Wool Felt Hats Market Size

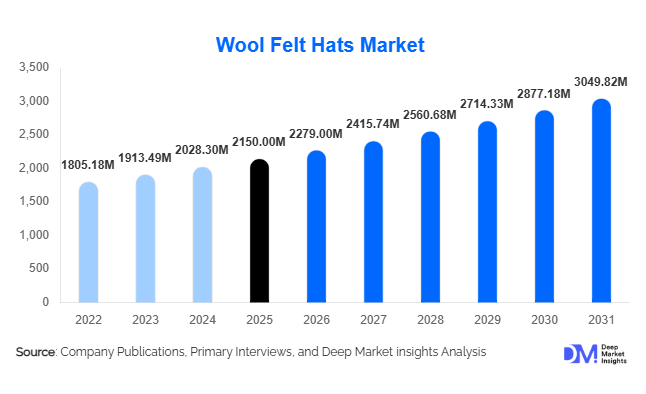

According to Deep Market Insights, the global wool felt hats market size was valued at USD 2,150 million in 2025 and is projected to grow from USD 2,279.00 million in 2026 to reach USD 3,049.82 million by 2031, expanding at a CAGR of 6.0% during the forecast period (2026–2031). The market growth is primarily driven by the resurgence of vintage fashion trends, increasing consumer preference for sustainable materials, and the rising adoption of premium accessories across both developed and emerging economies.

Key Market Insights

- Fashion & lifestyle applications dominate demand, accounting for over 55% of total consumption as hats transition from utility to style statements.

- The mid-range pricing segment leads, contributing nearly 40% of total market share due to its balance of affordability and quality.

- North America dominates the global market with approximately 35% share, driven by strong cultural adoption and high consumer spending.

- Asia-Pacific is the fastest-growing region, supported by rising disposable incomes and increasing fashion awareness.

- Online retail channels account for nearly 45% of total sales, reflecting rapid digital transformation in apparel distribution.

- Sustainability trends, including eco-friendly wool sourcing and biodegradable materials, are reshaping consumer preferences.

What are the latest trends in the wool felt hats market?

Premiumization and Designer Collaborations

The wool felt hats market is increasingly witnessing premiumization, with consumers gravitating toward high-quality, handcrafted products. Designer collaborations and limited-edition collections are becoming prominent, allowing brands to command higher margins and enhance brand exclusivity. Luxury hats priced above USD 300 are gaining traction among affluent consumers, particularly in North America and Europe. These collaborations often blend traditional craftsmanship with modern aesthetics, attracting younger consumers while retaining heritage value. Customisation options, such as personalised trims and bespoke fittings, are further strengthening the premium segment.

Digital Transformation and Direct-to-Consumer Growth

E-commerce and direct-to-consumer (DTC) channels are reshaping the market landscape. Online platforms now contribute significantly to global sales, enabling brands to reach international audiences without relying on traditional retail networks. Technologies such as augmented reality (AR) for virtual try-ons and AI-driven recommendations are enhancing customer engagement. Social media platforms and influencer marketing are also playing a critical role in driving product visibility and consumer adoption. This digital shift is particularly impactful in emerging markets, where online accessibility is accelerating market penetration.

What are the key drivers in the wool felt hats market?

Resurgence of Vintage and Heritage Fashion

The revival of classic fashion styles such as fedoras, trilbies, and bowler hats is a key driver of market growth. These styles are being reintroduced in modern designs, appealing to both traditional and contemporary consumers. Cultural influences, particularly in North America and Europe, continue to sustain demand for heritage-inspired products.

Rising Demand for Sustainable Fashion

Consumers are increasingly prioritizing eco-friendly products, and wool felt hats align well with this trend due to their biodegradable and natural material composition. Brands emphasizing ethical sourcing and sustainable production processes are gaining a competitive edge. Regulatory pressures and consumer awareness are further accelerating this shift toward sustainability.

What are the restraints for the global market?

