Algae Product Market Size

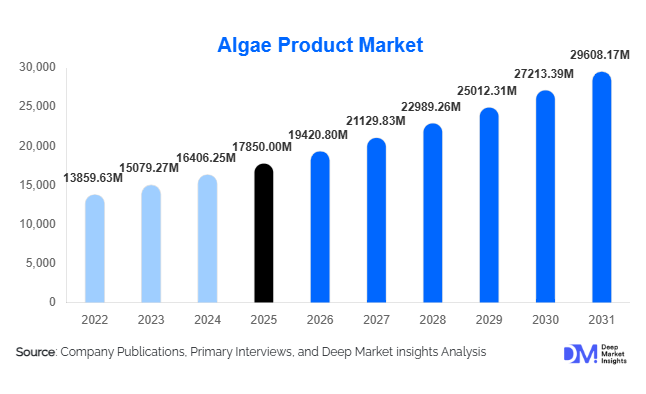

According to Deep Market Insights, the global algae product market size was valued at USD 17,850 million in 2025 and is projected to grow from USD 19,420.80 million in 2026 to reach USD 29,608.17 million by 2031, expanding at a CAGR of 8.8% during the forecast period (2026–2031). The algae product market growth is primarily driven by rising demand for plant-based nutrition, sustainable bio-based ingredients, expanding aquaculture production, and increasing adoption of algae-derived omega-3 and protein in functional foods and dietary supplements.

Key Market Insights

- Nutraceuticals & dietary supplements dominate the market, accounting for nearly 32% of global revenue in 2025, led by spirulina, chlorella, and algal DHA/EPA products.

- Asia-Pacific holds the largest regional share (35%), driven by large-scale spirulina production in China and India and rising supplement consumption in Japan.

- Hydrocolloids such as agar, carrageenan, and alginate remain critical food stabilizers, contributing approximately 24% of total market revenue.

- Aquaculture feed applications are among the fastest-growing segments, supported by expanding seafood exports from Norway, Chile, Vietnam, and China.

- Carbon capture and industrial algae cultivation are emerging growth frontiers, particularly in Europe and North America under decarbonization mandates.

- Technological advancements in closed photobioreactors and precision fermentation are reducing production costs and improving yield efficiency.

What are the latest trends in the algae product market?

Shift Toward High-Value Specialty Extracts

The algae product industry is transitioning from bulk hydrocolloids toward high-margin specialty extracts such as astaxanthin, phycocyanin, and algal omega-3 oils. These products command premium pricing due to their antioxidant properties and clinical validation in cardiovascular and cognitive health. Demand from the global dietary supplement market, valued at over USD 180 billion, continues to stimulate innovation in algae-derived functional ingredients. Manufacturers are increasingly investing in strain selection, controlled cultivation, and purification technologies to enhance bioavailability and product consistency. This trend is elevating profit margins in the nutraceutical segment to 20–30%, compared to 10–15% in commodity hydrocolloids.

Integration of Algae in Sustainable Food Systems

Algae protein and oils are gaining traction in plant-based meat, dairy alternatives, and functional beverages. Food manufacturers are leveraging algae for natural coloring, emulsification, and protein fortification. The growing flexitarian and vegan population in North America and Europe is accelerating adoption. Additionally, algae’s low land and water requirements align with sustainability goals, positioning it as a climate-resilient protein source. Partnerships between ingredient suppliers and plant-based brands are expanding, particularly in seafood analogs and high-protein snacks.

What are the key drivers in the algae product market?

Rising Plant-Based and Preventive Health Consumption

Consumer preference for natural, plant-based, and immunity-boosting ingredients is significantly driving market growth. Spirulina and chlorella are widely marketed for detoxification, protein supplementation, and antioxidant benefits. Increasing awareness of omega-3 deficiencies and concerns over fish oil sustainability are further boosting algal DHA/EPA demand. The clean-label movement has strengthened algae’s position in food and beverage formulations globally.

