Wet & Dry Vacuum Cleaners Market Size

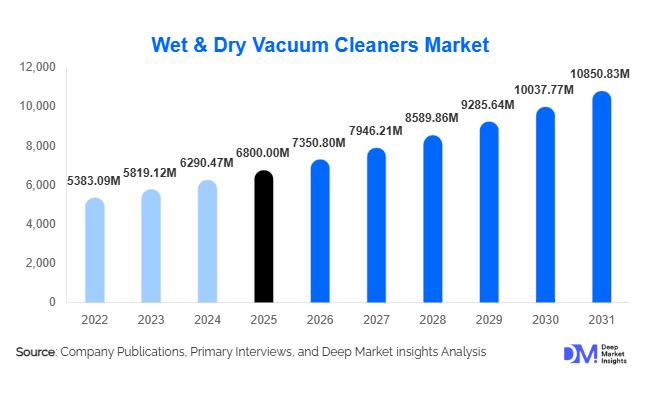

According to Deep Market Insights, the global wet & dry vacuum cleaners market size was valued at USD 6,800 million in 2025 and is projected to grow from USD 7,350.80 million in 2026 to reach USD 10,850.83 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The market growth is primarily driven by increasing hygiene awareness across residential and commercial spaces, rapid industrialization, and rising demand for multifunctional cleaning equipment capable of handling both liquid and solid waste. Additionally, advancements in cordless technology, HEPA filtration systems, and energy-efficient motors are further accelerating product adoption across diverse end-use industries.

Key Market Insights

- Industrial and commercial sectors dominate demand, driven by the increasing need for efficient cleaning solutions in manufacturing, warehousing, and hospitality industries.

- Asia-Pacific leads the global market, supported by strong manufacturing activity and rising urban household adoption in countries like China and India.

- Cordless vacuum cleaners are gaining rapid traction, particularly in residential and light commercial applications, due to ease of use and portability.

- HEPA filtration systems are increasingly preferred, driven by rising awareness of indoor air quality and allergen control.

- Offline retail remains dominant, as consumers prefer product demonstrations and after-sales service support.

- Technological innovations, including smart sensors and IoT-enabled devices, are transforming traditional vacuum cleaners into intelligent cleaning systems.

What are the latest trends in the wet & dry vacuum cleaners market?

Shift Toward Cordless and Smart Cleaning Solutions

The market is witnessing a significant shift toward cordless and battery-powered vacuum cleaners, driven by consumer demand for convenience and mobility. These products eliminate the limitations of cord length and power outlets, making them ideal for residential and small commercial spaces. Additionally, manufacturers are integrating smart technologies such as IoT connectivity, automated suction control, and app-based monitoring. These advancements enhance user experience and enable predictive maintenance, making cleaning systems more efficient and user-friendly.

Rising Adoption of Advanced Filtration Technologies

Increasing concerns regarding indoor air quality are driving the adoption of advanced filtration systems, particularly HEPA and multi-stage filtration technologies. These systems are highly effective in capturing fine dust particles, allergens, and pollutants, making them suitable for healthcare facilities, offices, and households. Manufacturers are also focusing on eco-friendly and reusable filters, aligning with sustainability trends and regulatory requirements. This shift is particularly prominent in developed markets, where environmental and health standards are stringent.

What are the key drivers in the wet & dry vacuum cleaners market?

Growing Emphasis on Hygiene and Cleanliness

Rising awareness regarding hygiene, particularly after the COVID-19 pandemic, has significantly increased demand for advanced cleaning equipment. Both residential and commercial users are investing in efficient cleaning solutions to maintain sanitary environments. This trend is especially strong in urban areas, where higher population density necessitates frequent cleaning and maintenance.

Expansion of Industrial and Construction Activities

The growth of the manufacturing, warehousing, and construction sectors is a major driver for the market. These industries require high-capacity vacuum cleaners to manage dust, debris, and liquid waste effectively. Wet & dry vacuum cleaners are increasingly becoming essential tools in these environments, supporting operational efficiency and compliance with safety standards.

Technological Advancements and Product Innovation

Continuous innovation in motor efficiency, battery technology, and filtration systems is enhancing product performance and attracting a broader customer base. Features such as energy efficiency, noise reduction, and compact designs are appealing to both residential and commercial users. Premium models with smart capabilities are also contributing to higher market value growth.

What are the restraints for the global market?

High Initial Cost of Advanced Models

Advanced wet & dry vacuum cleaners equipped with HEPA filters, smart features, and high-capacity motors often come with higher price points. This limits adoption among price-sensitive consumers, particularly in developing regions and small-scale enterprises.