Seasonal Demand Fluctuations

The demand for wool felt hats is highly seasonal, with peak sales occurring during colder months. This creates uneven revenue streams for manufacturers and retailers, particularly in regions with mild climates. Seasonal dependency also limits year-round production efficiency.

Volatility in Raw Material Prices

Fluctuations in wool prices, driven by climatic conditions and livestock supply constraints, pose a significant challenge for manufacturers. Rising input costs can impact profit margins, especially for mid-range and economy segments where price sensitivity is high.

What are the key opportunities in the wool felt hats industry?

Expansion in Emerging Markets

Emerging economies in the Asia-Pacific and Latin America present significant growth opportunities. Rising disposable incomes, urbanization, and exposure to global fashion trends are driving demand for premium accessories. Localized designs and affordable premium offerings can help brands penetrate these markets effectively.

Sustainable and Ethical Product Innovation

There is growing potential for innovation in sustainable materials and ethical production processes. Brands that invest in cruelty-free wool sourcing, eco-friendly dyes, and transparent supply chains can attract environmentally conscious consumers and differentiate themselves in a competitive market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2150 Million |

| Market Size in 2026 | USD 2279 Million |

| Market Size in 2031 | USD 3049.82 Million |

| CAGR | 6.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fedora hats dominate the product segment, accounting for approximately 28% of the global wool felt hats market in 2025. The leadership of this segment is primarily driven by its versatility across both formal and casual fashion, making it a staple accessory across diverse consumer groups. Fedoras are widely adopted in North America and Europe due to their strong association with vintage and contemporary fashion trends, and their adaptability across seasons enhances consistent demand. In addition, increasing celebrity influence and media exposure have reinforced their popularity globally. Cowboy and western hats continue to maintain a strong foothold, particularly in North America, supported by cultural heritage, outdoor utility, and demand from ranching and country lifestyle segments. Meanwhile, wide-brim and designer felt hats are witnessing accelerated growth in urban fashion markets, driven by premiumization and rising demand for statement accessories. Functional outdoor felt hats, although niche, remain essential in colder climates and outdoor professions, contributing to a stable baseline demand.

Application Insights

Fashion and lifestyle applications lead the market with over 55% share in 2025, driven by the transformation of wool felt hats from functional headwear to key fashion accessories. This dominance is fueled by rising fashion consciousness, social media influence, and the growing popularity of vintage-inspired styling. The segment benefits from frequent product innovation, seasonal collections, and designer collaborations, which sustain consumer interest. Outdoor and utility applications remain significant, particularly in regions with colder climates such as North America and parts of Europe, where wool felt hats provide insulation and durability. Cultural and traditional uses continue to support demand in specific geographies, including ceremonial and heritage-driven applications in Europe and Latin America. Additionally, event-based applications—such as weddings, music festivals, and themed gatherings—are emerging as high-growth areas, driven by experiential fashion trends and increasing consumer spending on occasion-based attire.

Distribution Channel Insights

Online retail channels dominate the wool felt hats market, contributing approximately 45% of total sales in 2025. The leadership of this segment is driven by the rapid expansion of e-commerce platforms, global accessibility, and increasing adoption of direct-to-consumer (DTC) models. Consumers benefit from a wider product selection, competitive pricing, and customization options, which are less accessible through traditional retail. Technological advancements such as virtual try-ons, AI-based recommendations, and seamless logistics have further strengthened online adoption. Offline channels, including specialty stores, department stores, and brand-owned outlets, continue to play a crucial role in the premium and luxury segments. These channels offer tactile experiences, personalized fittings, and brand storytelling, which are critical for high-value purchases. The coexistence of both channels reflects an omnichannel strategy adopted by leading brands to maximize market reach and customer engagement.

End-User Insights

Adults aged 25–50 years dominate the market, accounting for nearly 50% of total demand in 2025. This segment leads due to its higher disposable income, strong fashion awareness, and willingness to invest in premium accessories. Consumers in this age group are more likely to purchase wool felt hats for both professional and lifestyle purposes, driving consistent demand across mid-range and premium categories. Younger consumers (below 25 years) are emerging as a fast-growing segment, influenced by social media trends, celebrity endorsements, and online shopping platforms. Their preference for affordable yet stylish products is driving growth in the economy and mid-range segments. Meanwhile, mature consumers (above 50 years) continue to support traditional and functional segments, particularly in regions where hats are associated with cultural identity or practical usage. This demographic also contributes to demand for high-quality, durable products, reinforcing the premium segment.