Expansion of Global Aquaculture Production

Aquaculture now accounts for more than half of global seafood production, creating substantial demand for algae-based feed inputs. Microalgae enhance pigmentation, immunity, and growth rates in fish and shrimp farming. Export-oriented aquaculture hubs such as Norway, Chile, Vietnam, and China are increasingly integrating algae meal and algal oil into feed formulations, supporting steady market expansion at around 9–10% CAGR in this segment.

What are the restraints for the global market?

High Production and Capital Costs

Algae cultivation requires specialized infrastructure such as photobioreactors, controlled ponds, and advanced extraction systems. Energy-intensive drying and processing stages elevate operating costs, making algae-derived ingredients more expensive than soy or fish oil alternatives. This cost barrier limits penetration in price-sensitive markets.

Scalability and Yield Variability

Open-pond contamination risks and inconsistent biomass yields pose operational challenges. Climate variability and nutrient supply fluctuations can impact productivity, especially in developing economies where advanced cultivation systems are limited.

What are the key opportunities in the algae product industry?

Carbon Capture and Industrial Decarbonization

Algae cultivation integrated with industrial CO₂ emissions offers dual economic benefits, biomass production, and carbon credit monetization. European and North American governments are supporting pilot-scale projects that utilize algae for carbon sequestration. This creates opportunities for partnerships between algae producers and heavy industries such as cement and steel.

Next-Generation Alternative Proteins

Algae-based protein isolates are emerging as viable alternatives to soy and pea protein. Their complete amino acid profile and neutral taste make them attractive for sports nutrition, bakery fortification, and plant-based seafood. Asia-Pacific and Europe are witnessing strong R&D investments in this segment, which is expected to gain significant traction post-2026.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 17850 Million |

| Market Size in 2026 | USD 19420.80 Million |

| Market Size in 2031 | USD 29608.17 Million |

| CAGR | 8.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Nutraceuticals & dietary supplements remain the leading product segment, contributing approximately 32% of global algae product market revenue in 2025. This dominance is primarily driven by strong consumer demand for plant-based omega-3 (DHA/EPA), spirulina, chlorella, astaxanthin, and phycocyanin extracts. The leading growth driver within this segment is the global shift toward preventive healthcare and clean-label supplementation. Algal omega-3, in particular, is gaining rapid adoption as a sustainable alternative to fish oil, especially in infant nutrition, cardiovascular health products, and fortified foods. Rising awareness of immunity and antioxidant benefits across North America, Europe, and Japan further strengthens this segment’s leadership.

Hydrocolloids (24% share), including agar, carrageenan, and alginate, represent the second-largest segment, supported by their indispensable role in food stabilization, gelling, and thickening applications. The primary driver here is steady processed food demand and expansion of plant-based dairy alternatives, where these ingredients serve as texturizers and emulsifiers. Their established regulatory approvals and long-standing commercial acceptance ensure stable revenue generation. Animal & aquaculture feed (18% share) is one of the fastest-growing segments, propelled by expanding global seafood exports and the need for sustainable feed inputs. Microalgae-based feed improves pigmentation, immunity, and growth efficiency in fish and shrimp farming. The leading growth catalyst is aquaculture expansion in the Asia-Pacific and Latin America. Cosmetics (10%) benefit from rising demand for marine-derived anti-aging and antioxidant formulations. Meanwhile, biofuels (8%), pharmaceuticals & biotech (5%), and bioplastics & industrial applications (3%) remain emerging but strategically important, driven by decarbonization policies and bioeconomy investments.

End-Use Industry Insights

The food & beverage industry accounts for approximately 38% of total algae product demand, making it the largest end-use segment. Growth is driven by increasing integration of hydrocolloids, natural colorants such as phycocyanin, and algae-based proteins in plant-based dairy, meat substitutes, bakery, and beverages. The clean-label trend and demand for natural stabilizers continue to support expansion in this segment. The dietary supplement industry represents a high-margin end-use, especially in the United States, Germany, Japan, and South Korea. Growth is fueled by rising consumer spending on preventive health, immunity boosters, and omega-3 fortification. This segment benefits from premium pricing and strong brand positioning.

