Women’s Casual Shoes Market Size

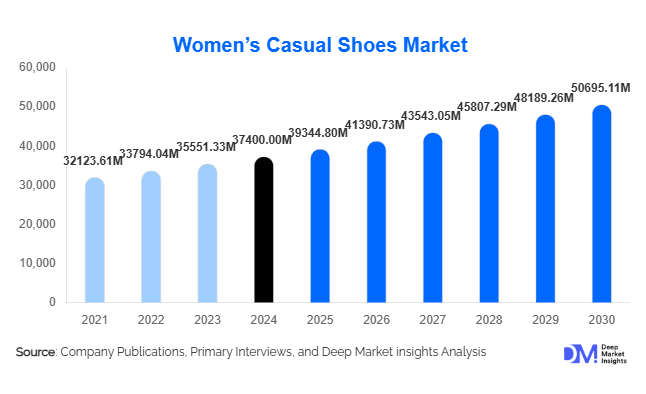

According to Deep Market Insights, the global women's casual shoes market size was valued at USD 37,400.00 million in 2025 and is projected to grow from USD 39,344.80 million in 2026 to reach USD 50,695.11 million by 2031, expanding at a CAGR of 5.2% during the forecast period (2026–2031). The market growth is primarily driven by increasing urbanization, rising disposable income among women, growing preference for stylish yet comfortable footwear, and the proliferation of e-commerce platforms that provide wider access to global brands.

Key Market Insights

- Sneakers and flats continue to dominate the women’s casual shoes market, fueled by athleisure trends and the increasing importance of comfort combined with fashion appeal.

- Online and e-commerce channels are expanding rapidly, enabling direct-to-consumer sales and personalized offerings, which are reshaping buying behavior globally.

- North America leads in market share, with the U.S. and Canada driving demand for both premium and mid-range casual footwear due to high disposable income and fashion-conscious consumers.

- Asia-Pacific is the fastest-growing region, led by China, India, and Southeast Asia, due to rising middle-class income, urbanization, and increasing adoption of international footwear brands.

- Technological integration in footwear, including smart insoles, ergonomic designs, and sustainable material innovations, is attracting health-conscious and environmentally-aware consumers.

- Luxury and mid-range segments are expanding, driven by consumers seeking high-quality materials such as leather and eco-friendly alternatives combined with trendy designs.

Women’s Casual Shoes Market Trends

Athleisure and Lifestyle Adoption

The global market is witnessing a significant shift toward athleisure and lifestyle-inspired casual shoes. Sneakers are increasingly being worn outside traditional sports or gym settings, blending seamlessly with everyday wear. Influencer-driven trends on social media platforms are further reinforcing the demand for fashionable yet functional footwear. Consumers now prioritize versatility, looking for shoes suitable for work, casual outings, and travel, encouraging brands to innovate designs that combine performance features with style.

Sustainable and Eco-Friendly Footwear

Sustainability has become a key driver in consumer decision-making. Brands are integrating recycled materials, biodegradable components, and eco-conscious manufacturing processes to appeal to environmentally-aware buyers. The market for sustainable women’s casual shoes is expected to grow rapidly, as younger demographics show a willingness to pay a premium for products that align with their ethical and environmental values. Eco-certifications and transparent supply chains are becoming critical differentiators in competitive positioning.

Women’s Casual Shoes Market Drivers

Rising Female Workforce Participation

Globally, the increasing number of women joining professional and corporate environments is driving demand for stylish, comfortable casual footwear that can be used in multiple settings. This segment, particularly in North America and Europe, accounts for nearly 28% of market growth in 2025. Functional yet fashionable shoes such as loafers, flats, and sneakers are increasingly preferred by working women for daily wear and commuting purposes.

Urbanization and Changing Lifestyle Preferences

Urban consumers are adopting a fast-paced, convenience-oriented lifestyle, which favors casual footwear that is versatile, easy to wear, and aesthetically appealing. Sneakers and slip-ons dominate in metropolitan areas, representing about 65% of global sales in 2025. Athleisure and casual chic trends continue to drive product development and influence consumer purchasing decisions.

Digital Influence and E-Commerce Penetration

The growing role of digital platforms is a major market driver. E-commerce adoption allows consumers in urban and semi-urban areas to access a wider range of brands and products. Social media platforms and fashion apps influence purchase decisions and help brands engage directly with younger consumers. Online sales accounted for 34% of the market in 2025, expected to grow further with integrated omnichannel strategies and AI-driven personalization tools.

Women’s Casual Shoes Market Restraints

Raw Material Price Volatility

Fluctuations in leather, synthetic polymers, and textile costs impact production and profitability, particularly for smaller players. Rising raw material prices can lead to higher retail prices, limiting affordability and potentially slowing market expansion in price-sensitive regions.

