Acidulants in Beverages Market Size

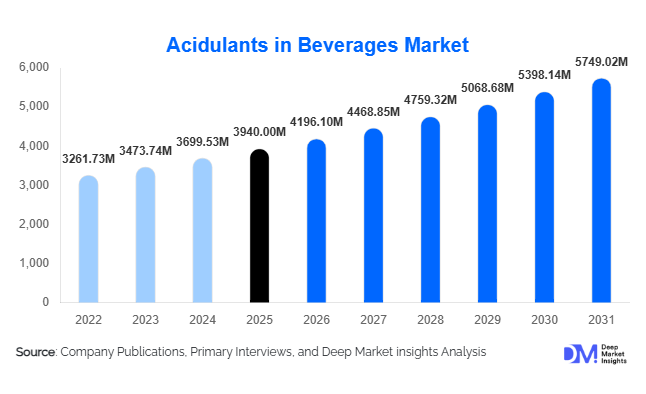

According to Deep Market Insights, the global acidulants in beverages market size was valued at USD 3,940 million in 2025 and is projected to grow from USD 4,196.10 million in 2026 to reach USD 5,749.02 million by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The market growth is primarily driven by rising consumption of ready-to-drink (RTD) beverages, increasing demand for clean-label and fermentation-derived ingredients, and growing innovation in functional and fortified drinks. Acidulants play a critical role in beverage formulation by regulating pH, enhancing flavor profiles, stabilizing carbonation, and extending shelf life. As beverage manufacturers continue reformulation strategies to reduce sugar and artificial preservatives, the demand for citric, malic, lactic, and phosphoric acids is strengthening globally.

Key Market Insights

- Citric acid dominates the market, accounting for nearly 42% of total revenue share in 2025 due to its versatility across carbonated drinks and juices.

- Natural fermentation-based acidulants hold over 63% share, driven by clean-label and regulatory preferences in North America and Europe.

- Asia-Pacific leads the global market, contributing approximately 38% of global demand in 2025, supported by China and India’s beverage manufacturing expansion.

- Functional and fortified beverages are the fastest-growing application, expanding at over 8% CAGR and boosting acidulant integration for mineral stabilization.

- Powdered acidulants account for nearly 68% of sales, preferred for longer shelf life and ease of transport.

- Top five companies control around 54% of global market share, reflecting moderate consolidation and strong fermentation capacity control.

What are the latest trends in the acidulants in beverages market?

Shift Toward Fermentation-Based & Clean-Label Acidulants

Beverage brands are increasingly transitioning toward bio-based acidulants produced through microbial fermentation. Consumers are scrutinizing ingredient labels, encouraging manufacturers to replace synthetic variants with naturally derived citric and lactic acids. European and North American regulatory bodies are reinforcing additive transparency, accelerating this shift. Premium beverages now highlight “naturally sourced acidity regulators” as a marketing differentiator, allowing suppliers to command 8–12% higher margins for fermentation-derived grades.

Growth of Functional & Reduced-Sugar Beverages

As sugar reduction becomes a global priority, acidulants are playing a central role in taste balancing. Malic and citric acids enhance perceived sweetness while compensating for reduced sugar content. Functional beverages fortified with electrolytes, vitamins, and probiotics rely on acidulants to maintain solubility and product stability. The rapid expansion of flavored water, plant-based drinks, and immunity beverages is creating consistent demand for customized acid blends.

What are the key drivers in the acidulants in beverages market?

Expansion of Ready-to-Drink Beverage Consumption

Urbanization and convenience-driven consumption are increasing global intake of carbonated drinks, RTD tea and coffee, energy drinks, and flavored water. With the global beverage industry expanding at approximately 5–6% CAGR, acidulant usage per liter remains stable or increasing due to formulation complexity. Carbonated soft drinks alone represent nearly 34% of total acidulant demand.

Shelf-Life Extension and Food Safety Compliance

Acidulants lower beverage pH levels, inhibiting microbial growth and reducing dependence on synthetic preservatives. Stricter global food safety standards are encouraging manufacturers to optimize acidity levels, ensuring regulatory compliance and product stability during international distribution.

