Women Leather Luxury Footwear Market Size

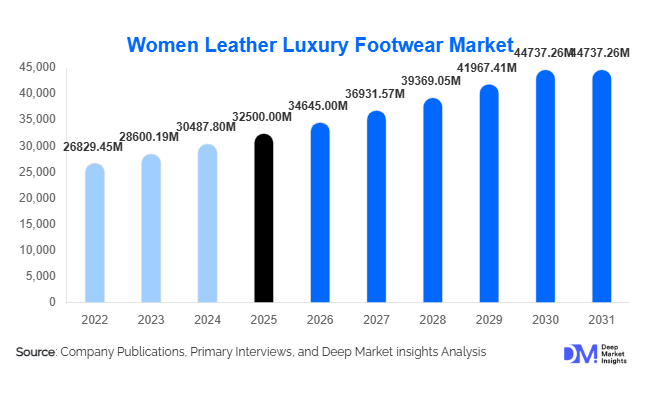

According to Deep Market Insights, the global women leather luxury footwear market size was valued at USD 32,500 million in 2025 and is projected to grow from USD 34,645.00 million in 2026 to reach USD 44,737.26 million by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The market growth is primarily driven by rising global disposable income, increasing penetration of luxury brands in emerging economies, and evolving consumer preferences toward premium, high-quality leather products. The demand for women leather luxury footwear is further supported by growing fashion consciousness, strong brand loyalty, and the expansion of omnichannel retail strategies. Additionally, sustainability initiatives and innovations in leather processing are reshaping product offerings, enabling brands to align with modern ethical expectations while maintaining premium positioning.

Key Market Insights

- Full-grain leather footwear dominates material demand, driven by its premium quality, durability, and strong association with luxury craftsmanship.

- Boots and formal footwear remain leading product categories, supported by high demand in developed regions and strong seasonal sales cycles.

- Europe leads the global market, benefiting from heritage luxury brands and strong export-oriented production.

- Asia-Pacific is the fastest-growing region, driven by rising affluent populations in China, India, and Southeast Asia.

- Core luxury price segment ($500–$1,000) holds the largest share, offering a balance between exclusivity and accessibility.

- Digital transformation and direct-to-consumer channels are significantly reshaping luxury footwear distribution and customer engagement.

What are the latest trends in the women leather luxury footwear market?

Sustainability and Ethical Leather Sourcing

The market is increasingly influenced by sustainability trends, with brands adopting eco-friendly tanning processes, sourcing leather that is traceable, and utilizing biodegradable packaging solutions. Consumers, particularly younger demographics, are prioritizing brands that demonstrate environmental responsibility without compromising luxury appeal. Premium players are investing in vegetable-tanned leather, recycled materials, and alternative premium leather solutions to align with regulatory requirements and consumer expectations. Transparency in the supply chain and certifications related to ethical sourcing are becoming key differentiators in purchase decisions.

Rise of Comfort-Luxury Hybrid Footwear

Changing lifestyles and work environments have accelerated demand for hybrid footwear that combines luxury aesthetics with comfort. Products such as luxury leather sneakers, cushioned loafers, and ergonomic heels are gaining traction globally. This trend reflects a broader shift toward versatility, where consumers seek footwear suitable for both professional and casual settings. Brands are incorporating advanced cushioning technologies, lightweight soles, and flexible leather materials to meet this demand, particularly among urban professionals and younger consumers.

What are the key drivers in the women leather luxury footwear market?

Growing Global Affluent Population

The expansion of high-net-worth individuals (HNWIs) and upper-middle-class consumers is a major driver for the market. Increasing wealth in regions such as Asia-Pacific and the Middle East is fueling demand for premium lifestyle products, including luxury footwear. This segment is characterized by high brand loyalty, preference for exclusivity, and willingness to pay premium prices for quality and craftsmanship.

Strong Brand Equity and Heritage Appeal

Luxury footwear brands benefit from strong heritage, craftsmanship, and brand storytelling, which create emotional connections with consumers. Established European brands, in particular, leverage their legacy and artisanal expertise to command premium pricing and maintain customer loyalty. Limited-edition collections and collaborations further strengthen brand desirability and market positioning.

