Agricultural Inputs Market Size

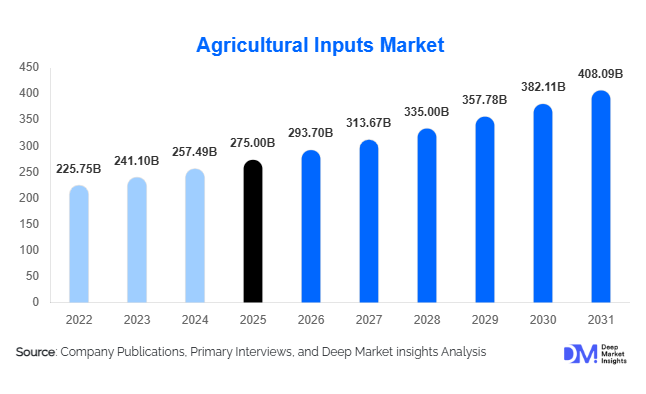

According to Deep Market Insights, the global agricultural inputs market size was valued at USD 275.0 billion in 2025 and is projected to grow from USD 293.7 billion in 2026 to reach USD 408.09 billion by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031).The agricultural inputs market growth is primarily driven by rising global food demand, increasing adoption of high-yield crop varieties, and the growing integration of precision farming technologies. Additionally, government subsidies and support programs across emerging economies are improving accessibility to fertilizers, seeds, and crop protection products, further strengthening market expansion.

Key Market Insights

- Fertilizers dominate the agricultural inputs market, accounting for the largest share due to their critical role in enhancing crop productivity and soil fertility.

- Asia-Pacific leads the global market, supported by large-scale agricultural activities in China and India and strong government subsidies.

- Bio-based inputs are gaining traction, driven by increasing environmental regulations and demand for sustainable farming practices.

- Precision agriculture technologies are transforming input utilization, enabling efficient use of fertilizers and pesticides.

- Retail agro-dealers remain the primary distribution channel, especially in developing economies with fragmented farming communities.

- Emerging markets in Africa and Latin America are witnessing rapid growth due to agricultural modernization and export-oriented farming.

What are the latest trends in the agricultural inputs market?

Shift Toward Sustainable and Bio-Based Inputs

The agricultural inputs market is undergoing a major transition toward sustainability, with increasing demand for biofertilizers, biopesticides, and organic soil conditioners. Governments in Europe and North America are imposing strict regulations on chemical inputs, encouraging farmers to adopt eco-friendly alternatives. This shift is further supported by rising consumer demand for organic food products, pushing farmers to reduce chemical usage. Companies are investing heavily in R&D to develop microbial-based fertilizers and plant growth enhancers that improve soil health while maintaining productivity. The integration of sustainability certifications and carbon footprint reduction initiatives is also influencing purchasing decisions across large-scale farming operations.

Integration of Precision Farming and Digital Technologies

Precision agriculture is rapidly transforming how inputs are applied in farming systems. Technologies such as GPS-guided machinery, IoT sensors, and AI-driven analytics are enabling farmers to optimize input usage based on real-time field data. This reduces wastage and improves crop yield, making high-efficiency inputs more attractive. Drone-based spraying and satellite monitoring are also gaining popularity, particularly in large farms across North America and Brazil. Digital platforms are further enabling farmers to access advisory services, weather forecasts, and input recommendations, enhancing decision-making and operational efficiency.

What are the key drivers in the agricultural inputs market?

Rising Global Food Demand

The increasing global population and changing dietary patterns are driving demand for higher agricultural productivity. Staple crops such as wheat, rice, and corn require consistent input usage to maintain yield levels. This has led to increased adoption of fertilizers, improved seeds, and crop protection chemicals, particularly in emerging economies where food security remains a priority.

Government Subsidies and Policy Support

Governments across countries such as India, China, and Brazil are providing subsidies on fertilizers and seeds to support farmers. These initiatives are improving affordability and encouraging higher consumption of agricultural inputs. Policies promoting irrigation infrastructure and mechanization are also contributing to market growth.

Technological Advancements in Agriculture

The adoption of advanced farming technologies, including genetically modified seeds and controlled-release fertilizers, is driving market expansion. These innovations improve crop yield, reduce input wastage, and enhance resilience to climate variability, making them increasingly popular among farmers.

