaged meat and convenience foods, thereby boosting demand for industrial casing solutions. Additionally, regional producers are increasingly adopting cost-efficient alginate casings to enhance scalability and reduce dependency on natural casings subject to supply fluctuations.

Middle East & Africa

The Middle East and Africa account for approximately 6% of global demand but demonstrate significant long-term growth potential as governments invest in strengthening domestic food processing capabilities to enhance food security. Countries such as Saudi Arabia, the UAE, and South Africa are expanding local meat and food manufacturing infrastructure, creating new opportunities for alginate casing suppliers. Regional growth is driven by rising population levels, increasing demand for halal-certified processed foods, and growing adoption of modern retail formats that favor standardized packaged products. Investments in cold chain logistics and food industrialization initiatives are further accelerating adoption of automated production technologies, positioning alginate casings as an efficient and scalable solution for emerging food manufacturing ecosystems.The alginate casing market is moderately consolidated, with the top five companies collectively accounting for approximately 58–62% of global market share. Competition focuses on technological innovation, product customization, and long-term partnerships with industrial food processors rather than price competition alone.

Key Players in the Alginate Casing Market

- Viscofan S.A.

- Devro plc

- Kalle GmbH

- Viskase Companies Inc.

- Shenguan Holdings Group Ltd.

- Fibran Group

- DAT-Schaub Group

- Ruitenberg Ingredients BV

- JRS Group

- Qingdao Hyzlin Biology Development Co., Ltd.

- Algaia SA

- Ceamsa

- Qingdao Gather Great Ocean Algae Industry Group

- SNAP Natural & Alginate Products

- Qingdao Bright Moon Seaweed Group