Expansion of Digital and Omnichannel Retail

The growth of e-commerce and digital platforms has significantly expanded market reach. Luxury brands are investing in direct-to-consumer channels, personalized online experiences, and AI-driven recommendations to enhance customer engagement. Omnichannel strategies, combining physical stores with digital interfaces, are improving accessibility while preserving exclusivity.

What are the restraints for the global market?

High Cost of Raw Materials

Fluctuations in leather prices and increasing costs associated with premium materials pose challenges for manufacturers. Environmental regulations and supply chain disruptions further impact raw material availability, affecting pricing strategies and profit margins.

Rising Sustainability and Ethical Concerns

Increasing scrutiny regarding animal welfare and environmental impact is creating pressure on brands to adopt sustainable practices. Failure to address these concerns can lead to reputational risks and reduced consumer trust, particularly among younger buyers.

What are the key opportunities in the women leather luxury footwear industry?

Expansion in Emerging Markets

Emerging economies, such as China, India, and the UAE, present significant growth opportunities due to rising disposable incomes and the increasing adoption of luxury consumption patterns. Localization strategies, including region-specific designs and pricing, can help brands capture untapped demand in these markets.

Digital Innovation and Personalized Shopping

The integration of advanced technologies such as augmented reality (AR), artificial intelligence (AI), and virtual try-ons is transforming the luxury shopping experience. Brands that invest in personalized digital platforms can enhance customer engagement and improve conversion rates, particularly in online channels.

Sustainable Product Innovation

Developing eco-friendly luxury footwear using alternative materials and sustainable processes presents a strong opportunity for differentiation. Companies that successfully balance sustainability with premium aesthetics are likely to gain a competitive advantage and attract environmentally conscious consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 32500 Million |

| Market Size in 2026 | USD 34645 Million |

| Market Size in 2031 | USD 44737.26 Million |

| CAGR | 6.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Boots continue to dominate the women leather luxury footwear market, accounting for approximately 28% of the 2025 market share. The leadership of this segment is primarily driven by its strong alignment with seasonal demand patterns in North America and Europe, where colder climates necessitate high-quality leather boots. Additionally, boots offer versatility across both formal and casual settings, making them a preferred choice among premium consumers. The ability of luxury brands to introduce innovative designs, such as hybrid boot-sneaker styles and weather-resistant leather, further strengthens this segment’s dominance.

Pumps and sandals hold significant shares due to their essential role in formal and occasion-based wear, particularly in corporate and social environments. Pumps remain a staple in professional wardrobes, while sandals benefit from strong demand in warmer regions and vacation-driven purchases. Luxury sneakers are emerging as the fastest-growing product type, driven by the global shift toward comfort-focused fashion and the integration of athleisure into luxury portfolios. Flats and loafers maintain steady demand, supported by increasing consumer preference for everyday luxury and functional elegance, particularly among urban working women.

Material Insights

Full-grain leather leads the market with an estimated 35% share in 2025, primarily due to its superior durability, natural texture, and premium perception among consumers. This segment’s growth is driven by the increasing emphasis on craftsmanship and product longevity, which are key purchasing factors in the luxury segment. Full-grain leather also supports higher pricing, significantly contributing to the overall market value.

Top-grain and suede leather segments follow, offering a balance between affordability and aesthetics, making them suitable for mid-tier luxury products. Exotic leathers, such as crocodile and ostrich, cater to the ultra-luxury segment, where exclusivity and uniqueness are primary drivers. These materials command significantly higher price points and are often used in limited-edition collections. Meanwhile, vegan and alternative premium leather segments are gaining traction, driven by sustainability concerns and evolving consumer preferences. Innovations in bio-based and lab-grown materials are expected to accelerate growth in this category further.

Distribution Channel Insights

Mono-brand stores dominate the distribution landscape, accounting for approximately 38% of total sales in 2025. Their leadership is driven by the ability to offer a controlled brand environment, personalized customer service, and exclusive product collections, which are critical in maintaining luxury positioning. Flagship stores in major fashion capitals also serve as brand experience centers, reinforcing customer loyalty.