Explore more data points, trends and opportunities Download Free Sample Report

Wool Felt Hats Market Segmentations

By Product Type

- Fedora Hats

- Cowboy/Western Hats

- Trilby Hats

- Bowler/Derby Hats

- Cloche Hats

- Wide-Brim Felt Hats

- Outdoor/Functional Felt Hats

- Fashion/Designer Felt Hats

By Application

- Fashion & Lifestyle

- Outdoor & Utility

- Cultural & Traditional Use

- Events & Occasions

By Distribution Channel

- Online Retail

- Specialty Stores

- Department Stores

- Brand-Owned Stores

By End-User Age Group

- Youth (Below 25 years)

- Adults (25–50 years)

- Mature Consumers (Above 50 years)

By Price Range

- Economy (Below USD 30)

- Mid-Range (USD 30–100)

- Premium (USD 100–300)

- Luxury (Above USD 300)

Regional Insights

North America

North America leads the global wool felt hats market with approximately 35% share in 2025, with the United States accounting for the majority of regional demand. The region’s dominance is driven by strong cultural affinity for cowboy and western hats, high consumer spending power, and a well-established fashion accessories market. Additionally, the presence of leading heritage brands and robust retail infrastructure supports sustained growth. Seasonal demand in colder regions and the popularity of outdoor activities further contribute to market expansion. The U.S. market alone represents a significant share due to its large consumer base and strong adoption of premium and designer hats.

Europe

Europe holds around 30% of the global market share, led by countries such as the UK, Italy, France, and Germany. The region’s growth is driven by its rich heritage in hat-making, strong demand for premium handcrafted products, and high export capabilities. Italy, in particular, is a global hub for luxury wool felt hats, benefiting from artisanal craftsmanship and strong international demand. The UK maintains a consistent demand due to its tradition of formal headwear and event-based usage. Increasing consumer preference for sustainable and high-quality fashion products is further supporting market growth across Europe.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 7%, driven by rapid urbanization, rising disposable incomes, and increasing exposure to global fashion trends. China leads regional demand due to its large population and expanding middle class, while India is emerging as a high-growth market supported by a young demographic and growing e-commerce penetration. Japan contributes a steady demand through its mature fashion market and preference for high-quality products. The region’s growth is further fueled by digital retail expansion, influencer-driven fashion trends, and increasing adoption of Western-style accessories.

Latin America

Latin America demonstrates moderate growth, with Brazil and Mexico as key markets. The region’s demand is supported by cultural affinity for hats, increasing urbanization, and gradual growth in disposable incomes. Traditional usage, combined with rising interest in fashion accessories, is driving market expansion. Additionally, the growing middle class and increasing penetration of online retail platforms are enabling access to a wider range of products, including premium offerings. However, price sensitivity remains a key factor influencing purchasing decisions in this region.

Middle East & Africa

The Middle East and Africa region is an emerging market, with demand concentrated in GCC countries and South Africa. Growth in the Middle East is driven by high-income consumers, a strong preference for luxury fashion, and increasing adoption of premium accessories. The presence of luxury retail hubs and international brands further supports demand. In Africa, the textile sector and local production capabilities contribute to regional supply, while urbanization and growing fashion awareness are gradually increasing demand. Additionally, climatic conditions in certain regions create functional demand for wool felt hats, supporting steady market growth.

Key Players in the Wool Felt Hats Market

- Stetson

- Borsalino

- Akubra

- Bailey Hats

- Goorin Bros

- Lock & Co. Hatters

- Christys’ London

- Scala Hats

- Dorfman Pacific

- Kangol

- Bollman Hat Company

- Tilley Endurables

- American Hat Company

- Resistol

- Brixton