Waterless Cosmetics Market Size

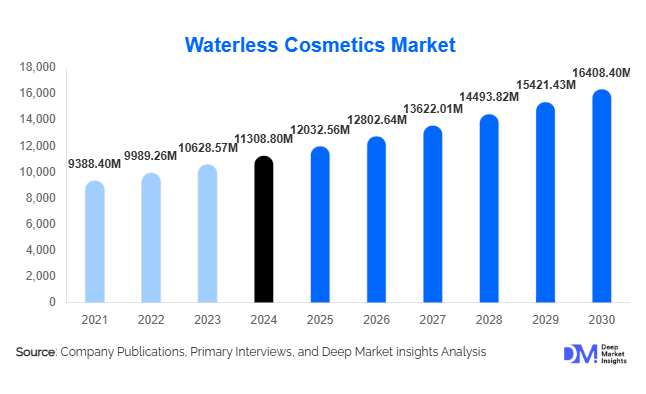

According to Deep Market Insights, the global waterless cosmetics market size was valued at USD 11,308.80 million in 2025 and is projected to grow from USD 12,032.56 million in 2026 to reach USD 16,408.40 million by 2031, expanding at a CAGR of 6.40% during the forecast period (2026–2031). The waterless cosmetics market growth is primarily driven by rising consumer demand for eco-friendly beauty solutions, increasing adoption of travel-friendly product formats, and expansion of online and emerging market channels focused on sustainable personal care products.

Key Market Insights

- Waterless cosmetics are aligning with sustainability trends, offering products with minimal water footprint and eco-friendly packaging to appeal to environmentally conscious consumers.

- Travel-friendly and compact formulations are on the rise, including solid shampoo bars, powder foundations, and stick serums that cater to on-the-go lifestyles.

- Asia-Pacific dominates the market, with China, India, Japan, and South Korea driving demand due to rising disposable income, eco-awareness, and adoption of premium beauty routines.

- North America remains a significant and fast-growing market, with the U.S. leading adoption through e-commerce penetration and clean-beauty awareness.

- Europe is emphasizing sustainable and ethical formulations, supported by EU regulations, consumer awareness, and premium retail penetration.

- Technological integration in product development and e-commerce platforms, including D2C and subscription models, is reshaping consumer engagement with waterless cosmetics.

Waterless Cosmetics Market Trends

Eco-Conscious Formulation Adoption

Brands are increasingly focusing on water-free and low-water formulations, leveraging solid bars, powders, and concentrated sticks. These products reduce environmental impact while offering longer shelf-life and higher active ingredient concentration. Certifications such as cruelty-free, vegan, and organic labels further enhance appeal to conscious consumers. The trend is reinforced by marketing campaigns emphasizing reduced water use and minimal packaging waste, positioning waterless products as premium and environmentally responsible alternatives.

Online and Direct-to-Consumer Channels Driving Growth

Emerging brands and established players alike are expanding online sales through e-commerce platforms and D2C channels. Subscription box models and social media marketing allow consumers to experience niche waterless products conveniently. Online platforms also provide educational content on usage and sustainability, helping overcome consumer hesitation regarding unfamiliar textures or application methods. The convenience and accessibility of digital platforms are accelerating adoption, particularly among younger demographics.

Waterless Cosmetics Market Drivers

Rising Sustainability and Eco-Awareness

Environmental consciousness is a primary driver of waterless cosmetics growth. Consumers increasingly prefer brands that minimize water usage and packaging waste. This trend is amplified by global sustainability initiatives and the growing prominence of "clean beauty" movements, encouraging manufacturers to innovate formulations that reduce environmental impact without compromising performance.

Innovation in Travel-Friendly Formats

Solid bars, powder foundations, and stick serums appeal to mobile, on-the-go lifestyles. These formats are lightweight, spill-proof, and convenient for travel, making them increasingly popular among frequent travelers and urban consumers. Brands that innovate compact, portable products are capturing premium pricing and higher adoption rates in both developed and emerging markets.

Emerging Market Penetration

Emerging markets in Asia-Pacific, Latin America, and the Middle East are witnessing rapid growth due to increasing disposable incomes, rising interest in sustainable beauty, and expanding e-commerce reach. These regions represent a key growth opportunity for both established players and new entrants seeking to leverage untapped demand.

Waterless Cosmetics Market Restraints

Consumer Awareness and Acceptance

Some consumers are hesitant to switch from traditional aqueous formulations due to unfamiliar textures and application methods. Education campaigns and trial initiatives are critical for overcoming this barrier and driving mainstream adoption.

Formulation Complexity and Cost

Waterless products require alternative preservatives, specialized solid or powder formulations, and unique packaging solutions, which can increase manufacturing costs. These complexities may constrain pricing competitiveness and limit adoption among cost-sensitive consumers.

