Agricultural Sprayer Market Size

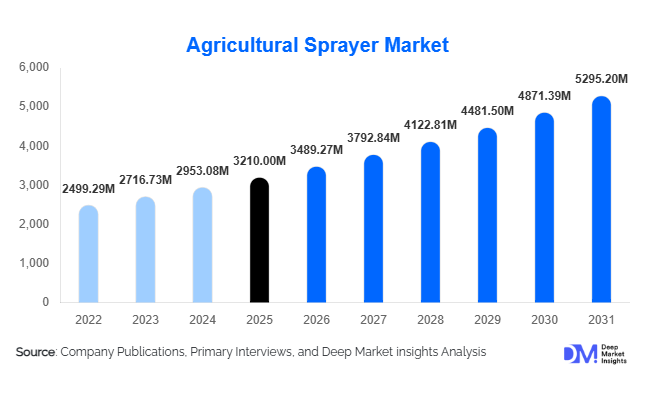

According to Deep Market Insights, the global agricultural sprayer market size was valued at USD 3,210 million in 2025 and is projected to grow from USD 3,489.27 million in 2026 to reach USD 5,295.20 million by 2031, expanding at a CAGR of 8.7% during the forecast period (2026–2031). Market growth is primarily driven by rising global food demand, increasing mechanization across developing agricultural economies, and the adoption of precision farming technologies that enhance input efficiency and crop productivity. Agricultural sprayers have evolved from basic mechanical equipment into technologically advanced systems integrating GPS guidance, automation, and data-driven application controls, enabling farmers to reduce chemical usage while improving yield outcomes.

Key Market Insights

- Precision agriculture adoption is accelerating globally, driving demand for GPS-enabled and variable-rate sprayers that optimize agrochemical usage.

- Asia-Pacific dominates the market due to rapid mechanization and government subsidy programs supporting farm equipment adoption.

- Drone-based aerial spraying is emerging as a high-growth segment, particularly in Asia and Latin America where labor shortages persist.

- Large commercial farms account for the largest equipment demand, benefiting from economies of scale and automation investments.

- Battery-operated and electric sprayers are gaining popularity due to sustainability goals and lower operational costs.

- Technological integration, including AI crop sensing and autonomous navigation, is reshaping modern spraying operations.

What are the latest trends in the agricultural sprayer market?

Precision and Smart Spraying Technologies Expanding Rapidly

The agricultural sprayer industry is witnessing a strong transition toward precision agriculture systems. Farmers increasingly deploy GPS-guided sprayers capable of variable-rate application, minimizing chemical waste and improving application accuracy. Smart sensors now detect crop density and weed presence, enabling targeted spraying that reduces agrochemical consumption by up to 30%. Integration with farm management platforms allows real-time data monitoring, predictive maintenance, and optimized spray scheduling. These capabilities are transforming sprayers into intelligent farm management tools rather than standalone machinery, attracting commercial farms seeking operational efficiency and sustainability compliance.

Rise of Agricultural Drone Spraying

Aerial spraying using agricultural drones is emerging as one of the most transformative trends. Drone sprayers enable uniform application across uneven terrain, plantations, and flooded fields where traditional equipment struggles to operate. Governments across Asia-Pacific are approving drone spraying frameworks to address labor shortages and improve productivity. Drone-based spraying also reduces water usage and operator exposure to chemicals, improving safety standards. Service-based drone spraying models are gaining traction, allowing small farmers to access advanced spraying technologies without large capital investments.

What are the key drivers in the agricultural sprayer market?

Rising Demand for Agricultural Productivity

Global population growth and limited arable land are pushing farmers toward higher productivity per hectare. Efficient spraying plays a vital role in pest control, nutrient delivery, and crop protection, directly impacting yield performance. High-value crops such as fruits, vegetables, and oilseeds require precise spraying cycles, accelerating equipment adoption worldwide. Export-oriented agriculture further reinforces demand for standardized spraying practices that meet global quality and safety regulations.

Mechanization Driven by Labor Shortages

Agricultural labor shortages in developed markets such as North America and Europe, along with rising labor costs in emerging economies, are accelerating mechanization adoption. Tractor-mounted and self-propelled sprayers significantly reduce manual workload while improving operational efficiency. Government incentives supporting farm mechanization programs are further strengthening equipment penetration across rural economies.

