Wireless Power Bank Market Size

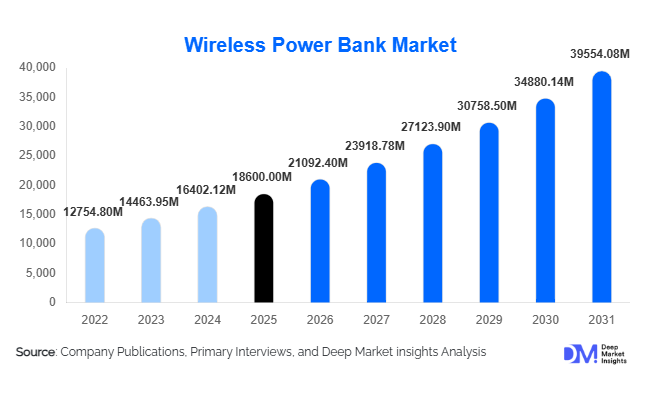

According to Deep Market Insights, the global wireless power bank market size was valued at USD 18,600 million in 2025 and is projected to grow from USD 21,092.40 million in 2026 to reach USD 39,554.08 million by 2031, expanding at a CAGR of 13.4% during the forecast period (2026–2031). The wireless power bank market growth is primarily driven by the increasing adoption of wireless charging-enabled smartphones, the rapid expansion of portable consumer electronics, and the rising demand for convenient cable-free charging solutions.

Wireless power banks enable portable energy storage and wireless power transfer using inductive or magnetic charging technologies. As smartphones, smartwatches, wireless earbuds, and other portable devices increasingly incorporate wireless charging compatibility, the demand for wireless charging accessories has accelerated globally. Consumers are prioritizing convenience, portability, and multi-device charging capabilities, making wireless power banks a key accessory within the mobile electronics ecosystem.

Technological advancements such as magnetic alignment charging, high-capacity lithium batteries, and fast wireless charging standards are further strengthening market growth. Manufacturers are also focusing on compact designs, improved thermal management, and integrated charging solutions to enhance usability. With the expansion of mobile lifestyles, remote work trends, and digital connectivity worldwide, wireless power banks are transitioning from optional accessories into essential mobile charging solutions.

Key Market Insights

- Rising smartphone penetration and wireless charging adoption are driving strong demand for wireless power banks globally.

- Magnetic wireless charging ecosystems are expanding rapidly, particularly among premium smartphone users.

- Asia-Pacific dominates the market, supported by strong consumer electronics manufacturing and high mobile device usage.

- North America represents the largest premium accessories market, driven by high consumer spending and the adoption of advanced charging technologies.

- Online retail channels lead global distribution, enabling direct-to-consumer sales and wider product availability.

- Product innovation, such as fast wireless charging and multi-device compatibility, is reshaping the competitive landscape.

What are the latest trends in the wireless power bank market?

Magnetic Wireless Charging Ecosystems Expanding

Magnetic wireless charging technology has emerged as one of the most influential trends in the wireless power bank market. Magnetic alignment ensures optimal positioning between the power bank and the device, improving charging efficiency and stability compared with traditional inductive wireless charging. These power banks attach securely to smartphones, enabling convenient charging during travel or daily use.

Premium smartphone ecosystems are increasingly adopting magnetic charging compatibility, which has accelerated demand for magnetically aligned wireless power banks. Manufacturers are responding by launching compact and lightweight products with integrated magnets, high-capacity batteries, and faster charging speeds. This trend has also enabled slimmer form factors and improved portability, making magnetic wireless power banks particularly popular among frequent travelers and mobile professionals.

Multi-Device Wireless Charging Solutions

Another significant trend shaping the market is the development of wireless power banks capable of charging multiple devices simultaneously. Modern consumers often carry several portable electronics, including smartphones, smartwatches, wireless earbuds, and tablets. As a result, there is increasing demand for power banks that support simultaneous charging of multiple devices.

Manufacturers are integrating multiple wireless charging coils, USB-C fast charging ports, and intelligent power management systems to support multi-device charging. These products appeal strongly to professionals and travelers who require reliable portable charging solutions for multiple devices. As the ecosystem of wireless-charging-enabled devices continues to expand, multi-device wireless power banks are expected to gain substantial market traction.

What are the key drivers in the wireless power bank market?