What are the restraints for the global market?

Volatility in Raw Material Prices

The production of fertilizers depends heavily on raw materials such as natural gas and mined minerals. Fluctuations in these prices impact production costs and final product pricing, affecting both manufacturers and farmers. This volatility can lead to reduced input usage, particularly in price-sensitive markets.

Stringent Environmental Regulations

Strict regulations on chemical fertilizers and pesticides, especially in Europe, are limiting the growth of conventional inputs. Compliance with these regulations requires significant investment in product reformulation and testing, which can slow down innovation and market expansion.

What are the key opportunities in the agricultural inputs industry?

Expansion in Emerging Markets

Emerging economies in Asia-Pacific, Latin America, and Africa present significant growth opportunities due to increasing agricultural activities and government investments in rural development. Countries such as India, Brazil, and Nigeria are focusing on improving agricultural productivity, creating strong demand for inputs.

Growth of Bio-Based and Specialty Inputs

The rising demand for sustainable agriculture is creating opportunities for biofertilizers, biopesticides, and specialty nutrients. These products offer higher margins and align with regulatory trends, making them attractive for both new entrants and established players.

Digital Agriculture and Smart Input Solutions

The integration of digital technologies with agricultural inputs is opening new avenues for growth. Smart fertilizers and precision-compatible crop protection products are gaining popularity, enabling companies to offer value-added solutions and differentiate their offerings in a competitive market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 275 Billion |

| Market Size in 2026 | USD 293.7 Billion |

| Market Size in 2031 | USD 408.09 Billion |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The agricultural inputs market is structurally anchored by fertilizers, which continue to dominate the global landscape, accounting for approximately 38% of the total market share in 2025. This dominance is fundamentally linked to the indispensable role fertilizers play in replenishing soil nutrients and enhancing crop productivity across both developed and developing agricultural systems. Nitrogen-based fertilizers, in particular, remain the cornerstone of this segment due to their immediate and visible impact on plant growth, chlorophyll production, and overall yield optimization. The increasing global demand for staple crops such as rice, wheat, and maize has further intensified the reliance on nitrogen-intensive formulations, reinforcing their market leadership.Beyond fertilizers, the seeds segment has evolved into a highly dynamic and innovation-driven category. Hybrid and genetically modified seeds are witnessing widespread adoption due to their ability to deliver higher yields, improved resistance to pests and diseases, and better tolerance to environmental stressors such as drought and salinity. The leading driver for this segment is the growing need to maximize productivity per hectare amid shrinking arable land and increasing food demand. Advancements in biotechnology and breeding techniques are also accelerating the development of climate-resilient seed varieties, making them increasingly attractive to farmers seeking consistent output in unpredictable weather conditions.Biostimulants and organic fertilizers are also gaining momentum as part of the broader transition toward sustainable agriculture. These products enhance nutrient uptake, improve soil health, and support long-term agricultural productivity. While still a smaller portion of the overall market, their growth trajectory is robust, driven by increasing consumer demand for organic produce and stricter environmental regulations. Collectively, the product type landscape is characterized by a balance between conventional high-efficiency inputs and emerging sustainable solutions, with innovation serving as the central force shaping future growth.

Application Insights

From an application standpoint, soil treatment continues to lead the agricultural inputs market, accounting for nearly 45% of the total share. This segment’s leadership is driven by its foundational role in determining crop health, nutrient availability, and overall yield outcomes. Soil treatment applications involve the incorporation of fertilizers, soil conditioners, and microbial solutions directly into the soil, ensuring optimal nutrient absorption and root development. The leading driver for this segment is the increasing awareness among farmers regarding soil degradation and the need for balanced nutrient management to sustain long-term productivity.Seed treatment has emerged as another important application area, particularly for commercial and high-value crop cultivation. This technique involves coating seeds with protective chemicals or biological agents to enhance germination rates and protect against early-stage pests and diseases. The leading driver for seed treatment adoption is the need to ensure uniform crop establishment and reduce input costs associated with replanting and early crop failures. As farmers increasingly prioritize efficiency and risk mitigation, seed treatment is becoming a standard practice in modern agriculture.Fertigation and advanced application methods such as drone-based spraying are redefining the way agricultural inputs are delivered. Fertigation, which combines irrigation with nutrient application, enables precise control over nutrient delivery and reduces wastage. Drone-based applications, on the other hand, offer unparalleled efficiency in covering large areas and accessing difficult terrains. These advanced methods are driven by the broader shift toward precision agriculture, where technology is leveraged to optimize input usage, reduce environmental impact, and enhance overall farm productivity. As digital agriculture continues to evolve, these application techniques are expected to gain further prominence.