Aquaculture is the fastest-growing end-use sector, expanding at nearly double-digit growth rates. Increasing seafood exports from countries such as Norway, Chile, Vietnam, India, and China are reinforcing demand for algae-based feed. Export-driven production models require high-quality, sustainable feed inputs, positioning algae as a preferred ingredient. Emerging industrial applications, including biodegradable packaging, wastewater treatment, and carbon capture systems, are expected to contribute more significantly post-2027. Sustainability mandates and circular economy policies are encouraging industrial adoption, especially in Europe and North America.

Explore more data points, trends and opportunities Download Free Sample Report

Algae Product Market Segmentations

By Product Type

- Nutraceuticals & Dietary Supplements

- Hydrocolloids (Agar, Carrageenan, Alginate)

- Animal & Aquaculture Feed

- Cosmetics & Personal Care

- Biofuels

- Pharmaceuticals & Biotechnology

- Bioplastics & Industrial Applications

By End-Use Industry

- Food & Beverage

- Dietary Supplements

- Aquaculture

- Cosmetics & Personal Care

- Pharmaceutical & Biotech

- Industrial & Environmental Applications

Regional Insights

North America

North America holds approximately 32% of the global algae product market share in 2025, with the United States representing the largest single-country market. Regional growth is primarily driven by high dietary supplement consumption, strong retail penetration of plant-based products, and expanding infant nutrition applications for algal DHA. Federal funding for biofuel innovation and carbon capture research further stimulates industrial algae projects. Canada is advancing algae cultivation for sustainable agriculture and wastewater treatment applications, supported by government-backed clean technology initiatives.

Asia-Pacific

Asia-Pacific leads globally with 35% market share in 2025 and is the fastest-growing region, registering approximately 10.2% CAGR. China dominates global spirulina production and export volumes due to cost-efficient cultivation and large-scale facilities. India is a significant producer of nutraceutical-grade algae, benefiting from favorable climatic conditions and export-oriented supplement manufacturing. Japan drives demand for functional foods, specialty extracts, and premium nutraceuticals. Rapid aquaculture expansion across Vietnam, Indonesia, and Thailand further accelerates feed demand. Rising middle-class health awareness and government support for biotechnology industries are additional regional growth drivers.

Europe

Europe accounts for roughly 22% of global revenue, with Germany, France, Norway, and the UK as leading markets. The primary regional growth driver is sustainability regulation under EU green policies, which encourage algae-based carbon capture, biofuel research, and biodegradable material development. Norway’s strong aquaculture industry fuels demand for algae-based feed inputs, while Germany and France lead omega-3 supplement adoption. Consumer preference for natural and organic products further supports nutraceutical growth.

Latin America

Latin America is an emerging growth region, led by Chile and Brazil. Chile’s salmon export industry is a major driver of algae feed imports, making aquaculture the primary regional demand engine. Brazil is gradually expanding algae cultivation for food and cosmetic applications. Increasing seafood export revenues and improvements in aquaculture technology continue to support steady market penetration.

Middle East & Africa

The Middle East & Africa region is strategically important despite its relatively smaller share. Israel is recognized for innovation in photobioreactor technology and desert-based algae cultivation systems. The UAE is investing in water-efficient algae farming aligned with food security strategies. In Africa, coastal countries are exploring seaweed cultivation for export markets. Growth drivers include water scarcity solutions, renewable energy diversification, and government-backed food security programs.

Key Players in the Algae Product Market

- Corbion

- DSM-Firmenich

- Cyanotech Corporation

- DIC Corporation

- BASF SE

- Cargill, Incorporated

- Roquette Frères

- Euglena Co., Ltd.

- Fuji Chemical Industries

- AlgaEnergy

- Algatech Ltd.

- Cellana Inc.

- Algenol Biotech

- Parry Nutraceuticals

- Seaweed Energy Solutions