Water Fountain Market Size

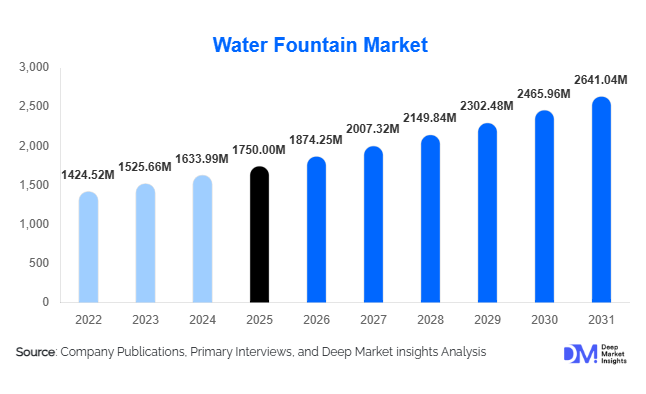

According to Deep Market Insights, the global water fountain market size was valued at USD 1,750 million in 2025 and is projected to grow from USD 1,874.25 million in 2026 to reach USD 2,641.04 million by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). The water fountain market growth is primarily driven by urban beautification projects, rising adoption of smart and energy-efficient fountain technologies, and increasing investments in tourism and hospitality sectors that emphasize aesthetic and interactive water features.

Key Market Insights

- Decorative and musical fountains continue to dominate demand globally, enhancing aesthetics in commercial, public, and tourism-driven spaces.

- Smart and IoT-enabled fountains are gaining traction, with remote monitoring, programmable jets, and energy-efficient pumps reshaping market expectations.

- Asia-Pacific leads in market share, driven by rapid urbanization, smart city initiatives, and large-scale infrastructure investments in China and India.

- North America holds a significant share, with strong demand for retrofit and modernization projects, especially in public infrastructure and commercial properties.

- Public infrastructure projects are the fastest-growing end-use segment, fueled by government spending on parks, urban squares, and civic beautification.

- Technological integration, including solar-powered pumps, programmable LED lighting, and IoT-based maintenance systems, is transforming both commercial and public fountain installations.

What are the latest trends in the water fountain market?

Smart and Energy-Efficient Fountains

Fountains with integrated IoT sensors, programmable lighting, and solar-powered pumps are increasingly being deployed across commercial, public, and residential applications. These smart systems allow operators to monitor water usage, optimize energy consumption, and schedule automated maintenance alerts. Solar and low-energy pumps are becoming mainstream, particularly in regions with strict environmental regulations, positioning water fountains as sustainable infrastructure solutions. IoT-enabled designs also support programmable water shows and interactive experiences, increasing the appeal of fountains in public and entertainment spaces.

Decorative and Experiential Installations

Decorative and musical fountains are being used to enhance urban aesthetics and visitor engagement in parks, hotels, resorts, and shopping complexes. Large-scale installations incorporating choreographed lighting and water displays are becoming key attractions in tourism-centric locations. Public and private clients increasingly demand customizable fountains with premium materials such as granite, marble, and stainless steel, combining functionality with visual appeal. This trend is particularly evident in luxury commercial and tourism-driven infrastructure.

What are the key drivers in the water fountain market?

Urbanization and Infrastructure Development

Rapid urbanization and investments in public infrastructure, especially in Asia-Pacific and the Middle East, are driving demand for water fountains in parks, transportation hubs, and civic spaces. Governments prioritize urban beautification projects to improve public engagement and city aesthetics, positioning water fountains as essential urban elements. Greenfield urban projects and retrofits in developed markets are creating significant installation opportunities for both decorative and drinking fountains.

Hospitality and Tourism Expansion

The growing hospitality sector, particularly hotels, resorts, and entertainment venues, is investing heavily in decorative and musical fountains to enhance visitor experiences. These installations serve as iconic attractions, differentiating properties while boosting brand value. Luxury and mid-scale hotels are incorporating custom-designed water features in their landscaping, lobbies, and outdoor spaces, further strengthening market growth.

Adoption of Smart Technologies

The integration of smart technologies, such as IoT-enabled pumps, programmable lighting, and remote monitoring, is transforming the water fountain market. Commercial and public sectors increasingly prefer these solutions for energy savings, predictive maintenance, and interactive visual displays. Smart fountains align with sustainability goals and provide added value in both residential and commercial projects.

What are the restraints for the global market?

