Frozen Dough Additives Market Size

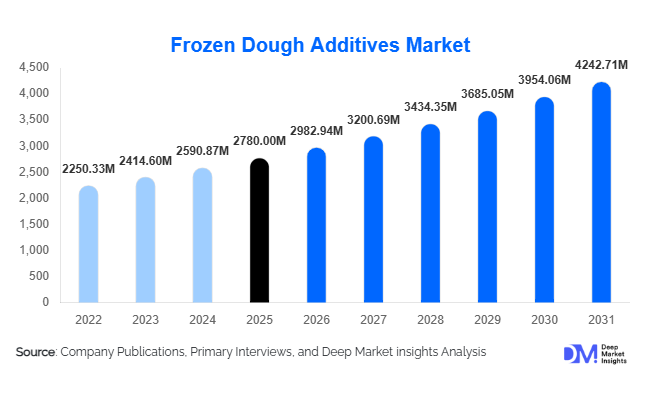

According to Deep Market Insights, the global frozen dough additives market size was valued at USD 2,780 million in 2025 and is projected to grow from USD 2,982.94 million in 2026 to reach USD 4,242.71 million by 2031, expanding at a CAGR of 7.3% during the forecast period (2026–2031). Market growth is primarily driven by rising demand for frozen bakery products, increasing automation in industrial baking, and the growing adoption of freeze–thaw stable dough solutions across quick service restaurants (QSRs) and retail bakery chains worldwide.

Key Market Insights

- Enzyme-based additives are replacing traditional chemical dough improvers, supporting clean-label bakery formulations globally.

- Industrial bakeries account for the largest consumption share, driven by centralized production and frozen dough logistics models.

- Europe dominates global demand due to strong frozen bakery traditions and export-oriented pastry manufacturing.

- Asia-Pacific is the fastest-growing region, supported by expanding cold-chain infrastructure and urban food consumption patterns.

- Quick service restaurant expansion is accelerating standardized frozen dough adoption worldwide.

- Technological innovation in enzymes and multifunctional improvers is reshaping competitive differentiation among ingredient manufacturers.

What are the latest trends in the frozen dough additives market?

Shift Toward Clean-Label and Enzyme-Based Solutions

The frozen dough additives market is witnessing a major transition toward enzyme-based solutions that replace synthetic oxidizers and emulsifiers. Consumers increasingly demand natural ingredient labels, prompting bakery manufacturers to reformulate frozen dough recipes using biological processing aids. Enzymes such as amylases, lipases, and xylanases improve dough elasticity, gas retention, and freeze–thaw tolerance without requiring chemical additives. Manufacturers are investing heavily in biotechnology platforms to develop multifunctional enzyme blends that deliver improved texture stability while meeting regulatory and consumer expectations for transparency. Clean-label positioning has also enabled suppliers to command premium pricing and strengthen long-term contracts with industrial bakery customers.

Automation and Centralized Frozen Dough Manufacturing

Industrial bakeries are rapidly adopting centralized manufacturing models in which dough is produced in large facilities, frozen, and distributed globally for final baking. This trend reduces labor dependency and ensures consistent product quality across retail outlets and foodservice locations. Frozen dough additives play a critical role in enabling this model by stabilizing fermentation activity and maintaining structural integrity during storage and transport. Automation technologies such as precision mixing, automated dosing systems, and AI-assisted formulation optimization are further increasing additive efficiency and encouraging bakeries to adopt advanced improver systems.

What are the key drivers in the frozen dough additives market?

Rising Demand for Convenience Bakery Products

Urbanization and changing lifestyles are significantly increasing demand for ready-to-bake and partially prepared bakery products. Frozen dough allows retailers and restaurants to offer fresh-baked products without extensive preparation time or skilled labor. Additives ensure consistent dough performance after freezing, making them essential for scalable production. Supermarkets and café chains are increasingly installing in-store baking systems, further boosting additive consumption.

Expansion of Quick Service Restaurants and Retail Bakery Chains

The rapid expansion of global QSR brands and convenience retail outlets has increased demand for standardized bakery inputs. Frozen dough enables centralized manufacturing and uniform product quality across thousands of outlets. Additive suppliers benefit from recurring demand as restaurant chains adopt customized formulations designed for operational efficiency, shelf-life extension, and consistent sensory performance.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in vegetable oils, fermentation substrates, and hydrocolloid feedstocks affect production costs for emulsifiers and dough conditioners. Price instability can compress margins and create procurement challenges for additive manufacturers, especially during agricultural supply disruptions.

Regulatory Pressure and Reformulation Costs

Increasing regulatory scrutiny on certain chemical improvers requires manufacturers to invest in research and development for compliant alternatives. Reformulation processes can be costly and time-intensive, particularly for small and mid-sized ingredient suppliers adapting to clean-label trends.

What are the key opportunities in the frozen dough additives industry?