Growing Global Smartphone and Wearable Device Adoption

The rapid increase in smartphone and wearable device usage worldwide remains a major driver of the wireless power bank market. Smartphones have become essential tools for communication, entertainment, navigation, and work, resulting in higher power consumption and increased demand for portable charging solutions. As more smartphone manufacturers integrate wireless charging capabilities into mid-range and flagship devices, the adoption of compatible wireless accessories continues to grow.

Wearable electronics such as smartwatches and wireless earbuds have further increased demand for wireless power banks capable of charging multiple devices simultaneously. Consumers prefer cable-free charging solutions that provide flexibility during travel, commuting, or outdoor activities.

Expansion of Wireless Charging Standards

The widespread adoption of standardized wireless charging technologies, particularly Qi wireless charging, has significantly boosted market growth. Standardization ensures compatibility between devices and charging accessories produced by different manufacturers, enabling consumers to charge their devices with a wide range of wireless power banks.

Technological advancements in wireless charging efficiency, coil design, and power management chips have also improved charging speeds and reduced energy losses. These improvements have addressed early concerns regarding slow wireless charging performance, making wireless power banks a practical and convenient solution for everyday charging needs.

What are the restraints for the global market?

Lower Charging Efficiency Compared with Wired Charging

Despite improvements in wireless charging technologies, wired charging remains faster and more energy efficient than wireless charging. Wireless power transfer typically results in some energy loss due to heat generation and electromagnetic interference, which can reduce charging efficiency. For consumers requiring rapid device charging, wired power banks may still be preferred over wireless alternatives.

Manufacturers continue to address this limitation by improving coil alignment technologies, integrating fast wireless charging protocols, and enhancing heat dissipation systems. However, the efficiency gap between wired and wireless charging remains a technical challenge for the industry.

Higher Product Costs in Premium Segments

Wireless power banks typically cost more than conventional wired power banks due to the additional hardware required for wireless charging functionality. Components such as charging coils, magnetic alignment systems, and advanced power management circuits increase manufacturing costs.

Premium wireless power banks offering fast charging capabilities, high-capacity batteries, and multi-device charging functionality often carry significantly higher price points. For price-sensitive consumers, particularly in developing markets, traditional power banks may remain a more affordable option, potentially limiting wireless power bank adoption in certain segments.

What are the key opportunities in the wireless power bank industry?

Growing Demand in Emerging Markets

Emerging economies across Asia-Pacific, Latin America, and Africa present significant opportunities for wireless power bank manufacturers. Smartphone penetration continues to grow rapidly in countries such as India, Indonesia, Brazil, and Vietnam, creating strong demand for mobile accessories.

Increasing digital connectivity, expanding middle-class populations, and growing e-commerce penetration are supporting the distribution and adoption of wireless charging accessories. Manufacturers that offer competitively priced products tailored to local consumer preferences are likely to capture significant market share in these high-growth regions.

Integration with IoT and Smart Device Ecosystems

The rapid expansion of the Internet of Things (IoT) ecosystem presents new opportunities for wireless power banks beyond smartphone charging. Devices such as smartwatches, wireless earbuds, portable gaming consoles, and IoT-enabled gadgets are increasingly integrating wireless charging compatibility.

Wireless power banks capable of charging multiple device types simultaneously are becoming increasingly popular among consumers. Companies that develop innovative charging solutions designed for multi-device ecosystems will benefit from the growing demand within the smart device market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18600 Million |

| Market Size in 2026 | USD 21092.40 Million |

| Market Size in 2031 | USD 39554.08 Million |

| CAGR | 13.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Battery Type Insights

Lithium-ion batteries dominate the wireless power bank market, accounting for approximately 62% of global demand in 2025. Their dominance is primarily driven by superior energy density, lightweight construction, and relatively lower manufacturing costs compared with alternative battery chemistries such as lithium-polymer or nickel-based batteries. Lithium-ion batteries enable compact product designs while still providing sufficient capacity to recharge modern smartphones and wearable devices multiple times. The technology also offers stable output voltage, longer lifecycle performance, and strong safety features when integrated with modern battery management systems.

Another factor driving the dominance of lithium-ion batteries is the maturity of the global supply chain supporting their production. Large-scale battery manufacturing ecosystems in China, South Korea, and Japan have significantly reduced production costs while improving battery performance and reliability. These economies of scale allow wireless power bank manufacturers to produce high-capacity portable chargers at competitive prices, making them accessible to a wide range of consumers. Furthermore, lithium-ion batteries integrate efficiently with fast-charging circuits and wireless power transfer technologies, enabling improved charging speeds and power management. As demand for portable consumer electronics continues to rise globally, manufacturers are increasingly relying on lithium-ion battery technology to balance performance, durability, and cost efficiency. These advantages ensure that lithium-ion batteries will continue to remain the leading battery type within the wireless power bank market over the forecast period.