Waterless Cosmetics Market Opportunities

Premium and Sustainable Product Expansion

Brands can capitalize on the rising demand for eco-conscious products by developing premium waterless formulations that emphasize sustainability, concentrated active ingredients, and reduced packaging. Opportunities exist to target both luxury and mid-range segments by leveraging clean beauty credentials and innovative formats.

Travel and On-the-Go Product Innovation

The growing mobility of consumers presents opportunities for compact, portable, and spill-proof formats. Solid shampoos, powders, stick serums, and multi-purpose products allow brands to capture travel-oriented demand, increase cross-selling potential, and differentiate their offerings in saturated markets.

Emerging Market Expansion

Untapped regions such as India, Southeast Asia, the Middle East, and Latin America offer high growth potential. Brands can invest in localized formulations, educational campaigns, and e-commerce platforms to reach new consumer segments seeking sustainable, innovative beauty solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11308.80 Million |

| Market Size in 2026 | USD 12032.56 Million |

| Market Size in 2031 | USD 16408.40 Million |

| CAGR | 6.40% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Skincare dominates the market, accounting for approximately 33% of 2025 sales, driven by high consumer familiarity and adoption. Haircare, makeup, and body care products also contribute significantly, with haircare bars and solid makeup formats gaining traction. Skincare’s lead is attributed to concentrated active formulations, longer shelf life, and the ease of transitioning traditional routines to waterless formats.

Application Insights

Daily personal care routines remain the largest application for waterless cosmetics. Travel-focused and portable formats are growing rapidly, complemented by male grooming and unisex product demand. Professional salons, spas, and subscription boxes provide additional growth channels. Export-driven demand from developed markets to emerging economies is further expanding application opportunities.

Distribution Channel Insights

Online retail dominates with 40% of the market in 2025, leveraging D2C websites, e-commerce marketplaces, and subscription models. Offline channels, including specialty beauty stores, supermarkets, and department stores, account for the remaining 60%. The shift to online is accelerating adoption, enhancing consumer education, and enabling global brand reach.

Gender Insights

The women's segment leads with an 80% share in 2025, reflecting higher product adoption and spending. Men and unisex categories are emerging rapidly, especially in grooming and multifunctional product lines. These trends indicate potential for expansion into previously underserved segments.

Explore more data points, trends and opportunities Download Free Sample Report

Waterless Cosmetics Market Segmentations

By Product Type

- Skincare

- Haircare

- Makeup

- Body Care

- Other Personal Care Products

By Application

- Daily Personal Care

- Travel and On-the-Go

- Male Grooming

- Professional/Salon Use

- Subscription Boxes

By Distribution Channel

- Online Retail (E-Commerce, D2C)

- Specialty Beauty Stores

- Department Stores

- Supermarkets & Hypermarkets

- Pharmacies & Drug Stores

Regional Insights

North America

North America accounts for 20% of the 2025 market. The U.S. leads in adoption due to high consumer awareness, e-commerce penetration, and premium beauty preferences. Growth is further supported by eco-conscious and travel-friendly product demand.

Europe

Europe represents 18% of the market, with the U.K., Germany, and France leading. Sustainability regulations and ethical consumer preferences drive adoption, with premium skincare and haircare leading demand.

Asia-Pacific

Asia-Pacific dominates with 42% of the 2025 market share. China, India, Japan, and South Korea are the largest contributors, driven by rising disposable income, sustainability awareness, and innovative beauty routines. India and Southeast Asia are among the fastest-growing markets in the region.

Latin America

Latin America accounts for 10% of the market, with Brazil, Argentina, and Mexico driving growth. Consumers are increasingly adopting premium and eco-conscious beauty products, supported by digital retail expansion.

Middle East & Africa

MEA holds 10% of the market, with the UAE, Saudi Arabia, and South Africa leading. High-income populations, luxury beauty preferences, and travel retail hubs support growth. The UAE is the fastest-growing country in the region due to premium consumer demand.

Key Players in the Waterless Cosmetics Market

- L’Oréal S.A.

- The Procter & Gamble Company

- Unilever Plc

- Kao Corporation

- The Estée Lauder Companies Inc.

- Johnson & Johnson

- Coty Inc.

- Henkel AG & Co. KGaA

- Amway Corp.

- Shiseido Company, Ltd.

- Loli Beauty PBC

- Clensta International Private Limited

- Pinch of Colour

- Ruby’s Organics

- Carter + Jane

Recent Developments

- In May 2025, L’Oréal expanded its waterless skincare portfolio with new solid serums and shampoo bars focused on sustainability and reduced water footprint.

- In April 2025, Unilever launched a range of travel-friendly solid haircare products in Asia-Pacific, tapping emerging market demand.

- In February 2025, Estée Lauder introduced powder-based foundations and compact sticks in North America, promoting eco-conscious packaging and concentrated formulations.