3D Audio Market Size

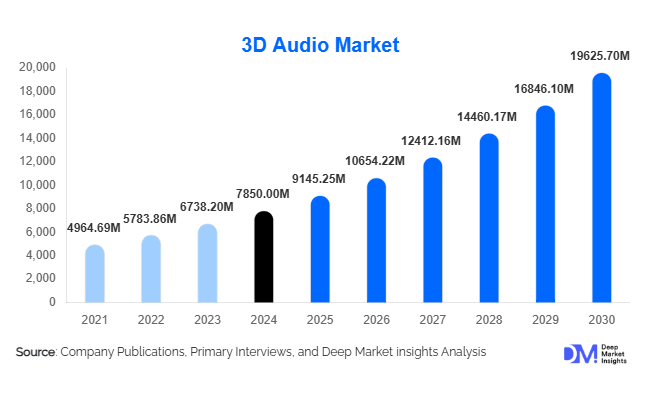

According to Deep Market Insights, the global 3D audio market size was valued at USD 7,850 million in 2025 and is projected to grow from USD 9,145.25 million in 2026 to reach USD 19,625.70 million by 2031, expanding at a CAGR of 16.5% during the forecast period (2026–2031). The growth of the 3D audio market is primarily driven by rising adoption of immersive entertainment technologies, increasing penetration of AR/VR devices, rapid growth of gaming and esports, and expanding use of spatial audio in automotive infotainment and enterprise simulation applications.

Key Market Insights

- Object-based and spatial audio formats are becoming industry standards, driven by gaming engines, OTT platforms, and immersive content creation workflows.

- Software-based 3D audio solutions dominate the market, supported by recurring licensing models and integration into consumer and enterprise ecosystems.

- North America leads the global market, supported by strong technology adoption, advanced content ecosystems, and automotive innovation.

- Asia-Pacific is the fastest-growing region, fueled by electronics manufacturing, mobile gaming expansion, and government-backed digital initiatives.

- Automotive applications are emerging as a high-growth segment, with premium EVs increasingly integrating immersive audio systems.

- AI-driven audio processing and personalization are reshaping product differentiation and improving real-time spatial sound rendering.

What are the latest trends in the 3D audio market?

Mainstream Adoption of Spatial Audio in Consumer Devices

Spatial and 3D audio technologies are rapidly transitioning from premium features to mainstream capabilities across consumer electronics. Smartphones, smart TVs, gaming consoles, and wireless headphones increasingly ship with native spatial audio support, enabling immersive sound experiences without specialized hardware. Streaming platforms and music services are expanding spatial audio catalogs, encouraging content creators to produce audio mixes optimized for three-dimensional playback. This trend is significantly increasing consumer awareness and accelerating mass-market adoption of 3D audio technologies.

Integration of AI and Real-Time Audio Rendering

Artificial intelligence is playing a critical role in advancing 3D audio performance. AI-powered engines enable dynamic sound positioning, adaptive acoustic environments, and personalized head-related transfer function (HRTF) modeling. These capabilities are especially important for gaming, VR training, and live virtual events where real-time responsiveness is essential. As AI models improve computational efficiency, 3D audio solutions are becoming more scalable across cloud-based and edge-computing platforms.

What are the key drivers in the 3D audio market?

Growth of Gaming, eSports, and Immersive Entertainment

The global gaming and esports industry is one of the strongest drivers of 3D audio adoption. Competitive gamers increasingly rely on positional audio for tactical advantages, while game developers integrate object-based sound design to enhance realism. The rise of cloud gaming, VR gaming, and cross-platform engines has further increased demand for advanced audio middleware and rendering software. Gaming alone accounted for nearly 29% of the total 3D audio market revenue in 2025.

Expansion of AR/VR and Simulation-Based Applications

Enterprise adoption of AR/VR technologies for training, simulation, and design visualization is accelerating demand for high-fidelity spatial audio. Industries such as defense, healthcare, aviation, and education require realistic audio cues to enhance situational awareness and learning outcomes. Government and enterprise investments in digital twins and virtual training environments are creating long-term demand for scalable 3D audio solutions.

Automotive Industry Shift Toward Software-Defined Vehicles

Automotive manufacturers are increasingly integrating immersive audio as a core feature in premium and electric vehicles. 3D audio enhances in-car entertainment, navigation alerts, and advanced driver-assistance systems by improving sound localization and clarity. As vehicles become software-defined platforms, licensing-based audio solutions and long-term OEM partnerships are emerging as key revenue drivers for market participants.