Capacity Insights

Wireless power banks with a capacity range of 5,000–10,000 mAh represent the largest segment of the market, holding nearly 34% of global market share in 2025. This capacity range has emerged as the preferred option among consumers because it provides an ideal balance between portability and charging capability. A power bank within this capacity range can typically recharge a standard smartphone one to two times, which is sufficient for daily use scenarios such as commuting, traveling, or attending events.

The popularity of this segment is also driven by its compact size and lightweight form factor. Consumers increasingly prioritize portable accessories that can easily fit into pockets, handbags, or backpacks without adding significant bulk. Power banks with capacities above 10,000 mAh often offer greater charging capability but tend to be heavier and less convenient for everyday carry, which limits their adoption among casual users. Additionally, the 5,000–10,000 mAh category is widely adopted by accessory brands because it allows them to integrate wireless charging coils, fast-charging ports, and safety features without significantly increasing product dimensions. As smartphones become more power-intensive due to larger displays and higher processing requirements, manufacturers are continuing to optimize battery efficiency within this capacity segment, ensuring it remains the leading category in the wireless power bank market.

Technology Insights

Inductive wireless charging remains the most widely used technology in the wireless power bank market, accounting for approximately 58% of global adoption in 2025. The dominance of inductive charging technology is largely attributed to its compatibility with the Qi wireless charging standard, which has become the global benchmark for wireless power transfer in smartphones and consumer electronics. The Qi standard enables seamless interoperability between devices and charging accessories manufactured by different companies, which has significantly accelerated adoption. Most major smartphone brands now integrate Qi wireless charging support into their flagship and mid-range devices, ensuring compatibility with a wide range of wireless power banks available in the market.

Another factor supporting the growth of inductive charging technology is its reliability and ease of integration into compact devices. Inductive charging systems rely on electromagnetic coils that transfer power between the charger and the device when placed in close proximity. Continuous improvements in coil design, power management chips, and thermal dissipation technologies have improved charging efficiency and reduced heat generation. Manufacturers are also combining inductive charging with magnetic alignment technologies to enhance charging stability and user convenience. As wireless charging becomes a standard feature across consumer electronics, inductive wireless power transfer is expected to remain the dominant technology used in wireless power banks worldwide.

Distribution Channel Insights

Online retail platforms dominate global wireless power bank distribution, accounting for nearly 41% of total sales in 2025. The rapid expansion of e-commerce has transformed the consumer electronics accessories market by enabling customers to access a wide range of products, compare prices, and review product specifications before making a purchase decision. Major online marketplaces and direct-to-consumer brand websites have become key distribution channels for wireless power bank manufacturers. These platforms provide manufacturers with global reach and allow them to sell products without relying heavily on traditional retail networks. Online platforms also enable frequent product launches, promotional discounts, and bundled accessory offers that encourage consumers to purchase charging accessories alongside smartphones and other devices.

Digital marketing and influencer-driven product promotions have also contributed significantly to online sales growth. Consumers increasingly rely on product reviews, social media recommendations, and technology blogs when selecting portable charging devices. As internet penetration continues to increase globally and mobile commerce becomes more prevalent, online retail channels are expected to maintain their leadership position in the wireless power bank distribution ecosystem.

End-Use Insights

Individual consumers represent the largest end-user segment for wireless power banks, accounting for a significant portion of total market demand. This segment is driven primarily by the rapid growth of the global consumer electronics industry, particularly smartphones, tablets, wireless earbuds, smartwatches, and portable gaming devices. As modern consumers rely heavily on mobile devices for communication, entertainment, navigation, and productivity, the need for reliable portable charging solutions has increased substantially. The global smartphone installed base continues to expand, and many new devices now support wireless charging capabilities. This technological shift has accelerated demand for wireless-compatible charging accessories, including wireless power banks. Consumers increasingly prefer cable-free charging options that provide convenience and flexibility during travel, commuting, and outdoor activities.

Commercial applications are also gradually emerging as an important growth area within the market. Hotels, airports, cafés, and coworking spaces are adopting wireless charging solutions to enhance customer convenience and improve user experiences. Corporate environments are also integrating portable charging solutions to support employees who frequently travel or work remotely. Furthermore, industries such as logistics, field services, event management, and outdoor recreation are beginning to adopt wireless power banks to support mobile workforce operations. These emerging commercial applications are expected to contribute to steady demand growth in the coming years.

