Water Dispenser Market Size

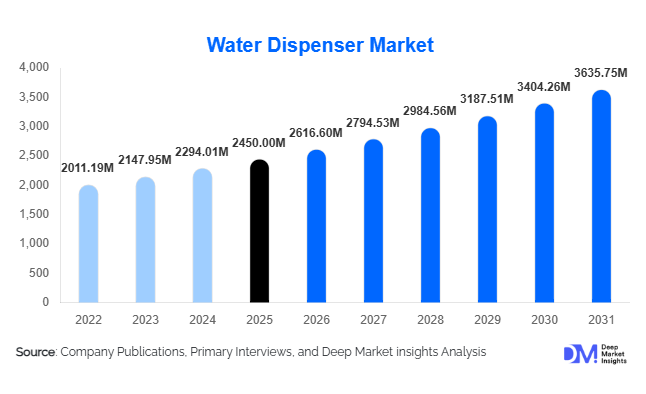

According to Deep Market Insights, the global water dispenser market size was valued at USD 2,450 million in 2025 and is projected to grow from USD 2,616.60 million in 2026 to reach USD 3,635.75 million by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The water dispenser market growth is primarily driven by rising awareness of safe drinking water, increasing adoption across commercial spaces such as offices and healthcare facilities, and growing demand for convenient and energy-efficient hydration solutions. Technological advancements, including smart dispensers, touchless interfaces, and integrated filtration systems, are further accelerating market expansion globally.

Key Market Insights

- Bottle-less (point-of-use) dispensers are gaining significant traction, driven by sustainability goals and reduced operational costs.

- Commercial end-users dominate demand, particularly offices, healthcare institutions, and hospitality sectors.

- Asia-Pacific is the fastest-growing region, fueled by urbanization and rising water quality concerns in emerging economies.

- Hot and cold multifunctional dispensers lead product demand, accounting for the largest share due to versatility.

- Smart and touchless technologies are reshaping product innovation, especially in post-pandemic environments.

- Rental and subscription-based models are emerging, lowering upfront costs and increasing adoption among SMEs and households.

What are the latest trends in the water dispenser market?

Shift Toward Bottle-less and Sustainable Solutions

The market is witnessing a strong shift toward bottle-less water dispensers that connect directly to water supply systems and incorporate advanced filtration technologies such as reverse osmosis and UV purification. These systems eliminate the need for plastic bottles, reducing environmental impact and logistics costs. Organizations are increasingly adopting these solutions to meet ESG targets and sustainability commitments. Additionally, governments and corporate entities are promoting plastic reduction initiatives, further accelerating the adoption of eco-friendly dispenser systems across developed markets.

Smart and Touchless Dispenser Adoption

Technological innovation is transforming water dispensers into intelligent appliances. Touchless dispensing systems using sensors are becoming standard in offices and public spaces to enhance hygiene. IoT-enabled dispensers allow remote monitoring of water usage, filter life, and maintenance schedules, improving operational efficiency. Mobile app integration and real-time quality monitoring are also gaining traction, particularly in premium product segments. These advancements are attracting tech-savvy consumers and enabling manufacturers to differentiate through value-added features.

What are the key drivers in the water dispenser market?

Rising Demand for Safe and Purified Drinking Water

Increasing concerns over water contamination and health risks are driving demand for water dispensers equipped with advanced filtration systems. Urban populations, particularly in developing countries, are prioritizing safe drinking water solutions, boosting both residential and commercial adoption.

Expansion of Commercial Infrastructure

The rapid growth of office spaces, co-working environments, hospitals, and educational institutions is significantly contributing to market expansion. Corporate wellness initiatives and regulatory requirements for workplace hygiene are further supporting the installation of water dispensers in commercial environments.

What are the restraints for the global market?

High Initial Costs of Advanced Systems

Advanced water dispensers, particularly bottle-less and smart variants, involve higher upfront costs compared to traditional models. This limits adoption in price-sensitive markets and among small-scale users.