Distribution Channel Insights

The distribution landscape of the agricultural inputs market is dominated by retail agro-dealers, which account for approximately 50% of total market sales. These local dealers serve as the primary point of contact for farmers, particularly in developing economies where access to formal supply chains may be limited. The leading driver for this segment is the strong trust-based relationship between farmers and agro-dealers, who not only provide products but also offer critical advisory services on crop management, input selection, and application techniques. This personalized support plays a crucial role in influencing purchasing decisions and ensuring effective product utilization.Cooperatives also play a significant role in the distribution ecosystem, particularly in regions with strong agricultural communities. These organizations facilitate collective procurement, allowing farmers to access inputs at competitive prices while benefiting from shared knowledge and resources. The leading driver for cooperative-based distribution is the need to enhance affordability and accessibility for smallholder farmers, who often face financial and logistical constraints.In recent years, online platforms and agri-tech marketplaces have emerged as transformative forces in the distribution landscape. These digital channels enable direct-to-farmer sales, improve price transparency, and provide access to a wider range of products. The rapid growth of this segment is driven by increasing internet penetration, smartphone adoption, and the digitization of agricultural services. Farmers are increasingly leveraging online platforms to compare products, access expert advice, and make informed purchasing decisions. As digital ecosystems continue to expand, online distribution channels are expected to play an increasingly important role in shaping the future of agricultural input supply chains.

End-Use Insights

Crop production remains the dominant end-use segment within the agricultural inputs market, underpinned by the global imperative to ensure food security and meet the nutritional needs of a growing population. Cereals and grains account for the largest share within this segment, driven by their status as staple foods across most regions. The leading driver for this segment is the continuous demand for high-yield crop production to support population growth, urbanization, and changing dietary patterns. Governments and agricultural organizations worldwide are also investing heavily in initiatives aimed at improving cereal productivity, further reinforcing this segment’s dominance.Controlled-environment agriculture, including greenhouses and vertical farming, represents a niche but rapidly expanding segment. This approach to farming involves the use of controlled conditions to optimize crop growth, often in urban or resource-constrained environments. The leading driver for this segment is the need to produce high-quality crops with minimal environmental impact, particularly in regions facing land and water scarcity. Controlled-environment systems require specialized inputs such as water-soluble fertilizers, precision nutrient solutions, and bio-based crop protection products, creating new opportunities for innovation within the agricultural inputs market.Additionally, the increasing integration of technology in agriculture is influencing end-use patterns, with farmers adopting data-driven approaches to optimize input usage and improve yield outcomes. This shift toward smart farming is expected to further diversify end-use applications and drive demand for advanced agricultural inputs tailored to specific crop and environmental conditions.