High Installation and Maintenance Costs

Large-scale decorative and musical fountains require substantial capital investments, including design, engineering, installation, and ongoing maintenance. This restricts adoption among budget-constrained municipalities and small-scale commercial developers. High costs can also limit demand in regions with low public or private spending capacity.

Water Scarcity and Regulatory Restrictions

In water-stressed regions, strict regulations limit fountain installations or require costly water recycling and conservation systems. Compliance with such regulations adds to operational complexity and increases the total cost of ownership, potentially slowing market adoption.

What are the key opportunities in the water fountain market?

Smart City and Urban Beautification Projects

Governments in Asia-Pacific, the Middle East, and Europe are investing in smart city projects, integrating IoT-enabled fountains with urban planning. This provides opportunities for manufacturers and service providers to offer programmable, interactive, and energy-efficient fountain solutions. Smart fountains with digital monitoring and interactive features cater to public spaces, tourist hubs, and commercial complexes.

Sustainable and Eco-Friendly Fountains

The rising focus on sustainability presents opportunities for solar-powered, low-energy, and recycled-water fountains. Regulatory frameworks and environmental certifications in Europe and North America encourage manufacturers to innovate in eco-friendly water features. This trend supports premium pricing and aligns with the global emphasis on energy efficiency and water conservation.

Hospitality and Tourism Sector Expansion

The rapid growth of luxury resorts, hotels, and entertainment venues in the Middle East and Asia-Pacific creates demand for large-scale decorative and musical fountains. Customized installations that combine visual appeal, interactivity, and sustainability allow new entrants and existing players to capture high-value contracts. Retrofitting aging infrastructure in mature markets also presents recurring revenue opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1750 Million |

| Market Size in 2026 | USD 1874.25 Million |

| Market Size in 2031 | USD 2641.04 Million |

| CAGR | 7.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Decorative fountains continue to dominate the global water fountain market, accounting for approximately 42% of total demand in 2025. The leadership of this segment is primarily driven by increasing investments in urban beautification, commercial real estate development, and hospitality infrastructure. Decorative fountains enhance visual appeal and property value, making them a preferred choice for hotels, malls, corporate campuses, and public parks. The growing trend of experiential spaces and aesthetically designed urban environments is further reinforcing demand for customized and large-scale decorative installations. Drinking fountains are witnessing steady growth, supported by rising awareness around public health, hygiene, and sustainability. Governments and institutions are actively promoting drinking water infrastructure to reduce reliance on single-use plastic bottles, especially across schools, universities, transportation hubs, and healthcare facilities. Meanwhile, musical fountains are gaining traction in tourism-driven economies, where synchronized water, light, and sound displays are used to create iconic attractions that boost visitor engagement.

Smart and interactive fountains represent the fastest-growing segment, driven by increasing adoption of IoT-enabled systems, programmable controls, and energy-efficient technologies. These fountains are particularly appealing to smart city developers and premium commercial projects, where automation, remote monitoring, and dynamic water displays provide both operational efficiency and enhanced user experience.

Application Insights

Public infrastructure remains the leading application segment, contributing approximately 38% of the global market share in 2025. This dominance is driven by large-scale government investments in urban development, including parks, recreational areas, city squares, and transportation hubs. Water fountains are increasingly being integrated into public spaces to improve urban aesthetics, promote community engagement, and support tourism initiatives. The rise of smart city programs across Asia-Pacific and the Middle East further accelerates demand in this segment. Commercial applications, including hotels, resorts, shopping malls, and office complexes, represent a significant share of the market. The growth of the hospitality and retail sectors is a key driver, as businesses invest in visually appealing water features to enhance customer experience and differentiate their properties. Residential applications are also expanding, particularly in high-income regions, where homeowners are incorporating decorative fountains into landscaping and luxury property designs.

The entertainment and tourism sectors are emerging as high-growth application areas, driven by increasing demand for immersive and interactive attractions. Musical and programmable fountains are being widely adopted in theme parks, event venues, and tourist destinations, serving as focal points that enhance visitor engagement and drive footfall.

Distribution Channel Insights

Direct sales dominate the water fountain market, accounting for nearly 70% of total revenue, as most installations are executed through large-scale projects, government tenders, and commercial contracts. The complexity and customization involved in fountain installations necessitate direct engagement between manufacturers, contractors, and end users, making this channel the most effective for high-value projects. The growth of turnkey solution providers is a key driver within this segment, as clients increasingly prefer vendors who can offer end-to-end services, including design, installation, maintenance, and system integration. This approach reduces project risk and ensures long-term operational efficiency, further strengthening the dominance of direct sales.