Maintenance and Operational Challenges

Regular maintenance, including filter replacement and sanitation, increases long-term costs and operational complexity. Lack of proper servicing infrastructure in certain regions can further hinder adoption.

What are the key opportunities in the water dispenser industry?

Emerging Market Expansion

Rapid urbanization and improving living standards in emerging economies such as India, Indonesia, and parts of Africa present significant growth opportunities. Increasing awareness about water safety and government initiatives for clean water access are driving demand in these regions.

Integration of Smart and IoT Technologies

The integration of IoT and smart monitoring systems offers opportunities for manufacturers to create premium product segments. Features such as predictive maintenance, energy optimization, and real-time monitoring enhance user experience and operational efficiency.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2450 Million |

| Market Size in 2026 | USD 2616.60 Million |

| Market Size in 2031 | USD 3635.75 Million |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Bottle-less (point-of-use) water dispensers continue to dominate the global market, accounting for approximately 38% of total market share in 2025. This leadership is primarily driven by their long-term cost efficiency, elimination of recurring bottled water logistics, and strong alignment with sustainability goals. Organizations across corporate offices, healthcare facilities, and educational institutions are increasingly transitioning toward these systems to reduce plastic waste and operational expenses. Additionally, regulatory pressure and ESG commitments in developed markets are accelerating the adoption of bottleless systems.

Bottled water dispensers still maintain a significant presence, particularly in regions with underdeveloped water infrastructure or inconsistent municipal supply. These systems offer reliability and ease of installation, making them suitable for rural and semi-urban markets. Meanwhile, countertop and compact dispensers are witnessing rising adoption in residential segments due to space constraints in urban housing, especially in the Asia-Pacific and Europe. Freestanding dispensers remain the most widely deployed format globally, driven by their higher capacity, durability, and suitability for high-traffic commercial environments such as offices, factories, and public facilities.

Technology Insights

Compressor-based cooling technology leads the market with over 55% share in 2025, primarily due to its superior cooling efficiency, durability, and ability to handle high-volume usage in commercial and institutional environments. These systems are particularly preferred in regions with warmer climates, where consistent cooling performance is critical. The dominance of compressor technology is further reinforced by its compatibility with large-capacity freestanding units used in offices and industrial facilities.

In parallel, filtration technologies are becoming a critical differentiator in product offerings. Reverse osmosis (RO), UV purification, and ultrafiltration systems are increasingly integrated into modern dispensers, addressing growing concerns over water contamination and safety. This trend is especially prominent in emerging markets, where water quality issues are more prevalent. Additionally, advancements in multi-stage filtration and mineral enhancement technologies are enabling manufacturers to offer premium products with enhanced health benefits. The integration of smart monitoring systems to track filter life and water quality is further strengthening the adoption of technologically advanced dispensers across both residential and commercial segments.

End-Use Insights

The commercial segment dominates the water dispenser market, accounting for approximately 50% of total demand in 2025. This dominance is driven by the rapid expansion of office spaces, co-working hubs, healthcare facilities, and hospitality establishments. Corporate wellness initiatives, employee hygiene standards, and regulatory requirements for safe drinking water are key factors supporting this segment’s leadership. High consumption volumes and the need for continuous water supply make commercial environments the primary adopters of advanced and high-capacity dispensers.

The residential segment is the fastest-growing, with growth driven by increasing urbanization, rising disposable incomes, and heightened awareness of water quality and health. Consumers are increasingly investing in compact, aesthetically designed, and multi-functional dispensers for home use. Additionally, the growing trend of smart homes is encouraging the adoption of IoT-enabled dispensers. Institutional demand, including schools, universities, and government buildings, is also expanding steadily, particularly in developing regions. Government initiatives focused on public health and access to clean drinking water are playing a crucial role in driving adoption within this segment.

Distribution Channel Insights

Direct sales channels account for approximately 40% of the market, primarily driven by bulk procurement through B2B contracts in commercial and institutional sectors. Large organizations prefer direct partnerships with manufacturers for customized solutions, maintenance services, and long-term cost benefits. Retail and e-commerce channels are witnessing rapid growth, fueled by increasing digital adoption and consumer preference for convenience. Online platforms offer a wide range of product options, competitive pricing, and access to customer reviews, making them particularly attractive for residential buyers.