Reformulation and Premiumization Strategies

Beverage brands are increasingly experimenting with flavor complexity, hybrid fruit blends, and botanical infusions. Acidulants enable enhanced tartness and taste differentiation, supporting premium beverage launches in mature markets.

What are the restraints for the global market?

Raw Material Price Volatility

Fermentation-based acidulants depend on feedstocks such as corn, molasses, and sugar substrates. Agricultural price fluctuations can impact production costs and compress margins, particularly for citric acid manufacturers.

Regulatory Scrutiny on Phosphoric Acid

Phosphate-related health concerns are moderating phosphoric acid usage in certain markets. Declining cola consumption in North America and Western Europe slightly constrains segmental growth.

What are the key opportunities in the acidulants industry?

Emerging Market Beverage Industrialization

India, Indonesia, Vietnam, Saudi Arabia, and African nations are witnessing significant beverage manufacturing expansion. Localization of acidulant production can reduce import dependency and logistics costs, presenting strong growth opportunities.

Customized Blended Acidulant Solutions

Suppliers offering tailored acid blends for specific beverage formulations-such as sports drinks or probiotic beverages can capture premium contracts and improve client retention.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3940 Million |

| Market Size in 2026 | USD 4196.10 Million |

| Market Size in 2031 | USD 5749.02 Million |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global beverage acidulants market is segmented by product type into citric acid, phosphoric acid, malic acid, lactic acid, fumaric acid, and blended acidulants. Among these, citric acid remains the dominant segment, accounting for approximately 42% of total market share in 2025. The segment’s leadership is primarily driven by its broad compatibility across carbonated soft drinks, fruit juices, flavored water, and functional beverages. Its cost-effectiveness, strong acidification efficiency, flavor-enhancing properties, and natural sourcing through fermentation further strengthen its widespread adoption. Additionally, growing demand for clean-label and naturally derived ingredients continues to reinforce citric acid’s market dominance.Phosphoric acid holds nearly 21% of the market, largely supported by its essential role in cola beverages. Its ability to deliver sharp acidity and enhance shelf stability makes it indispensable for major carbonated beverage formulations. However, health-conscious trends are gradually encouraging partial substitution in certain formulations.

Malic acid is expanding rapidly, particularly in fruit-flavored and reduced-sugar beverages. Its longer-lasting sourness profile enhances flavor perception, making it ideal for sugar-reduction strategies without compromising taste.Lactic acid and fumaric acid are gaining traction in functional drinks, dairy-based beverages, and fortified formulations due to their pH control efficiency and preservative functionality.Blended acidulants represent a niche but high-margin segment, increasingly adopted in sports drinks, energy beverages, and fortified formulations. These customized blends allow manufacturers to optimize taste balance, stability, and performance benefits, supporting premium product positioning.

Application Insights

By application, carbonated soft drinks (CSDs) lead the market with approximately 34% share in 2025. The segment’s dominance is driven by high global soda consumption, strong brand presence, and continuous product reformulations requiring precise pH control and flavor enhancement. Acidulants remain essential in maintaining product stability, carbonation efficiency, and shelf life in CSD formulations.Fruit juices and nectars account for nearly 22% of total demand. Rising consumer preference for natural and fruit-based beverages is sustaining demand for citric and malic acid as flavor enhancers and preservative agents.

Sports and energy drinks represent around 14% of the market and are among the fastest-growing segments. Growth is supported by increasing fitness awareness, expanding young consumer demographics, and demand for performance-oriented beverages. Acidulants play a critical role in flavor balancing, electrolyte stabilization, and product safety.Functional beverages, including vitamin-enhanced water, probiotic drinks, and plant-based fortified beverages, are expanding at over 8% CAGR. The segment’s growth is fueled by health-conscious consumers seeking immunity, hydration, and gut-health benefits. Acidulants ensure product safety, enhance nutrient stability, and maintain desired taste profiles, creating sustained long-term demand.

Form Insights

Based on form, powdered acidulants dominate the market with approximately 68% share. The segment’s leadership is attributed to easier storage, longer shelf life, cost-efficient transportation, and enhanced stability under varying environmental conditions. Powdered formats are particularly preferred by beverage manufacturers operating across multiple geographic markets due to reduced logistics costs and improved supply chain efficiency.Liquid acidulants account for nearly 32% of the market and are primarily preferred in large-scale beverage production facilities equipped with automated and integrated dosing systems. Liquid formats enable precise real-time blending and improved production efficiency, making them suitable for high-volume carbonated beverage manufacturing.