Maintenance and Operational Challenges

Industrial-grade vacuum cleaners require regular maintenance, including filter replacement and motor servicing. These operational complexities can increase the total cost of ownership and deter adoption, especially among small businesses with limited technical expertise.

What are the key opportunities in the wet & dry vacuum cleaners industry?

Expansion in Emerging Markets

Emerging economies in Asia-Pacific, Latin America, and Africa present significant growth opportunities due to rapid urbanization, increasing disposable incomes, and rising awareness of hygiene. Government initiatives promoting cleanliness and infrastructure development are further supporting demand for advanced cleaning equipment in these regions.

Integration of Smart and IoT Technologies

The incorporation of smart features such as IoT connectivity, automated operation, and real-time monitoring is opening new avenues for product differentiation. These technologies not only improve efficiency but also enable predictive maintenance, reducing downtime and operational costs for users.

Growth in Industrial and Commercial Applications

The expansion of organized retail, logistics hubs, and large-scale industrial facilities is driving demand for high-performance vacuum cleaners. Stringent safety and cleanliness regulations are compelling businesses to adopt advanced cleaning solutions, creating opportunities for manufacturers to target high-value industrial segments.

Product Type Insights

Wet & dry canister vacuum cleaners continue to dominate the global market, accounting for approximately 32% of the total market share in 2025. Their leadership is primarily driven by their high versatility, allowing users to efficiently handle both liquid spills and dry debris across diverse environments such as households, offices, and small commercial establishments. The compact yet powerful design, ease of mobility, and cost-effectiveness compared to industrial models make canister vacuums the preferred choice globally. Additionally, manufacturers are increasingly integrating advanced filtration systems and ergonomic designs into canister models, further strengthening their dominance. Drum and industrial vacuum cleaners represent a critical segment in heavy-duty applications, particularly in construction sites, manufacturing plants, and large warehouses. Their high-capacity tanks (often exceeding 30 liters) and powerful suction capabilities make them indispensable for industrial cleaning tasks. This segment is benefiting from rising industrial automation and stricter workplace safety regulations, which require efficient dust and debris management systems.

Meanwhile, upright and handheld wet & dry vacuum cleaners are gaining traction, especially in residential and light commercial applications. Their compact size, lightweight design, and ease of storage are key growth drivers. Increasing demand for portable and quick-cleaning solutions in urban households is accelerating adoption, particularly in developed markets where convenience is a primary purchasing factor.

Application Insights

Commercial cleaning applications lead the wet & dry vacuum cleaners market, accounting for approximately 38% share in 2025. This dominance is driven by the rapid expansion of office spaces, retail outlets, hotels, and healthcare facilities, all of which require frequent and efficient cleaning solutions. The growing emphasis on maintaining hygiene standards in customer-facing environments, particularly in hospitality and healthcare, is a major driver for this segment. Additionally, the outsourcing of facility management services is further boosting demand for high-performance cleaning equipment. Industrial applications follow closely, accounting for approximately 34% of the market share. The segment’s growth is primarily fueled by increasing manufacturing output, expansion of logistics and warehousing infrastructure, and rising construction activities globally. Wet & dry vacuum cleaners are essential in these environments for managing hazardous dust, liquid waste, and debris, ensuring compliance with occupational safety regulations.

The residential segment is witnessing the fastest growth, supported by rising urbanization, increasing disposable incomes, and growing awareness of hygiene. Consumers are increasingly adopting multifunctional cleaning appliances that offer convenience and efficiency. The trend toward smart homes and connected appliances is also encouraging the adoption of advanced vacuum cleaners with automated features and enhanced usability.

Distribution Channel Insights

Offline retail channels dominate the market, accounting for nearly 60% of the total share in 2025. The continued preference for offline purchasing is driven by the need for physical product demonstrations, especially for high-value appliances. Consumers often rely on in-store experiences to assess product performance, build quality, and usability before making a purchase. Additionally, strong after-sales service support and immediate product availability further reinforce the dominance of offline channels.

However, online retail is emerging as the fastest-growing distribution channel, driven by increasing e-commerce penetration, particularly in emerging economies. Competitive pricing, wider product selection, and the convenience of home delivery are key factors contributing to this growth. Manufacturers are also investing heavily in direct-to-consumer (D2C) platforms, leveraging digital marketing, personalized recommendations, and subscription-based services to enhance customer engagement and brand loyalty.