Multi-brand luxury retail stores continue to play a significant role, particularly in metropolitan areas, where they provide consumers with access to multiple premium brands under one roof. However, online retail is the fastest-growing channel, driven by increasing consumer confidence in purchasing luxury goods digitally. The expansion of direct-to-consumer (D2C) platforms, combined with advancements in virtual try-ons and AI-driven personalization, is driving a surge in online sales. Duty-free and travel retail channels also contribute significantly, supported by the recovery of global tourism and increased spending by international travelers.

End-Use Insights

The fashion and lifestyle industry remains the primary end-use segment, supported by a global market exceeding USD 1.7 trillion. The demand is largely driven by the integration of luxury footwear into broader fashion ecosystems, including apparel and accessories. Corporate and professional use continues to drive demand for formal footwear, particularly pumps and loafers, as workplace dressing standards evolve toward premium yet comfortable options.

Casual and athleisure segments are witnessing the fastest growth, driven by changing work environments, including hybrid and remote working models, which have increased demand for versatile and comfortable luxury footwear. The travel and tourism sector also plays a significant role, particularly through duty-free retail channels in Europe and the Asia-Pacific region, where luxury purchases are often linked to international travel. Export-driven demand remains strong, with European countries such as Italy and France serving as major production hubs that supply high-value footwear to global markets.

Explore more data points, trends and opportunities Download Free Sample Report

Women Leather Luxury Footwear Market Segmentations

By Product Type

- Pumps

- Sandals

- Boots

- Loafers & Moccasins

- Sneakers

- Flats

- Others

By Material Type

- Full-Grain Leather

- Top-Grain Leather

- Patent Leather

- Suede Leather

- Exotic Leather

- Vegan/Alternative Leather

By Distribution Channel

- Mono-brand Stores

- Multi-brand Retail Stores

- Online Retail

- Duty-Free & Travel Retail

By End-Use/Application

- Formal Wear

- Casual Wear

- Party/Evening Wear

- Seasonal Wear

By Age Group

- 18–30 years

- 31–45 years

- 46–60 years

- 60+ years

Regional Insights

Europe

Europe is expected to hold the largest share, approximately 34%, in 2025, driven by countries such as Italy, France, and the UK. The region’s dominance is supported by its strong heritage in luxury craftsmanship, presence of globally renowned brands, and well-established supply chains. Italy serves as a key manufacturing hub, exporting premium leather footwear worldwide. Additionally, high tourist inflows and strong domestic demand for luxury goods further boost regional growth. Government support for traditional leather industries and stringent quality standards also enhance Europe’s competitive advantage.

North America

North America accounts for around 28% of the market, with the United States leading demand. The region benefits from high disposable income levels, strong brand awareness, and a mature luxury retail ecosystem. Growth is further driven by the rapid adoption of digital luxury platforms, enabling seamless online purchasing experiences. Additionally, the presence of a large working professional population supports demand for formal and semi-formal luxury footwear. Seasonal demand, particularly for boots and winter footwear, also contributes significantly to market growth in this region.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 8%. China dominates regional demand, contributing over 40% of the market, followed by Japan, South Korea, and India. Growth in this region is driven by rising disposable incomes, rapid urbanization, and an expanding middle-class population aspiring to own luxury products. The increasing influence of social media and digital platforms is also shaping consumer behavior, particularly among younger demographics. Additionally, the expansion of luxury retail networks and localized product offerings are accelerating market penetration across key countries.

Middle East & Africa

The Middle East, particularly the UAE and Saudi Arabia, shows strong demand driven by high-income consumers, luxury-oriented lifestyles, and a well-developed retail infrastructure. The region’s growth is further supported by increasing tourism and the presence of luxury shopping destinations such as Dubai. In Africa, the market is gradually expanding due to rising urbanization and improving economic conditions. However, growth remains concentrated in select urban centers. Increasing investments in retail infrastructure and the expansion of international luxury brands are expected to drive future growth in the region.

Latin America

Latin America holds a smaller share but is experiencing steady growth, led by Brazil and Mexico. The region’s growth is driven by increasing fashion awareness, the expansion of the urban middle class, and rising exposure to global luxury trends. Economic stabilization in key countries is also supporting consumer spending on premium products. Additionally, the expansion of international luxury brands into major cities and the growth of e-commerce platforms are enhancing accessibility and driving demand across the region.