Emerging Market Cold-Chain Expansion

Rapid investment in refrigerated logistics across Asia-Pacific, the Middle East, and Latin America is creating new demand for frozen bakery solutions. As modern retail formats expand into urban and semi-urban markets, frozen dough adoption rises, directly increasing additive consumption. Governments supporting food processing modernization are indirectly accelerating market expansion.

Customized Functional Additive Systems

Ingredient suppliers are increasingly collaborating with bakery manufacturers to develop application-specific improver blends tailored to pizza dough, laminated pastries, and specialty breads. These customized systems increase switching costs and create long-term supply agreements. Innovation in multifunctional additives that combine emulsification, enzymatic activity, and moisture retention represents a major growth opportunity.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2780 Million |

| Market Size in 2026 | USD 2982.94 Million |

| Market Size in 2031 | USD 4242.71 Million |

| CAGR | 7.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Additive Type Insights

The frozen dough additives market demonstrates strong diversification across additive categories, with enzymes emerging as the leading segment, accounting for approximately 31% of the global market share in 2025. The dominance of enzymes is primarily driven by their ability to improve dough machinability, fermentation tolerance, texture stability, and shelf-life performance while supporting clean-label product development. As bakery manufacturers increasingly prioritize ingredient transparency and reduced chemical dependency, enzyme-based solutions provide multifunctional performance advantages that align with evolving consumer expectations and regulatory trends. Continuous advancements in enzyme engineering have further enhanced freeze–thaw stability, enabling consistent product quality across industrial-scale frozen dough production.Emulsifiers continue to maintain significant adoption across industrial bread manufacturing due to their effectiveness in strengthening gluten networks, improving gas retention, and delivering uniform crumb structure. Their ability to enhance dough tolerance during mechanical processing and frozen storage makes them indispensable in high-volume bakery operations. Hydrocolloids and dough conditioners are gaining traction, particularly in premium frozen bakery applications where moisture retention, softness preservation, and extended freshness are critical differentiators. These additives help maintain structural integrity after thawing and baking, addressing quality challenges associated with frozen distribution. Preservatives remain essential for ensuring microbiological stability and extending product shelf life, especially within export-oriented frozen bakery supply chains that require long transit times and temperature fluctuations. Increasing globalization of frozen bakery trade continues to sustain demand for preservation technologies that maintain safety and quality standards across international markets.

Application Insights

Bread and rolls represent the dominant application segment, accounting for nearly 34% share of total demand, supported by their high consumption frequency, standardized production processes, and widespread adoption in both retail and foodservice channels. The leading position of this segment is driven by the need for consistent volume, crumb softness, and freeze–thaw resilience in mass-produced bakery items, which requires advanced additive formulations to maintain performance across large-scale production cycles. Industrial bakeries increasingly rely on additive systems that enhance dough stability while minimizing waste and operational variability.Pizza dough has emerged as one of the fastest-growing application areas, fueled by expanding global fast-food consumption and the rapid growth of delivery-oriented dining models. Additives play a critical role in maintaining elasticity, fermentation control, and baking performance after frozen storage, ensuring standardized product outcomes across quick service restaurant networks. Viennoiserie products, including croissants and Danish pastries, require highly specialized additive solutions to preserve laminated dough structures and butter layer separation during freezing and thawing processes. These technical requirements contribute to higher-value additive adoption within premium bakery segments. Meanwhile, specialty artisan frozen dough is developing into a premium niche category as retailers and bakery chains seek differentiation through craft-style offerings that combine convenience with artisanal quality attributes, driving demand for customized additive formulations that replicate traditional baking characteristics.

Distribution Channel Insights

Direct industrial supply channels dominate the frozen dough additives market, accounting for approximately 57% of global sales, reflecting strong long-term procurement relationships between additive manufacturers and large-scale industrial bakeries. The leadership of this channel is driven by the need for formulation consistency, technical collaboration, and integrated supply agreements that ensure stable production performance. Industrial customers increasingly prefer direct partnerships that provide application support, customized solutions, and ongoing product optimization rather than transactional ingredient purchasing.Ingredient distributors continue to play an important role, particularly in emerging markets where small and mid-sized bakeries depend on regional distribution networks for ingredient accessibility and technical guidance. These distributors facilitate market penetration by bridging logistical and knowledge gaps in developing bakery ecosystems. Bakery solution providers offering formulation expertise, troubleshooting services, and performance-based ingredient systems are gaining strategic importance as bakeries transition toward efficiency-focused operations. The shift from commodity sourcing to solution-driven procurement models is reshaping distribution dynamics, encouraging collaborative innovation between additive suppliers and bakery manufacturers.