What are the restraints for the global market?

High Development and Computational Costs

Advanced 3D audio rendering requires significant processing power and specialized expertise, particularly for real-time applications. This increases development costs for content creators and limits adoption among smaller developers and budget-constrained markets. Hardware limitations in low-cost consumer devices also restrict performance consistency across platforms.

Lack of Universal Standards and Interoperability

The absence of fully unified standards across hardware manufacturers and software platforms creates compatibility challenges. Inconsistent playback experiences across devices can reduce consumer satisfaction and complicate content distribution. Addressing interoperability remains a key challenge for industry-wide scalability.

What are the key opportunities in the 3D audio industry?

Metaverse and Virtual Collaboration Platforms

The development of metaverse environments and virtual collaboration tools presents a major growth opportunity. Spatial audio is essential for realistic social interaction, remote teamwork, and virtual events. As enterprises adopt virtual offices and immersive collaboration spaces, demand for scalable 3D audio engines is expected to grow rapidly.

Government-Supported Digital Infrastructure Initiatives

National programs such as “Make in India,” “Made in China 2025,” and smart city initiatives are driving investments in digital content, simulation technologies, and electronics manufacturing. These initiatives support localized production of 3D audio hardware and software, reducing costs and expanding addressable markets for new entrants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7850 Million |

| Market Size in 2026 | USD 9145.25 Million |

| Market Size in 2031 | USD 19625.70 Million |

| CAGR | 16.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Technology Type Insights

Object-based audio dominates the technology landscape, accounting for approximately 34% of total market revenue in 2025 due to its flexibility and real-time rendering capabilities. Binaural audio remains widely used in headphones and VR applications, while ambisonics is gaining traction in cinematic and live-event environments. Wave field synthesis and advanced HRTF processing represent niche but high-value segments focused on professional and research applications.

Component Insights

Software solutions represent the largest share of the market at around 57% in 2025, driven by licensing revenues, SDK integrations, and middleware adoption. Hardware components such as headsets, soundbars, and automotive speaker systems continue to grow steadily, supported by consumer electronics and vehicle production volumes.

End-Use Industry Insights

Gaming and esports lead end-use adoption, followed by media and entertainment, VR/AR, and automotive. Automotive is the fastest-growing end-use segment, expanding at over 18% CAGR, as immersive audio becomes a key differentiator in electric and premium vehicles. Healthcare and defense are emerging as high-value niches, leveraging 3D audio for simulation, therapy, and training applications.

Explore more data points, trends and opportunities Download Free Sample Report

3D Audio Market Segmentations

By Technology Type

- Object-Based Audio

- Binaural Audio

- Ambisonics

- Wave Field Synthesis

- Head-Related Transfer Function (HRTF) Processing

By Component

- Hardware

- Software

By Deployment Platform

- Consumer Devices

- Enterprise & Commercial Systems

By End-Use Industry

- Gaming & eSports

- Media & Entertainment

- Virtual Reality (VR) & Augmented Reality (AR)

- Automotive

- Healthcare

- Defense & Aerospace

- Education & Corporate Training

Regional Insights

North America

North America accounts for approximately 38% of the global 3D audio market in 2025, led by the United States. Strong presence of technology leaders, high adoption of gaming and streaming platforms, and advanced automotive innovation support regional dominance.

Europe

Europe represents a mature market with strong demand from Germany, the UK, and France. Automotive audio innovation, cinematic production, and enterprise simulation drive adoption across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing region, accounting for about 31% of global demand in 2025. China, Japan, South Korea, and India are key contributors, supported by electronics manufacturing, mobile gaming growth, and government-backed digital initiatives.

Latin America

Latin America holds a smaller but growing share, driven by rising smartphone penetration and gaming adoption in countries such as Brazil and Mexico.

Middle East & Africa

The Middle East & Africa region is witnessing gradual adoption, particularly in defense simulation, smart infrastructure, and premium automotive segments led by the UAE and Saudi Arabia.

Key Players in the 3D Audio Market

- Dolby Laboratories

- Sony Corporation

- Apple Inc.

- Sennheiser Electronic

- DTS (Xperi Inc.)

- Bose Corporation

- Yamaha Corporation

- Harman International

- Avid Technology

- Microsoft Corporation

- NVIDIA Corporation

- Qualcomm Incorporated

- Bang & Olufsen

- Valve Corporation

- Meta Platforms, Inc.