End-Use Industry Insights

The industrial sector remains the largest end-use segment, contributing approximately 34% of the market share in 2025. This dominance is driven by the continuous expansion of manufacturing facilities, warehouses, and construction projects worldwide. Industrial users require durable, high-capacity vacuum cleaners capable of handling heavy-duty cleaning tasks, making wet & dry vacuum cleaners a critical component of operational efficiency and workplace safety compliance. The commercial sector, including hospitality, retail, and office spaces, is among the fastest-growing segments. Increasing focus on cleanliness, customer experience, and regulatory compliance is driving demand for advanced cleaning equipment in this sector. The growth of organized retail and global tourism is further amplifying demand for efficient cleaning solutions.

The residential sector is also witnessing significant growth, particularly in emerging economies across Asia-Pacific and Latin America. Rising disposable incomes, urban lifestyle changes, and increasing awareness of hygiene are encouraging consumers to invest in advanced home cleaning appliances. The growing popularity of compact, cordless, and smart vacuum cleaners is further supporting expansion in this segment.

| By Product Type | By Application | By Distribution Channel |

|---|---|---|

|

|

|

Regional Insights

Asia-Pacific

The Asia-Pacific region leads the global wet & dry vacuum cleaners market, accounting for approximately 38% of the total share in 2025, and is also the fastest-growing region, with a CAGR exceeding 9%. China dominates the regional market due to its large-scale manufacturing sector, which generates substantial demand for industrial cleaning equipment. Additionally, China’s position as a global manufacturing hub supports both domestic consumption and export-driven demand.

India is emerging as a high-growth market, driven by rapid urbanization, rising middle-class income, and government initiatives such as cleanliness campaigns and infrastructure development. Increasing penetration of household appliances and expansion of organized retail are further boosting demand. Japan and South Korea contribute through strong adoption of technologically advanced and energy-efficient cleaning solutions. Overall, the region’s growth is driven by industrial expansion, urban population growth, and rising consumer awareness of hygiene.

North America

North America holds approximately 25% of the global market share, with the United States being the largest contributor. The region’s growth is driven by high adoption of advanced cleaning technologies across commercial and industrial sectors. Strong presence of large office spaces, retail chains, and healthcare facilities creates consistent demand for high-performance vacuum cleaners. Additionally, high consumer purchasing power and early adoption of smart home technologies are supporting the residential segment. The growing trend of automation and integration of IoT-enabled cleaning devices is further accelerating market growth. Regulatory standards related to workplace safety and indoor air quality are also key drivers in this region.

Europe

Europe accounts for around 22% of the global market share, led by countries such as Germany, the United Kingdom, and France. The region’s growth is strongly influenced by stringent environmental regulations and high standards for indoor air quality, which are driving demand for vacuum cleaners equipped with advanced filtration systems such as HEPA. Additionally, the presence of established industrial and automotive sectors supports steady demand for industrial cleaning equipment. Sustainability trends, including energy-efficient appliances and eco-friendly product designs, are also shaping market dynamics. Increasing adoption of smart and connected home appliances is further contributing to growth in the residential segment.

Middle East & Africa

The Middle East & Africa region contributes approximately 8% of the global market share. Growth in this region is primarily driven by rapid infrastructure development, particularly in the Gulf Cooperation Council (GCC) countries such as the UAE and Saudi Arabia. Expansion of the hospitality and tourism sectors is creating strong demand for commercial cleaning equipment. Additionally, increasing investments in construction and real estate projects are boosting demand for industrial vacuum cleaners. In Africa, gradual urbanization and improving economic conditions are supporting the adoption of basic cleaning appliances, although the market remains price-sensitive.

Latin America

Latin America holds nearly 7% of the global market share, with Brazil and Mexico being the key contributors. The region’s growth is driven by expanding industrial activities, particularly in manufacturing and automotive sectors, which require efficient cleaning solutions. Retail sector growth and increasing penetration of modern trade formats are also contributing to demand in commercial applications. Additionally, rising urbanization and improving consumer purchasing power are supporting the adoption of household appliances, including wet & dry vacuum cleaners. However, economic fluctuations and price sensitivity remain key challenges in this region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Wet & Dry Vacuum Cleaners Market

- Kärcher

- Nilfisk Group

- Bosch

- Stanley Black & Decker

- Panasonic

- LG Electronics

- Samsung Electronics

- Makita Corporation

- Hitachi

- Dyson

- Techtronic Industries (TTI)

- Shop-Vac

- Bissell

- Electrolux

- Alfred Kärcher SE & Co. KG