A2 Milk Infant Formula Market Size

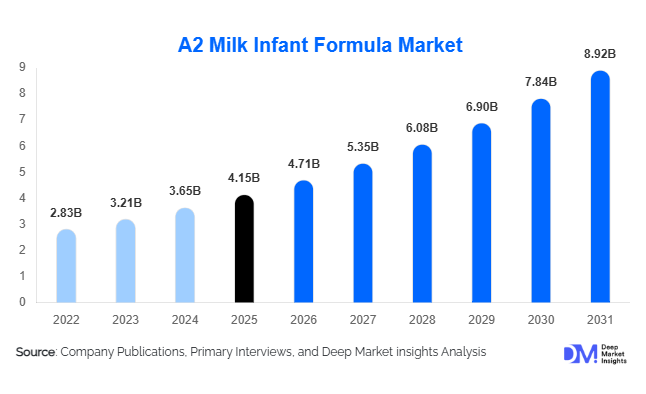

According to Deep Market Insights, the global A2 milk infant formula market size was valued at USD 4.15 billion in 2025 and is projected to grow from USD 4.71 billion in 2025 to reach approximately USD 8.92 billion by 2030, expanding at a robust CAGR of 13.6% during the forecast period (2026–2031). The A2 milk infant formula market growth is primarily driven by rising parental awareness regarding infant digestive health, increasing preference for premium and protein-specific nutrition, and growing clinical endorsement of A2 beta-casein–based formulas as a gentler alternative to conventional A1 protein formulas.

Key Market Insights

- A2 milk infant formula is rapidly transitioning from a niche to a mainstream premium category, particularly in Asia-Pacific, supported by strong consumer trust in digestive health claims.

- Stage 1 (0–6 months) formula dominates global demand, as parents prioritize digestibility and safety during early infancy.

- Asia-Pacific accounts for the largest market share, led by China, Australia, and New Zealand, supported by strong import demand and domestic premiumization trends.

- Super-premium pricing tiers command the majority of market value, reflecting high willingness to pay for clinically perceived benefits.

- Offline retail channels such as pharmacies and specialty baby stores remain critical, while cross-border e-commerce continues to expand access in emerging markets.

- Product innovation integrating A2 protein with probiotics, HMOs, and DHA/ARA is shaping next-generation infant formula offerings.

What are the latest trends in the A2 milk infant formula market?

Premiumization and Clean-Label Nutrition

Premiumization remains a defining trend in the A2 milk infant formula market. Parents are increasingly scrutinizing ingredient lists, sourcing transparency, and protein composition, driving strong demand for clean-label, minimally processed formulations. A2 milk formulas benefit from clear differentiation through single-protein positioning, traceable dairy herds, and perceived digestive advantages. Organic A2 formulas are gaining traction, particularly in Europe and North America, where regulatory oversight and consumer awareness of pesticide-free and hormone-free nutrition are high. As a result, brands are investing heavily in storytelling around farm origins, genetic testing of A2 cows, and sustainable dairy practices to strengthen brand trust.

Expansion of Cross-Border and Digital Sales Channels

Cross-border e-commerce has emerged as a key enabler of market growth, especially in China and Southeast Asia. Parents increasingly rely on international platforms to access premium A2 formulas from Australia, New Zealand, and Europe. Brand-owned digital platforms are also gaining importance, allowing manufacturers to control pricing, combat counterfeiting, and educate consumers directly. Subscription-based infant nutrition models are being piloted, offering recurring deliveries and personalized feeding plans, which improve customer retention and lifetime value.

What are the key drivers in the A2 milk infant formula market?

Rising Incidence of Infant Digestive Sensitivities

Digestive discomfort, colic, and constipation are increasingly reported among infants consuming conventional A1 protein-based formulas. Pediatric recommendations and parental experiences are driving a shift toward A2 beta-casein formulas, which are perceived to produce fewer digestive by-products. This driver is particularly strong in China, Australia, and urban North America, where clinical awareness and parental education levels are high. As digestive comfort becomes a primary purchase criterion, A2 formulas are benefiting from strong word-of-mouth and repeat purchase behavior.