Intense Competition

The women’s casual shoes market is highly fragmented, with numerous international and regional brands competing on price, design, and quality. High competition creates pricing pressures and challenges in maintaining brand loyalty. Differentiating products through innovation, sustainability, and technological features is critical for market players to retain and grow market share.

Women’s Casual Shoes Market Opportunities

Expansion in Emerging Economies

Emerging markets in Asia-Pacific (China, India, Southeast Asia) and Latin America present significant growth potential due to rising urban populations, increasing disposable income, and shifting fashion preferences. E-commerce adoption in these regions enhances accessibility to global and local brands. Companies establishing local production or marketing hubs can tap into growing consumer demand efficiently.

Integration of Smart and Sustainable Technologies

Technological innovation in footwear, including health-tracking insoles, ergonomic designs, and eco-friendly materials, offers opportunities to differentiate products. Brands focusing on sustainability and smart features are able to cater to health-conscious and environmentally aware consumers, tapping into premium market segments.

Direct-to-Consumer Channel Expansion

Direct-to-consumer (DTC) channels enable brands to optimize margins, enhance personalization, and gather consumer data. Omni-channel strategies integrating online and offline stores allow seamless shopping experiences. Subscription models, customization platforms, and loyalty programs provide additional revenue streams while strengthening customer retention and engagement.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 37400 Million |

| Market Size in 2026 | USD 39344.80 Million |

| Market Size in 2031 | USD 50695.11 Million |

| CAGR | 5.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Sneakers / athletic shoes lead the market with a 42% share in 2025, driven by athleisure trends and multi-purpose usage across urban and semi-urban consumers. Loafers and flats remain significant for office and casual wear, with growing demand for ergonomic designs and sustainable materials. Sandals and slip-ons are gaining traction in warmer climates and for casual everyday use. The mid-range ($50–$150) segment holds a 46% market share, balancing affordability and quality.

Material Insights

Leather-based casual shoes dominate at 38% of the market due to durability, premium appeal, and comfort. Synthetic and canvas materials are growing in emerging markets, offering cost-effective alternatives with lightweight and flexible designs. Rubber and EVA soles remain popular for sneakers and sandals, catering to urban and athleisure demand.

Distribution Channel Insights

Online and e-commerce channels lead at 34% market share, allowing consumers to access multiple brands, compare prices, and enjoy doorstep delivery. Retail stores, department stores, and exclusive brand outlets remain important for experiential shopping and brand exposure. Digital engagement, social media campaigns, and influencer marketing are increasingly shaping consumer purchasing patterns.

End-Use Insights

Young adults (20–35 years) represent the fastest-growing segment, contributing 40% of the market in 2025. Demand is driven by urban millennials seeking trendy yet comfortable footwear for work, leisure, and social activities. Emerging industries such as wellness, outdoor recreation, and professional lifestyle sectors are creating new applications for casual footwear. Export-driven demand from North America and Europe remains strong, particularly for premium and mid-range products.

Explore more data points, trends and opportunities Download Free Sample Report

Women’s Casual Shoes Market Segmentations

By Product Type

- Sneakers / Athletic Shoes

- Flats / Ballerinas

- Loafers & Moccasins

- Slip-ons

- Sandals & Slides

- Espadrilles

- Wedges

By Material Type

- Leather

- Synthetic / PU Leather

- Canvas / Fabric

- Rubber / EVA

- Suede

By Price Range

- Economy (Under USD 50)

- Mid-Range (USD 50–150)

- Premium (USD 150–300)

- Luxury (Above USD 300)

By Distribution Channel

- Online / E-commerce

- Specialty Footwear Stores

- Department Stores

- Exclusive Brand Outlets

- Hypermarkets & Supermarkets

By End User

- Teenagers (13–19 Years)

- Young Adults (20–35 Years)

- Adults (36–50 Years)

- Older Adults (50+ Years)

Regional Insights

North America

North America holds the largest market share at 28% in 2025, with the U.S. leading due to high disposable income, fashion-conscious consumers, and robust e-commerce penetration. Canada also contributes significantly, with sneakers and flats dominating urban consumption. Demand is driven by professional women and the athleisure trend.

Europe

Europe accounts for 24% of the global market in 2025, with Germany, the UK, and France as major contributors. Growth is fueled by rising urbanization, disposable income, and strong adoption of mid-range and premium casual footwear. Younger demographics show increasing interest in sustainable and eco-friendly products.

Asia-Pacific

Asia-Pacific is the fastest-growing region with a CAGR of 8.5% during 2026–2031. China, India, and Japan are leading the growth due to rising middle-class income, e-commerce penetration, and urbanization. Demand for branded footwear and international trends are reshaping the market landscape.

Latin America

Brazil, Argentina, and Mexico are emerging markets for women’s casual shoes. Outbound demand and rising imports of branded footwear are boosting growth, particularly in urban centers.

Middle East & Africa

Premium and imported casual shoes drive demand in GCC countries. South Africa is a key market in Africa, with urban fashion trends encouraging the adoption of international brands.