Yogurt Natural (Yoplait) Market Size

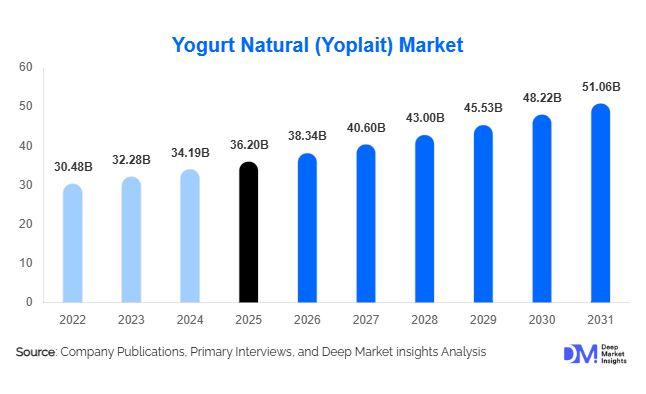

According to Deep Market Insights, the global yogurt natural (Yoplait segment) market size was valued at USD 36.2 billion in 2025 and is projected to grow from USD 38.34 billion in 2026 to reach USD 51.06 billion by 2031, expanding at a CAGR of 5.9% during the forecast period (2026–2031). Market growth is primarily driven by rising health awareness, increasing consumption of clean-label dairy products, and strong demand for protein-rich and probiotic foods across both developed and emerging economies.

Key Market Insights

- Natural and clean-label yogurts are gaining traction, supported by consumer preference for minimally processed foods with transparent ingredient lists.

- Greek-style and skyr-style yogurts are driving value growth, commanding premium pricing due to higher protein content and thicker textures.

- Europe remains the largest consumption hub, supported by long-standing yogurt consumption habits and strong private-label penetration.

- North America shows steady premiumization, with high demand for organic, low-fat, and functional yogurt variants.

- Asia-Pacific is the fastest-growing region, led by China and India, due to urbanization, cold-chain expansion, and Western dietary adoption.

- Packaging innovation and single-serve formats are improving convenience and driving impulse purchases in urban markets.

What are the latest trends in the yogurt natural market?

Premiumization Through High-Protein and Functional Yogurt

High-protein natural yogurts, particularly Greek and skyr-style variants, are increasingly shaping consumer purchasing behavior. These products are positioned as meal replacements or fitness-oriented snacks, appealing to health-conscious consumers and aging populations. Manufacturers are emphasizing texture, satiety benefits, and probiotic functionality, enabling premium pricing and higher margins. This trend is particularly strong in North America and Europe, where protein intake awareness is high.

Clean-Label and Sustainability-Focused Innovation

Consumers are actively avoiding artificial additives, preservatives, and excess sugar, accelerating demand for plain and unsweetened natural yogurts. Brands are responding with shorter ingredient lists, recyclable packaging, and sustainability commitments related to dairy sourcing and carbon footprint reduction. This trend is reinforcing brand loyalty and influencing purchasing decisions in developed markets.

What are the key drivers in the yogurt natural market?

Rising Digestive Health and Probiotic Awareness

Growing awareness of gut health and immunity has significantly increased daily yogurt consumption. Natural yogurt is widely perceived as a functional food, driving consistent household demand and repeat purchases across age groups.

Expansion of Modern Retail and Cold-Chain Infrastructure

Improved refrigeration and organized retail penetration in emerging markets are increasing product accessibility, reducing spoilage, and enabling wider distribution of premium yogurt products.

Growing Demand for Protein-Rich Diets

Fitness trends, aging populations, and lifestyle diseases are encouraging higher protein intake, directly benefiting Greek-style and low-fat natural yogurt segments.

What are the restraints for the global market?

Volatility in Raw Milk Prices

Fluctuations in milk and feed costs directly impact production economics, creating margin pressure for manufacturers, particularly in premium segments.

Cold Storage Dependency and Limited Shelf Life

Natural yogurt requires consistent refrigeration, increasing logistics costs and limiting penetration in regions with underdeveloped cold-chain infrastructure.

What are the key opportunities in the yogurt natural industry?

Functional and Clinical Nutrition Expansion

Opportunities exist to expand yogurt applications in medical nutrition, elderly care, and sports nutrition through fortified formulations and targeted health benefits.

High-Growth Emerging Markets

Asia-Pacific and Middle Eastern countries present strong growth potential, supported by rising disposable incomes, rapid urbanization, expanding dairy consumption, and increasing imports of premium and value-added yogurt products. Growing exposure to Western dietary patterns, improvements in cold-chain infrastructure, and rising health awareness among younger populations further accelerate market penetration in these regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 36.2 Billion |

| Market Size in 2026 | USD 38.34 Billion |

| Market Size in 2031 | USD 51.06 Billion |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Plain natural yogurt dominates the global yogurt market, accounting for approximately 34% of total market value in 2025. Its leadership is driven by widespread household usage, affordability, clean-label perception, and versatility across breakfast, cooking, and snacking applications. Consumers increasingly favor plain yogurt as a base for customization with fruits, grains, and probiotics.