Increasing Willingness to Pay for Early-Life Nutrition

Parents globally are prioritizing early-life nutrition as a long-term investment in child health and development. Declining birth rates in developed economies are further intensifying per-child spending. A2 milk infant formula aligns well with this trend, positioning itself as a super-premium, science-backed alternative. Higher disposable incomes, especially among urban middle-class households in Asia-Pacific, are accelerating adoption despite premium pricing.

What are the restraints for the global market?

High Cost of A2 Milk Sourcing and Production

The requirement for genetically certified A2-only dairy herds significantly increases raw milk procurement costs. Maintaining herd purity, conducting DNA testing, and ensuring segregation across the supply chain elevate production expenses. These costs limit pricing flexibility and constrain penetration in highly price-sensitive markets, particularly in parts of Africa and South Asia.

Complex and Stringent Regulatory Landscape

Infant formula is among the most heavily regulated food categories globally. Differing regulatory frameworks across regions particularly between China, Europe, and North America increase compliance costs and delay product launches. Smaller players often struggle with clinical validation, labeling requirements, and import approvals, acting as a barrier to entry and slowing market diversification.

What are the key opportunities in the A2 milk infant formula industry?

Emerging Market Penetration in High Birth-Rate Regions

Countries such as India, Indonesia, Vietnam, Nigeria, and Brazil present significant untapped opportunities due to rising birth rates and expanding middle-class populations. While penetration of A2 infant formula remains low, increasing urbanization, maternal education, and exposure to global nutrition trends are expected to drive rapid adoption. Local manufacturing partnerships and smaller pack sizes could significantly expand addressable demand.

Functional and Specialty A2 Formulations

There is strong opportunity to combine A2 protein with functional nutrition enhancements such as probiotics, prebiotics, HMOs, and immunity-supporting micronutrients. Specialty A2 formulas targeting lactose sensitivity, allergies, and premature infants represent high-margin growth avenues. Brands investing in clinical substantiation and pediatric endorsement are likely to gain long-term competitive advantage.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.15 Billion |

| Market Size in 2026 | USD 4.71 Billion |

| Market Size in 2031 | USD 8.92 Billion |

| CAGR | 13.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Stage 1 A2 milk infant formula (0–6 months) dominates the global market, accounting for approximately 38% of total market value in 2025. This segment’s leadership is primarily driven by exclusive feeding requirements during early infancy, as newborns rely almost entirely on formula or breast milk for nutrition. Heightened parental concern regarding digestibility, protein tolerance, and safety further strengthens demand for A2-based formulations during this critical developmental stage. The perception that A2 beta-casein protein is gentler on infant digestion compared to conventional milk proteins has significantly influenced purchasing decisions among first-time parents.

Stage 2 (6–12 months) and Stage 3 (12–36 months) A2 infant formulas together represent a substantial share of the market, supported by rising awareness of toddler-specific nutritional needs and increased focus on immunity, cognitive development, and gut health during weaning and early childhood. Parents are increasingly adopting follow-on formulas as part of structured feeding routines, particularly in urban and dual-income households.

Form Insights

Powdered A2 milk infant formula accounts for nearly 82% of global demand, making it the dominant form segment. The leading driver for powdered formula adoption is its longer shelf life combined with cost efficiency, which is especially important for bulk purchasing, international trade, and household storage. Ease of transportation and lower logistics costs further reinforce its preference across both developed and emerging markets.

Liquid and ready-to-feed A2 infant formulas are gaining gradual traction, particularly in developed regions such as North America, Europe, and parts of East Asia. Demand in this segment is driven by convenience-oriented consumption patterns, especially among working parents and urban families. However, higher pricing, limited product variety, and shorter shelf life continue to restrict widespread adoption compared to powdered alternatives.

Distribution Channel Insights

Offline retail channels contribute approximately 57% of global sales, maintaining their dominant position in the A2 milk infant formula market. The primary driver for offline dominance is the high level of consumer trust associated with pharmacies, drugstores, and specialty baby stores. These outlets offer professional guidance, pharmacist recommendations, and physical product verification, which are critical factors in infant nutrition purchasing decisions.

Online distribution channels are expanding rapidly and represent the fastest-growing sales channel. Growth is driven by cross-border e-commerce, wider product availability, and competitive pricing, particularly in Asia-Pacific markets such as China and Southeast Asia. Brand-owned websites are increasingly being leveraged to combat counterfeit products, offer subscription-based purchasing models, and provide detailed nutritional education, thereby strengthening brand loyalty and direct-to-consumer engagement.