Retail and online channels are gaining momentum, particularly for residential and small-scale commercial fountains. E-commerce platforms and home improvement stores are enabling wider accessibility, offering standardized and modular fountain solutions. Digital marketing, product visualization tools, and online customization options are also influencing purchasing decisions, especially among individual consumers and small businesses.

End-Use Insights

The commercial and hospitality sectors remain the largest end-use segments, driven by continuous expansion in global tourism and hotel infrastructure. Hotels, resorts, and commercial complexes increasingly invest in decorative and interactive fountains to enhance brand image, create premium experiences, and attract customers. This segment benefits from strong capital expenditure and a focus on experiential design. Public infrastructure is the fastest-growing end-use segment, supported by rising government spending on smart cities, urban renewal projects, and civic amenities. The integration of fountains into parks, public squares, and transportation hubs reflects a broader trend toward creating sustainable and visually appealing urban environments.

Emerging end-use segments include healthcare and educational institutions, where drinking fountains are being installed to promote hygiene and sustainability. Entertainment venues and tourism destinations are also driving demand for advanced fountain systems, particularly musical and interactive installations. Additionally, export-driven demand remains strong, with countries such as China and Germany playing a critical role in supplying fountain components and systems to global markets.

Explore more data points, trends and opportunities Download Free Sample Report

Water Fountain Market Segmentations

By Product Type

- Decorative Fountains

- Drinking Water Fountains

- Musical/Dancing Fountains

- Smart/Interactive Fountains

By Application

- Public Infrastructure

- Commercial

- Residential

- Institutional

- Entertainment & Tourism

By Distribution Channel

- Direct Sales

- Retail Stores

- Online/E-commerce Platforms

Regional Insights

Asia-Pacific

Asia-Pacific leads the global water fountain market, accounting for approximately 35% of total demand in 2025. China dominates the region due to extensive urban development, large-scale infrastructure projects, and strong manufacturing capabilities. India is emerging as a high-growth market, driven by smart city initiatives, urban beautification programs, and increasing investments in public infrastructure. Southeast Asian countries and Australia are also contributing to growth through expanding tourism infrastructure and commercial real estate development. Key growth drivers in this region include rapid urbanization, government-led infrastructure spending, and rising demand for smart and sustainable urban solutions.

North America

North America represents around 25% of the global market, with the United States accounting for the majority of regional demand. Growth in this region is primarily driven by the modernization and retrofit of aging infrastructure, along with the strong adoption of advanced and smart fountain technologies. Public parks, commercial complexes, and institutional facilities are key demand centers. Additionally, sustainability regulations and increasing emphasis on water conservation are encouraging the adoption of energy-efficient and recycled-water fountain systems, further supporting market growth.

Europe

Europe holds approximately 22% of the global market share, led by countries such as Germany, France, and Italy. The region’s growth is driven by strict environmental regulations, strong focus on sustainability, and high demand for aesthetically designed urban spaces. European cities are investing in eco-friendly and energy-efficient fountain systems, particularly those using recycled water and low-energy pumps. Heritage conservation and urban renewal projects also contribute significantly to demand, especially for stone-based and architecturally integrated fountain designs.

Middle East & Africa

The Middle East is the fastest-growing regional market, driven by large-scale investments in luxury tourism, hospitality, and urban development. Countries such as the UAE and Saudi Arabia are investing heavily in iconic infrastructure projects, including high-end hotels, entertainment hubs, and smart cities, where decorative and musical fountains play a central role. Africa is also witnessing gradual growth, particularly in tourism-centric countries such as South Africa, Kenya, and Botswana. Key growth drivers include tourism expansion, government-led megaprojects, and increasing demand for premium and experiential infrastructure.

Latin America

Latin America accounts for approximately 8% of the global market, with Brazil and Mexico being the primary contributors. Growth in this region is supported by expanding commercial infrastructure, urban redevelopment projects, and increasing investments in tourism and hospitality. While the market remains relatively smaller compared to other regions, niche demand for decorative fountains in public spaces and commercial properties is steadily increasing. Economic recovery, infrastructure investments, and growing interest in urban beautification are key drivers supporting long-term market growth in the region.

Key Players in the Water Fountain Market

- WET Design

- OASE GmbH

- Crystal Fountains

- Kasco Marine

- Safe-Rain

- Fontana Fountains

- Aqua Control

- Hall Fountains

- Pentair

- Otterbine Barebo

- Lumiartecnia Internacional

- Fountain People

- Delta Fountains

- AquaMaster Fountains

- Atlantic Water Gardens