Explore more data points, trends and opportunities Download Free Sample Report

Acidulants in Beverages Market Segmentations

By Product Type

- Citric Acid

- Phosphoric Acid

- Malic Acid

- Tartaric Acid

- Lactic Acid

- Fumaric Acid

- Acetic Acid

- Glucono Delta Lactone (GDL)

- Blended Acidulants

By Function

- pH Control

- Flavor Enhancement

- Preservative & Microbial Stability

- Chelating/Sequestration Agent

- Carbonation Stabilization

By Beverage Type (Application)

- Carbonated Soft Drinks

- Fruit Juices & Nectars

- Sports & Energy Drinks

- Ready-to-Drink (RTD) Tea & Coffee

- Alcoholic Beverages

- Functional & Fortified Drinks

- Flavored & Enhanced Water

- Dairy-Based Beverages

By Form

- Powder

- Liquid

By Distribution Channel

- Direct Supply to Beverage Manufacturers

- Ingredient Distributors

- Contract Manufacturing Supply

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest market share at approximately 38% in 2025. The region’s dominance is driven by its large-scale beverage production base, expanding middle-class population, rapid urbanization, and increasing demand for ready-to-drink (RTD) beverages. China alone contributes nearly 18% of global demand due to its extensive manufacturing capacity, strong domestic consumption, and export-oriented beverage industry.India is the fastest-growing country in the region, expanding at over 8.5% CAGR. Growth is supported by rising disposable incomes, rapid retail expansion, increasing youth population, and growing demand for carbonated drinks, fruit beverages, and functional drinks. Additionally, expanding local manufacturing of food-grade acidulants strengthens regional supply capabilities.

North America

North America accounts for nearly 27% of the global market share, with the United States leading regional demand. Growth is primarily driven by strong carbonated beverage production, continuous innovation in energy and functional drinks, and established beverage brands.Clean-label trends, regulatory scrutiny over synthetic additives, and rising consumer demand for natural and organic beverages are accelerating adoption of fermentation-based and naturally sourced acidulants. Additionally, product reformulation strategies aimed at sugar reduction are creating new opportunities for malic and blended acidulant solutions.

Europe

Europe contributes approximately 22% of global share, led by Germany, France, and the United Kingdom. The region’s growth is supported by stringent regulatory standards promoting safe and natural additives, which favor fermentation-derived acidulants.Increasing demand for low-sugar beverages, functional drinks, and plant-based alternatives is further supporting acidulant consumption. Strong innovation in premium beverage categories and sustainability-focused ingredient sourcing also contributes to steady regional expansion.

Latin America

Latin America represents around 8% of the global market, with Mexico and Brazil driving regional demand. High per capita soda consumption, expanding beverage exports, and increasing urban retail penetration support acidulant usage.Additionally, the growing popularity of flavored water, fruit beverages, and energy drinks is contributing to gradual market expansion. Local production capabilities and cost-sensitive formulations favor citric acid dominance in the region.

Middle East & Africa

The Middle East & Africa account for nearly 5% of global demand. Saudi Arabia and South Africa are the leading markets due to expanding beverage industrialization and rising consumption of carbonated and energy drinks.Favorable youth demographics, increasing tourism, rising disposable incomes, and expanding modern retail infrastructure are supporting steady beverage market growth. Although currently smaller in size, the region presents long-term growth potential driven by urban expansion and diversification of beverage offerings.

Key Players in the Acidulants in Beverages Market

- Cargill Incorporated

- Archer Daniels Midland Company (ADM)

- Tate & Lyle PLC

- Jungbunzlauer Suisse AG

- Corbion N.V.

- Brenntag SE

- Bartek Ingredients Inc.

- COFCO Biochemical

- RZBC Group

- TTCA Co., Ltd.

- Weifang Ensign Industry Co., Ltd.

- Gadot Biochemical Industries

- Shandong Juxian Hongde Citric Acid Co., Ltd.

- Fuso Chemical Co., Ltd.

- Hawkins Watts Limited