End-Use Insights

Household infant feeding remains the primary end-use segment, accounting for over 95% of total consumption. The leading growth driver for this segment is the rising prevalence of urban, dual-income households, where breastfeeding duration is often limited due to lifestyle and work constraints. Parents in these households show a strong preference for premium, easily digestible infant nutrition products.

Hospitals and maternity clinics play an influential secondary role by shaping brand preference through recommendations, sampling programs, and early-stage feeding guidance. While institutional consumption volumes remain limited, their indirect impact on household purchasing decisions is significant.

Explore more data points, trends and opportunities Download Free Sample Report

A2 Milk Infant Formula Market Segmentations

By Product Type

- Stage 1 Formula (0–6 Months)

- Stage 2 Formula (6–12 Months)

- Stage 3 Formula (12–36 Months)

- Specialty A2 Infant Formula (Digestive Care, DHA/ARA Enriched, Lactose-Sensitive)

By Form

- Powdered A2 Infant Formula

- Liquid / Ready-to-Feed A2 Infant Formula

By Source of Milk

- Cow-Based A2 Milk Formula

- Goat-Based A2 Milk Formula

By Nature

- Conventional A2 Infant Formula

- Organic A2 Infant Formula

By Distribution Channel

- Supermarkets & Hypermarkets

- Pharmacies & Drugstores

- Specialty Baby Stores

- Online Retail

By Price Tier

- Premium

- Super-Premium / Ultra-Premium

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global A2 milk infant formula market with approximately 45% market share in 2025. China alone accounts for nearly 28% of global demand, driven by strong premiumization trends, high trust in imported infant formula brands, and widespread awareness of A2 protein benefits following historical food safety concerns.

Key regional growth drivers include rising disposable incomes, declining breastfeeding rates in urban centers, and increasing parental focus on digestive health. Australia and New Zealand serve as major production and export hubs due to strong dairy regulations and A2 milk availability. Meanwhile, India and Southeast Asia represent the fastest-growing markets, with CAGRs exceeding 16%, supported by expanding middle-class populations and growing penetration of modern retail and e-commerce platforms.

North America

North America holds approximately 22% of global market share, led by the United States. Growth in this region is driven by increasing awareness of protein-specific nutrition and digestive health, along with a rising incidence of infant gastrointestinal sensitivities.

High purchasing power, strong preference for premium infant nutrition, and growing demand for organic, clean-label, and goat-based A2 formulas further support market expansion. Regulatory clarity and well-established pediatric recommendation systems also contribute to steady adoption.

Europe

Europe accounts for approximately 18% of global demand, with the U.K., Germany, and France as key markets. The primary growth driver in this region is strict regulatory oversight combined with strong consumer preference for organic, non-GMO, and clean-label infant nutrition products.

European parents demonstrate high awareness of ingredient sourcing and protein composition, supporting gradual but consistent adoption of A2 infant formulas, particularly in premium retail segments.

Latin America

Latin America represents around 8% of the global market, led by Brazil and Mexico. Market growth is driven by rapid urbanization, expansion of the middle class, and increasing exposure to premium infant nutrition brands.

Improving retail infrastructure and rising influence of digital marketing and e-commerce platforms are further enhancing consumer access to A2 milk infant formula products across the region.

Middle East & Africa

The Middle East & Africa region accounts for approximately 7% of global demand, with the UAE and Saudi Arabia leading regional consumption. The primary growth drivers include high disposable incomes, strong reliance on imported infant formula, and premium brand preference.

In parts of Africa, market growth remains gradual but positive, supported by improving healthcare access, urban population growth, and increasing awareness of infant nutrition standards.

Key Players in the A2 Milk Infant Formula Market

- The a2 Milk Company

- Nestlé

- Danone

- Mead Johnson Nutrition

- Abbott Laboratories

- Fonterra

- Yili Group

- Mengniu Dairy

- Bellamy’s Organic

- Ausnutria Dairy

- Beingmate

- Synlait Milk

- Hipp GmbH

- Feihe International

- FrieslandCampina