What are the restraints for the global market?

High Initial Equipment Investment

Advanced agricultural sprayers equipped with automation, sensors, and digital platforms involve high upfront costs, limiting adoption among smallholder farmers. Financing challenges and limited access to credit in developing countries slow penetration despite long-term operational savings offered by modern equipment.

Regulatory and Environmental Compliance Challenges

Strict environmental regulations governing pesticide application and chemical drift require manufacturers to continuously upgrade equipment designs. Compliance requirements increase development costs and create barriers for smaller manufacturers. Regional differences in regulatory standards also complicate global product standardization and distribution.

What are the key opportunities in the agricultural sprayer industry?

Expansion of Precision Agriculture Ecosystems

The growing adoption of digital agriculture presents significant opportunities for sprayer manufacturers. Integration with IoT platforms, AI crop analytics, and satellite data enables advanced decision-making capabilities. Companies offering connected spraying solutions bundled with farm software services are expected to capture premium market segments and recurring revenue streams.

Sustainable and Low-Chemical Application Solutions

Environmental sustainability initiatives are encouraging adoption of electrostatic and ultra-low-volume spraying systems that reduce chemical drift and environmental contamination. Regulatory pressure in Europe and North America is accelerating equipment replacement cycles, creating opportunities for technology-driven manufacturers focusing on eco-efficient spraying solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3210 Million |

| Market Size in 2026 | USD 3489.27 Million |

| Market Size in 2031 | USD 5295.20 Million |

| CAGR | 8.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global agricultural sprayer market demonstrates strong product diversification driven by evolving farm structures, precision agriculture adoption, and increasing demand for efficient crop protection solutions. Hydraulic sprayers continue to dominate the market, accounting for approximately 42% of total demand, primarily due to their operational versatility, cost-effectiveness, and compatibility with a wide range of agrochemical applications including herbicides, pesticides, and liquid fertilizers. Their adaptability across varying farm sizes and crop types makes them the preferred choice among both developing and developed agricultural economies. The continued expansion of row crop cultivation and increasing emphasis on uniform chemical distribution further reinforce the dominance of hydraulic systems.Tractor-mounted sprayers represent the most widely adopted mobility configuration globally, supported by rising farm mechanization levels and increasing tractor penetration across emerging markets. As farm sizes expand and operational efficiency becomes a priority, farmers favor tractor-mounted equipment that offers scalability, higher tank capacity, and improved coverage efficiency. The segment’s leadership is primarily driven by its balance between affordability and performance, allowing farmers to upgrade spraying capacity without significant capital investment.Self-propelled sprayers are witnessing accelerated adoption among large-scale commercial farming operations where operational efficiency, speed, and automation capabilities are critical. These machines provide higher ground clearance, advanced boom stability, GPS guidance, and variable-rate technology, enabling precise chemical application while minimizing input waste. Growing labor shortages and rising operational costs are encouraging large farms to invest in technologically advanced equipment capable of covering extensive acreage within shorter spraying windows.Aerial and drone sprayers are emerging as the fastest-growing product category, reflecting the industry’s transition toward digital agriculture and precision farming. Drone-based spraying solutions are particularly gaining momentum in regions characterized by fragmented landholdings, difficult terrain, and labor constraints. Their ability to reduce chemical exposure risks, lower water consumption, and provide targeted application enhances adoption across Asia-Pacific and parts of Latin America. Advancements in battery efficiency, AI-based mapping, and regulatory approvals are expected to further accelerate penetration of aerial spraying technologies during the forecast period.