Greek-style and skyr-style yogurts represent the fastest-growing sub-segments, supported by premium positioning, higher protein density, and strong adoption among fitness-focused and health-conscious consumers. Meanwhile, low-fat and fat-free yogurt variants continue to gain traction as demand rises for calorie-controlled, heart-healthy, and weight-management-friendly food options.

Milk Source Insights

Cow milk–based yogurt accounts for nearly 88% of global demand, driven by large-scale milk availability, cost efficiency, established dairy infrastructure, and high consumer familiarity. Its dominance is further reinforced by extensive product variety across mass-market and premium segments.

Goat and sheep milk yogurts remain niche but are witnessing gradual growth due to increasing awareness of their digestibility, lactose sensitivity suitability, and allergen-friendly properties. Demand is particularly strong in premium, organic, and specialty food segments across Europe and North America.

Distribution Channel Insights

Supermarkets and hypermarkets dominate yogurt distribution, accounting for over 52% of total market share. Their dominance is driven by strong shelf visibility, broad product assortments, aggressive promotional strategies, and the rapid expansion of private-label yogurt offerings.

Online and direct-to-consumer channels are growing at a robust pace, especially in urban and semi-urban markets. Growth is supported by convenience-based purchasing, subscription models, quick-commerce platforms, and rising penetration of digital grocery services. These channels are increasingly favored for premium, organic, and specialty yogurt products.

End-Use Insights

Household consumption represents approximately 61% of total yogurt demand, supported by daily dietary use, breakfast consumption habits, and yogurt’s role as a nutritious snack option across age groups.

Foodservice and bakery applications are expanding at a CAGR of over 7%, driven by increasing use of yogurt in sauces, dressings, desserts, smoothies, baked goods, and ready-to-eat meals. Rising demand from cafés, quick-service restaurants, and institutional catering continues to strengthen this segment.

Explore more data points, trends and opportunities Download Free Sample Report

Yogurt Natural (Yoplait) Market Segmentations

By Product Type

- Plain Natural Yogurt

- Low-Fat Natural Yogurt

- Fat-Free Natural Yogurt

- Greek-Style Natural Yogurt

- Skyr-Style Natural Yogurt

By Milk Source

- Cow Milk–Based Yogurt

- Goat Milk–Based Yogurt

- Sheep Milk–Based Yogurt

By Packaging Type

- Single-Serve Cups

- Multi-Serve Tubs

- Drinkable Yogurt Bottles

- Bulk & Foodservice Packs

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online & Direct-to-Consumer

- Foodservice / HoReCa

- Specialty & Health Food Stores

By End-Use Application

- Household Consumption

- Foodservice & QSR

- Bakery & Desserts

- Health & Clinical Nutrition

- Industrial Food Processing

Regional Insights

Europe

Europe accounted for approximately 34% of global yogurt market share in 2025, led by Germany, France, the U.K., and Greece. Strong cultural consumption habits, high per capita dairy intake, and deep-rooted yogurt traditions support stable demand.Regional growth is driven by premiumization, private-label expansion, demand for organic and clean-label products, and continued innovation in functional and high-protein yogurt categories.

North America

North America held nearly 28% of global market share, with the U.S. dominating regional demand. The market benefits from high health awareness, strong brand presence, and continuous product innovation.Growth is fueled by rising demand for premium, organic, lactose-free, and functional yogurts, along with increasing adoption of Greek-style and probiotic-rich formulations.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at a CAGR of over 8%, led by China, India, and Japan. Rapid urbanization, rising middle-class populations, and growing Western dietary influence significantly boost yogurt consumption.Market expansion is further supported by improvements in cold-chain logistics, increasing availability of flavored and drinkable yogurts, and aggressive expansion by multinational and regional dairy brands.

Latin America

Brazil and Mexico dominate yogurt consumption in Latin America, supported by urban population growth and expanding modern retail networks.Growth drivers include rising demand for affordable nutrition, increasing penetration of flavored and fortified yogurts, and growing availability of single-serve packaging formats tailored to on-the-go consumers.

Middle East & Africa

The Middle East & Africa region is led by Saudi Arabia, the UAE, and South Africa, supported by high dairy import volumes and strong demand for premium and functional dairy products.Growth is driven by government food security initiatives, rising disposable incomes, increasing health awareness, and expanding demand for long-shelf-life and fortified yogurt products across urban centers.

Company Market Share

The yogurt natural market is moderately consolidated, with the top five players accounting for approximately 42% of global market share. Leading brands benefit from strong distribution networks, product innovation, and high consumer trust.

Key Players in the Yogurt Natural Market

- Danone

- General Mills

- Lactalis Group

- Nestlé

- Chobani

- Arla Foods

- Fonterra

- Müller Group

- FrieslandCampina

- Fage

- Savencia

- Yili Group

- Mengniu Dairy

- Meiji Holdings

- Morinaga Milk Industry