End-Use Insights

Industrial bakeries account for the largest share of frozen dough additive consumption, representing approximately 46% of total demand. The leading position of this segment is driven by centralized production models supplying supermarkets, convenience stores, and foodservice operators with standardized bakery products. These facilities rely heavily on additives to ensure scalability, extended storage stability, and uniform product quality across multiple distribution channels. Automation and high-throughput production environments further increase dependence on performance-enhancing additive systems that reduce operational risks.Quick service restaurants constitute the fastest-growing end-use segment, expanding at nearly 8% annually as global restaurant chains standardize menus and expand geographically. Frozen dough solutions supported by advanced additives allow QSR operators to simplify operations while maintaining consistent taste and texture across locations. Retail frozen bakery brands are also increasing additive usage as private-label offerings gain market traction, driven by consumer demand for convenience-oriented meal solutions. Additionally, export-driven bakery manufacturing hubs across Europe and Asia are generating incremental demand as cross-border frozen dough shipments expand, requiring additives capable of maintaining product integrity throughout extended logistics cycles.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen Dough Additives Market Segmentations

By Additive Type

- Enzymes

- Emulsifiers

- Hydrocolloids & Dough Conditioners

- Oxidizing Agents

- Preservatives & Shelf-Life Extenders

- Flavor & Texture Enhancers

By Functionality

- Dough Stability Enhancement

- Freeze–Thaw Stability Improvement

- Volume & Texture Optimization

- Shelf-Life Extension

- Fermentation Control

- Moisture Retention

By Application

- Bread & Rolls

- Pizza Dough

- Viennoiserie (Croissants, Danish)

- Cakes & Pastries

- Cookies & Biscuits Dough

- Specialty & Artisan Frozen Dough

By Form

- Powdered Additives

- Liquid Additives

- Paste/Gel Systems

By Distribution Channel

- Direct Industrial Supply (B2B)

- Ingredient Distributors

- Bakery Solution Providers

By End User

- Industrial Bakeries

- Quick Service Restaurants (QSRs)

- Retail Frozen Dough Brands

- Foodservice & Catering

- In-Store Bakery Chains

Regional Insights

Europe

Europe leads the frozen dough additives market with approximately 34% share in 2025, supported by deeply established frozen bakery traditions, advanced industrial baking infrastructure, and strong intra-regional trade networks. Countries such as Germany, France, Italy, and Spain serve as major production and export centers for frozen bakery products. Regional growth is driven by high consumer demand for premium baked goods, increasing adoption of convenience-oriented bakery solutions, and stringent food quality standards that encourage the use of technologically advanced additives. France remains a major contributor due to global exports of frozen viennoiserie products, while Germany’s highly automated industrial bakery sector drives consistent additive consumption. Rising labor costs and workforce shortages across European bakeries further accelerate frozen dough adoption, reinforcing long-term demand for performance-enhancing additive systems.

North America

North America accounts for nearly 28% of global demand, led by the United States, where large-scale commercial bakeries and foodservice chains dominate production. Regional market expansion is driven by labor constraints, high operational expenses, and the need for production efficiency, all of which encourage the transition toward frozen dough solutions supported by advanced additives. The growth of supermarket in-store bakeries and expansion of quick service restaurant chains continue to strengthen additive demand. Additionally, increasing consumer preference for ready-to-bake and convenience foods, combined with technological innovation in bakery ingredients and clean-label reformulation trends, supports sustained regional market growth.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at over 9% CAGR, driven by rapid urbanization, rising disposable incomes, and changing dietary patterns favoring Western-style baked goods. China and India are experiencing accelerated industrial bakery expansion supported by modern retail development and growing demand for packaged convenience foods. Regional growth is further supported by investments in cold-chain infrastructure and food processing modernization. Japan and South Korea contribute through premium frozen bakery innovation, high-quality ingredient adoption, and strong demand for texture-focused bakery products. Increasing penetration of international bakery chains and evolving consumer lifestyles continue to drive adoption of frozen dough additives across the region.

Latin America

Latin America is witnessing steady market expansion, led by Brazil and Mexico as organized retail and modern bakery chains continue to expand across urban centers. Regional growth is supported by increasing demand for affordable convenience foods and operational efficiency improvements within supermarket bakeries. Frozen dough adoption is rising as bakeries seek standardized production outcomes while reducing labor dependency. Improvements in cold storage logistics, growth of quick service restaurant networks, and expanding middle-class consumption patterns further contribute to additive demand across the region.

Middle East & Africa

The Middle East & Africa region is experiencing gradual but consistent growth, with the UAE and Saudi Arabia leading demand due to strong hospitality sector expansion and reliance on imported frozen bakery products. Regional market growth is driven by tourism development, increasing hotel and restaurant investments, and expanding modern retail infrastructure. Limited local bakery production capacity in several countries encourages reliance on frozen dough imports, thereby increasing additive usage throughout supply chains. Rising urban populations, evolving dietary preferences, and the expansion of international foodservice brands continue to support long-term demand for frozen dough additives across the region.

Key Players in the Frozen Dough Additives Market

- Lesaffre

- AB Mauri

- IFF (Danisco)

- DSM-Firmenich

- Kerry Group

- Puratos Group

- Corbion N.V.

- Lallemand Inc.

- Novonesis

- Bakels Worldwide

- Archer Daniels Midland (ADM)

- Cargill Inc.

- Associated British Foods Ingredients

- Tate & Lyle PLC

- Oriental Yeast Co., Ltd.