Rental and subscription-based models are emerging as a transformative distribution strategy, especially in urban markets. These models reduce upfront costs and include maintenance services, making them highly appealing for small businesses and households. This shift toward “water-as-a-service” is expected to significantly reshape distribution dynamics over the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Water Dispenser Market Segmentations

By Product Type

- Bottled Water Dispensers

- Bottle-less (Point-of-Use) Water Dispensers

- Countertop Water Dispensers

- Freestanding Water Dispensers

By Technology

- Compressor-Based Cooling

- Thermoelectric Cooling

- Reverse Osmosis (RO) Filtration

- UV & Ultrafiltration Systems

By End-Use

- Residential

- Commercial

- Institutional

- Industrial

By Distribution Channel

- Direct Sales (B2B)

- Retail Stores

- E-commerce Platforms

- Rental & Subscription-Based Models

Regional Insights

North America

North America holds approximately 30% of the global market share in 2025, with the United States accounting for the majority of demand. The region’s growth is driven by widespread adoption of bottle-less dispensers in corporate offices, healthcare facilities, and educational institutions. Strong regulatory standards for water quality, combined with high awareness of hygiene and sustainability, are key drivers. Additionally, the presence of advanced infrastructure, high disposable income, and early adoption of smart technologies are accelerating market expansion. The growing trend of eco-friendly workplaces and the reduction of single-use plastics further supports demand for sustainable dispenser solutions.

Europe

Europe accounts for approximately 25% of the global market, led by countries such as Germany, the UK, and France. The region’s growth is primarily driven by stringent environmental regulations and a strong emphasis on sustainability. Increasing adoption of energy-efficient and bottle-less dispensers is supported by government policies aimed at reducing plastic waste and carbon emissions. Additionally, rising demand from offices and public institutions, coupled with high consumer awareness regarding water quality, is fueling market expansion. The growing popularity of compact and design-oriented dispensers in urban households is also contributing to regional growth.

Asia-Pacific

Asia-Pacific represents approximately 28% of the global market and is the fastest-growing region with a CAGR of around 8.5%. China and India are the primary growth engines, driven by rapid urbanization, population growth, and increasing concerns over water contamination. Government initiatives to improve access to clean drinking water, along with rising middle-class incomes, are significantly boosting demand. Additionally, expanding commercial infrastructure, including offices, retail spaces, and healthcare facilities, is driving large-scale adoption. The region also benefits from strong manufacturing capabilities, enabling cost-effective production and export of water dispensers globally.

Latin America

Latin America is experiencing steady growth, with Brazil and Mexico leading regional demand. The market is driven by increasing awareness of water safety, improving economic conditions, and the gradual expansion of commercial infrastructure. Urbanization and the rising adoption of modern appliances are also contributing to market growth. Additionally, growing investments in water purification infrastructure and public health initiatives are supporting the adoption of water dispensers across residential and institutional segments.

Middle East & Africa

The Middle East and Africa region is witnessing increasing demand due to water scarcity, extreme climatic conditions, and high dependence on purified drinking water. Countries such as the UAE and Saudi Arabia are key markets, driven by strong infrastructure development, high disposable incomes, and significant investments in commercial and hospitality sectors. The demand for advanced filtration systems is particularly high in this region due to limited natural freshwater resources. In Africa, improving access to clean drinking water and rising urbanization are gradually driving market growth, supported by government and international initiatives focused on water security.

Key Players in the Water Dispenser Market

- Primo Water Corporation

- Culligan International

- Waterlogic Holdings

- Blue Star Limited

- Honeywell International

- Oasis International

- Clover Co. Ltd.

- Midea Group

- Haier Group

- Whirlpool Corporation

- Panasonic Corporation

- LG Electronics

- Voltas Limited

- Avalon Water Coolers

- Cosmetal S.r.l.