Explore more data points, trends and opportunities Download Free Sample Report

Wireless Power Bank Market Segmentations

By Battery Type

- Lithium-Ion Batteries

- Lithium-Polymer Batteries

- Other Emerging Battery Technologies

By Capacity

- Below 5,000 mAh

- 5,000–10,000 mAh

- 10,000–20,000 mAh

- Above 20,000 mAh

By Technology

- Inductive Wireless Charging

- Resonant Wireless Charging

- RF-Based Wireless Charging

By Distribution Channel

- Online Retail

- Electronics & Specialty Stores

- Supermarkets & Hypermarkets

- Brand Stores

- Telecom Operator Stores

By End-Use

- Individual Consumers

- Commercial & Enterprise Applications

- Travel & Hospitality

- Industrial & Field Workforce

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest share of the wireless power bank market, accounting for approximately 41% of global demand in 2025. The region’s dominance is driven by its strong consumer electronics manufacturing ecosystem, high smartphone penetration, and rapidly expanding e-commerce infrastructure. China represents the largest market in the region due to its extensive electronics manufacturing capabilities and strong domestic demand for mobile accessories. Cities such as Shenzhen and Guangzhou serve as major global production hubs for wireless charging devices and portable power solutions.

India is emerging as one of the fastest-growing markets within Asia-Pacific, supported by rapid smartphone adoption, expanding digital connectivity, and increasing consumer spending on mobile accessories. Government initiatives encouraging electronics manufacturing and growing online retail penetration are further strengthening market growth. Other countries such as South Korea, Japan, and Southeast Asian markets are also contributing to demand due to high technology adoption rates and growing consumer electronics usage.

North America

North America represents nearly 23% of the global wireless power bank market, with the United States accounting for the majority of regional demand. High adoption of premium smartphones with wireless charging capabilities has significantly increased demand for compatible charging accessories. Consumers in the region also demonstrate strong purchasing power and a willingness to invest in high-performance technology products.

The growing popularity of remote work, digital lifestyles, and mobile entertainment has further increased the need for reliable portable charging solutions. Additionally, the presence of major consumer electronics brands and accessory manufacturers in the United States supports continuous product innovation. Retailers and technology companies in North America frequently launch advanced wireless power banks with fast charging capabilities, which helps drive regional market growth.

Europe

Europe accounts for approximately 19% of global wireless power bank demand, with key markets including Germany, the United Kingdom, France, Italy, and Spain. European consumers often prioritize premium electronic accessories that combine advanced functionality with durable design and sustainability considerations.

Growing environmental awareness has encouraged manufacturers to develop eco-friendly accessories, including power banks made with recyclable materials and improved battery efficiency. The increasing adoption of wireless charging-enabled smartphones across the region has also accelerated demand for compatible accessories. Strong retail networks and widespread availability of consumer electronics further support steady growth in the European wireless power bank market.

Latin America

Latin America represents a smaller but steadily expanding market for wireless power banks. Brazil and Mexico are the largest markets in the region due to their large populations and rising smartphone adoption rates. Expanding internet connectivity, growing e-commerce penetration, and increasing digitalization are encouraging consumers to invest in mobile accessories. The demand for portable charging solutions is also increasing as consumers rely more heavily on smartphones for mobile payments, online entertainment, and social media engagement. As wireless charging technology becomes more widely integrated into smartphones available in the region, adoption of wireless power banks is expected to grow steadily.

Middle East & Africa

The Middle East and Africa region is gradually emerging as a promising market for wireless power banks. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are experiencing increasing demand for premium mobile accessories due to high smartphone penetration and rising disposable incomes.

Urbanization and expanding digital infrastructure are also driving demand for portable charging solutions across major metropolitan areas. In addition, the growth of tourism, business travel, and mobile workforce activities in the region has increased the need for reliable portable power solutions. As consumer electronics adoption continues to expand and wireless charging technology becomes more common in smartphones, the wireless power bank market in the Middle East and Africa is expected to witness steady growth over the coming years.

Key Players in the Wireless Power Bank Market

- Anker Innovations

- Samsung Electronics

- Xiaomi Corporation

- Belkin International

- Mophie (ZAGG Inc.)

- AUKEY

- Zendure

- Baseus

- RAVPower

- Huawei Technologies

- Lenovo Group

- Sony Corporation

- Panasonic Corporation

- Energizer Holdings

- Spigen