Explore more data points, trends and opportunities Download Free Sample Report

Agricultural Inputs Market Segmentations

By Product Type

- Seeds

- Fertilizers

- Crop Protection Chemicals

- Soil Conditioners & Amendments

- Plant Growth Regulators

- Irrigation Inputs

- Adjuvants & Crop Enhancers

By Crop Type

- Cereals & Grains

- Oilseeds & Pulses

- Fruits & Vegetables

- Plantation Crops

- Turf & Ornamentals

By Application

- Soil Treatment

- Foliar Spray

- Seed Treatment

- Fertigation

- Drone-Based Application

By Farming Practice

- Conventional Agriculture

- Organic Agriculture

- Precision Farming

- Sustainable/Regenerative Agriculture

By Distribution Channel

- Direct Sales

- Retail Agro-Dealers

- Cooperatives

- Online Platforms

- Agri-Tech Marketplaces

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global agricultural inputs market, accounting for approximately 40% of the total share in 2025. The region’s leadership is primarily driven by the large agricultural base and high population density in countries such as China and India, which necessitate intensive farming practices to meet food demand. China’s extensive fertilizer production capacity ensures a steady supply of inputs, while India’s subsidy-driven consumption model significantly boosts fertilizer usage among farmers. In addition, the region is witnessing rapid adoption of hybrid seeds and crop protection solutions, particularly in emerging economies.Key growth drivers in Asia-Pacific include increasing government support for agricultural modernization, rising awareness of soil health management, and the expansion of high-value crop cultivation. Southeast Asian countries such as Indonesia and Vietnam are experiencing strong growth due to the increasing cultivation of cash crops such as palm oil, rubber, and coffee. Furthermore, the growing penetration of digital agriculture platforms and precision farming technologies is enhancing input efficiency and driving market expansion. Climate variability and the need for sustainable farming practices are also encouraging the adoption of bio-based inputs, further diversifying the regional market.

North America

North America holds approximately 22% of the global agricultural inputs market, characterized by highly advanced farming practices and strong technological integration. The United States leads the region, with widespread adoption of genetically modified seeds, precision agriculture, and data-driven farm management systems. The leading drivers for growth in this region include the continuous innovation in agricultural biotechnology, the increasing use of automation and digital tools, and the strong presence of major agribusiness companies.Additionally, the region’s focus on maximizing productivity and efficiency is driving demand for premium agricultural inputs, including specialized fertilizers and advanced crop protection products. Environmental sustainability is also a key consideration, with farmers increasingly adopting practices that reduce chemical usage and improve soil health. Government policies and research initiatives aimed at promoting sustainable agriculture further support market growth in North America.

Europe

Europe accounts for approximately 18% of the global market share, with a strong emphasis on sustainability and environmental stewardship. Countries such as Germany and France are at the forefront of adopting eco-friendly agricultural practices, driven by stringent regulatory frameworks and consumer demand for organic products. The leading drivers for growth in Europe include the increasing adoption of bio-based inputs, the implementation of integrated pest management systems, and the expansion of organic farming.The European Union’s policies aimed at reducing chemical pesticide usage and promoting sustainable agriculture are significantly influencing market dynamics. Farmers are increasingly transitioning toward biological solutions and precision farming techniques to comply with regulations and maintain productivity. Additionally, the region’s well-established research and development infrastructure is fostering innovation in agricultural inputs, particularly in the development of environmentally friendly products.

Latin America

Latin America is one of the fastest-growing regions in the agricultural inputs market, with a projected compound annual growth rate exceeding 7%. The region’s growth is largely driven by large-scale commercial farming in countries such as Brazil and Argentina, which are major exporters of crops such as soybeans, corn, and sugarcane. The leading drivers for growth include strong global demand for agricultural commodities, the availability of vast arable land, and the increasing adoption of modern farming techniques.In addition, favorable climatic conditions and government support for agricultural expansion are contributing to the region’s growth. Farmers are increasingly investing in high-quality seeds, fertilizers, and crop protection products to enhance yield and maintain competitiveness in global markets. The expansion of agribusiness operations and the integration of advanced technologies are further strengthening the demand for agricultural inputs in Latin America.

Middle East & Africa

The Middle East and Africa region is emerging as a high-growth market for agricultural inputs, driven by increasing investments in agricultural infrastructure and modernization efforts. Countries such as South Africa and Nigeria are focusing on improving agricultural productivity to reduce dependence on food imports and enhance food security. The leading drivers for growth in this region include government initiatives to support farming, the adoption of irrigation technologies, and the increasing availability of financing for agricultural activities.Water scarcity and challenging climatic conditions are also prompting the adoption of efficient input solutions, such as water-soluble fertilizers and drought-resistant seeds. Additionally, international development programs and private sector investments are playing a crucial role in advancing agricultural practices and improving access to inputs. As the region continues to address structural challenges and invest in agricultural development, the demand for agricultural inputs is expected to grow significantly.

Key Players in the Agricultural Inputs Market

- Bayer AG

- Syngenta Group

- Corteva Agriscience

- BASF SE

- Nutrien Ltd.

- Yara International

- CF Industries

- The Mosaic Company

- UPL Limited

- FMC Corporation

- Sumitomo Chemical

- ICL Group

- K+S AG

- Nufarm Ltd.

- Adama Agricultural Solutions