Application Insights

Application-based demand within the agricultural sprayer market is primarily influenced by evolving crop protection requirements and changing agronomic practices. Herbicide application remains the largest use case, contributing nearly 37% of total market demand, driven by rising weed resistance challenges and the growing need to protect crop yields amid shrinking arable land availability. Increasing adoption of herbicide-tolerant crop varieties and conservation tillage practices further strengthens the leading position of this segment, as farmers rely heavily on efficient spraying technologies to maintain productivity.Fungicide and pesticide spraying applications maintain significant market presence, particularly within horticulture, fruit cultivation, and plantation crops where frequent and precise treatment cycles are essential to prevent yield loss. Climate variability and increasing incidences of crop diseases have intensified reliance on advanced spraying equipment capable of uniform coverage and optimized droplet control. Precision spraying technologies are increasingly deployed to minimize chemical overuse while maintaining effective pest and disease management.Fertilizer and nutrient spraying applications are expanding steadily as farmers adopt foliar nutrition techniques to enhance crop quality, nutrient absorption efficiency, and yield performance. The growing focus on micronutrient management and balanced fertilization practices supports increased use of sprayers for liquid nutrient delivery, particularly in high-value crops. This trend aligns with precision agriculture strategies aimed at maximizing input efficiency while reducing environmental impact.Biological input spraying is gaining notable momentum as sustainable agriculture practices and organic farming initiatives expand globally. The rising adoption of bio-based crop protection products and microbial solutions requires specialized spraying systems capable of gentle and precise application. Increasing regulatory pressure to reduce chemical pesticide usage and growing consumer demand for residue-free produce continue to drive the adoption of sprayers suitable for biological formulations.

Distribution Channel Insights

The agricultural sprayer market distribution landscape remains strongly anchored in traditional sales networks while gradually integrating digital commerce channels. Agricultural equipment dealers dominate distribution channels with nearly 48% market share, as farmers rely extensively on localized dealer ecosystems for product demonstrations, after-sales services, spare parts availability, financing assistance, and technical consultation. The trust-based relationships established between farmers and regional dealers significantly influence purchasing decisions, particularly in emerging markets.OEM direct sales continue to play a critical role in developed agricultural economies where large commercial farms procure equipment directly from manufacturers to access customized configurations, advanced technologies, and long-term service contracts. Direct engagement enables manufacturers to integrate precision agriculture solutions, telematics systems, and performance monitoring technologies tailored to large-scale farming operations.Cooperative procurement models and government-supported purchasing programs remain vital distribution channels across developing regions, improving mechanization accessibility for small and medium-sized farmers. Subsidy-driven procurement initiatives reduce capital barriers and encourage adoption of modern spraying equipment, contributing to increased agricultural productivity and rural mechanization levels.Online agricultural platforms are gradually expanding their presence, particularly for small-capacity, handheld, and battery-operated sprayers. Digital marketplaces are improving product accessibility, price transparency, and comparison capabilities, especially among younger farmers and technologically aware agricultural entrepreneurs. The integration of e-commerce with rural logistics networks is expected to strengthen this channel’s contribution over the coming years.

End-Use Insights

End-use demand patterns in the agricultural sprayer market are shaped by farm size distribution, labor availability, and production intensity. Large commercial farms account for the largest share of agricultural sprayer demand, representing approximately 41% of global usage. The leading position of this segment is primarily driven by extensive land holdings, continuous crop cycles, and the need for high-capacity equipment capable of delivering consistent and timely spraying operations. These farms increasingly adopt automated and precision-enabled sprayers to reduce input costs and improve operational efficiency.Small and medium farms are progressively adopting compact, battery-operated, and portable sprayers supported by government subsidy programs and rural mechanization initiatives. Rising awareness regarding crop protection efficiency and increasing access to affordable equipment financing are enabling smaller farmers to transition from manual spraying methods to mechanized solutions, improving productivity and safety outcomes.Contract spraying services are emerging as one of the fastest-growing end-use categories, allowing farmers to outsource spraying operations and minimize upfront capital investments. The expansion of service-based agricultural models is particularly evident in regions facing labor shortages or seasonal workforce constraints. Professional spraying contractors utilize advanced machinery and precision technologies, ensuring optimized chemical usage and consistent application quality.Greenhouses and controlled environment agriculture represent high-growth end users requiring precision application systems tailored for enclosed farming conditions. Increasing investments in protected cultivation, hydroponics, and vertical farming are driving demand for specialized sprayers capable of fine droplet control, reduced chemical drift, and uniform coverage within controlled environments.

Explore more data points, trends and opportunities Download Free Sample Report

Agricultural Sprayer Market Segmentations

By Product Type

- Hydraulic Sprayers

- Pneumatic Sprayers

- Centrifugal Sprayers

- Electrostatic Sprayers

- Aerial & Drone Sprayers

By Mobility Type

- Handheld Sprayers

- Backpack Sprayers

- Tractor-Mounted Sprayers

- Trailed Sprayers

- Self-Propelled Sprayers

- Drone-Based Sprayers

By Application

- Herbicide Application

- Fungicide Application

- Insecticide Application

- Fertilizer & Nutrient Spraying

- Biological Crop Protection

By Distribution Channel

- OEM Direct Sales

- Agricultural Equipment Dealers

- Cooperatives & Government Procurement Programs

- Online Agricultural Platforms

By End-Use

- Large Commercial Farms

- Small & Medium Farms

- Contract Spraying Service Providers

- Greenhouses & Controlled Environment Agriculture

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest share of the agricultural sprayer market at approximately 38% in 2025, supported by rapid agricultural modernization, expanding food demand, and strong policy-driven mechanization programs. China and India remain the primary growth engines due to large agricultural workforces transitioning toward mechanized farming practices. Government subsidies promoting farm equipment adoption, rising labor costs, and increasing awareness of crop protection efficiency significantly drive regional demand. China leads global adoption of drone spraying technologies supported by favorable regulatory frameworks and technological innovation, while India experiences rapid expansion through subsidy schemes, custom hiring centers, and increasing penetration of battery-operated sprayers among smallholder farmers. Australia and Japan contribute through advanced precision agriculture adoption, high technology integration, and strong investment in smart farming solutions, collectively strengthening regional market leadership.

North America

North America accounts for nearly 24% of global agricultural sprayer market share, led primarily by the United States and supported by highly commercialized farming systems. Large farm sizes and high mechanization levels create sustained demand for high-capacity and technologically advanced spraying equipment. Regional growth is driven by increasing adoption of autonomous machinery, GPS-guided sprayers, and data-driven farm management platforms aimed at optimizing input efficiency and reducing operational costs. Strong replacement demand for aging equipment, combined with rising investments in precision agriculture and sustainability-focused farming practices, continues to support market expansion. Additionally, labor shortages and rising wage pressures encourage farmers to adopt automated spraying technologies that enhance productivity and operational consistency.

Europe

Europe represents approximately 21% of global market demand, with Germany, France, and the United Kingdom leading adoption due to technologically advanced agricultural systems and stringent environmental regulations. Regional growth is strongly influenced by policies promoting sustainable agriculture, reduced pesticide usage, and environmentally responsible farming practices under evolving regulatory frameworks. Farmers increasingly invest in precision spraying technologies, electrostatic systems, and variable-rate application equipment to comply with regulatory standards while maintaining productivity. The region’s strong emphasis on carbon reduction, biodiversity protection, and resource efficiency further accelerates adoption of advanced sprayers capable of minimizing chemical drift and optimizing application accuracy.

Latin America

Latin America demonstrates robust growth potential, primarily driven by Brazil and Argentina, where large-scale soybean, corn, and sugarcane cultivation dominates agricultural output. Export-oriented farming models and expanding farm consolidation trends encourage adoption of high-capacity sprayers capable of efficiently covering extensive farmland areas. Regional growth is further supported by increasing investment in modern agricultural machinery, rising global commodity demand, and improved access to financing for commercial farmers. Precision agriculture adoption is gradually increasing as producers seek to enhance yield performance and reduce input wastage across large agricultural landscapes.

Middle East & Africa

The Middle East & Africa agricultural sprayer market is witnessing steady expansion supported by irrigation development projects, food security initiatives, and growing investment in agricultural modernization. South Africa leads regional adoption due to relatively advanced commercial farming infrastructure and increasing mechanization levels. Gulf countries are investing heavily in controlled agriculture, smart irrigation systems, and mechanized farming technologies to improve domestic food production capacity amid water scarcity challenges. Across Africa, rising government and international development programs aimed at improving agricultural productivity are encouraging adoption of affordable and portable spraying solutions, gradually strengthening regional market penetration.

Key Players in the Agricultural Sprayer Market

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- CLAAS Group

- EXEL Industries

- STIHL Group

- Yamaha Motor Co., Ltd.

- Mahindra & Mahindra Ltd.

- Hardi International A/S

- Buhler Industries Inc.

- Amazone H. Dreyer GmbH & Co. KG

- Kuhn Group

- DJI Agriculture

- Escorts Kubota Limited