Virtual Mirrors Market Size

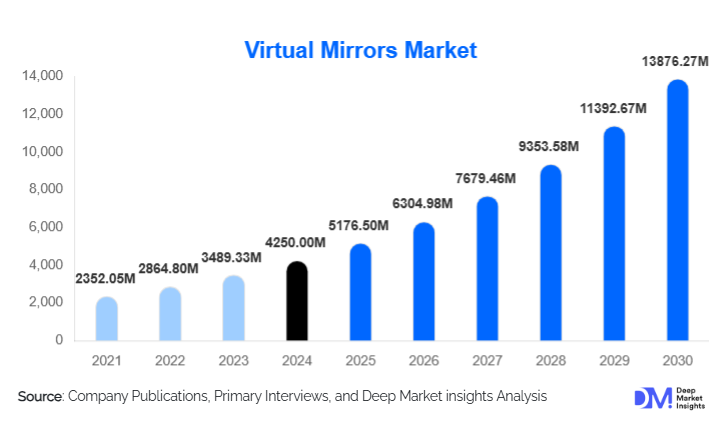

According to Deep Market Insights, the global virtual mirrors market size was valued at USD 4,250 million in 2025 and is projected to grow from USD 5,176.50 million in 2026 to reach USD 13,876.27 million by 2031, expanding at a CAGR of 21.8% during the forecast period (2026–2031). The virtual mirrors market growth is primarily driven by rapid digital transformation across the retail and fashion industries, increasing adoption of augmented reality (AR) and artificial intelligence (AI), and growing consumer preference for contactless and personalized shopping experiences across online and physical stores.

Key Market Insights

- Virtual mirrors are becoming a core component of omnichannel retail strategies, enabling seamless online-to-offline shopping journeys and reducing product return rates.

- Retail and fashion dominate market demand, accounting for more than half of global installations due to high consumer interaction volumes.

- Cloud-based deployment models lead adoption, offering scalability, faster implementation, and lower upfront investment for retailers.

- North America leads global market share, supported by early technology adoption and strong retail digitization.

- Asia-Pacific is the fastest-growing region, driven by e-commerce expansion, mobile-first consumers, and increasing investments in smart retail.

- Advancements in AI, computer vision, and 3D rendering are improving accuracy and driving wider consumer acceptance.

Virtual Mirrors Market Trends

AI-Powered Personalization and Styling Recommendations

Virtual mirrors are increasingly integrated with AI-driven recommendation engines that analyze body dimensions, facial features, skin tone, and browsing behavior to deliver personalized styling suggestions. Retailers are using these capabilities to increase conversion rates, cross-sell complementary products, and enhance customer engagement. Real-time personalization is becoming a differentiating factor, particularly in fashion, beauty, and eyewear segments, where consumers expect tailored experiences comparable to in-store assistance.

Expansion Beyond Fashion Retail

While apparel remains the dominant application, virtual mirrors are expanding into automotive showrooms, fitness studios, healthcare rehabilitation, and smart homes. Automotive brands are deploying virtual mirrors for vehicle configuration and customization, while fitness and wellness providers are using them for posture analysis and training feedback. This diversification is reducing reliance on fashion cycles and broadening the long-term addressable market.

Virtual Mirrors Market Drivers

Growing Demand for Contactless and Digital Shopping Experiences

Consumers increasingly prefer frictionless, contactless shopping solutions. Virtual mirrors enable product trials without physical interaction, aligning with hygiene-conscious and convenience-driven purchasing behavior. This has accelerated adoption across global retail chains and shopping malls.

Reduction in Product Returns and Inventory Optimization

Retailers adopting virtual mirrors report return rate reductions of 20–30%, particularly in apparel and footwear. Improved size and fit visualization lowers logistics costs and enhances sustainability, making virtual mirrors a strategic investment rather than a novelty technology.

Virtual Mirrors Market Restraints

High Initial Implementation Costs

Smart mirror hardware, advanced sensors, and custom software integration require significant upfront investment. Small and mid-sized retailers often face budget constraints, slowing penetration in price-sensitive markets.

Data Privacy and Regulatory Concerns

The use of facial and body data raises privacy challenges, especially under regulations such as GDPR. Ensuring secure data handling and regulatory compliance increases operational complexity for solution providers.

Virtual Mirrors Market Opportunities

Emerging Market Retail Digitization

Rapid retail digitization in Asia-Pacific, Latin America, and the Middle East presents significant growth opportunities. Governments and private retailers are investing in smart retail infrastructure, enabling large-scale deployment of virtual mirrors in emerging economies.

Integration with Smart Homes and Hospitality

Virtual mirrors are increasingly being integrated into smart homes and luxury hotels, offering features such as wardrobe planning, virtual concierge services, and wellness tracking. These applications open premium revenue streams beyond traditional retail.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4250 Million |

| Market Size in 2026 | USD 5176.50 Million |

| Market Size in 2031 | USD 13876.27 Million |

| CAGR | 21.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Technology Type Insights

Augmented reality (AR)-based virtual mirrors dominate the global virtual mirrors market, accounting for approximately 48% of the total market size in 2025. The leadership of this segment is driven by AR’s ability to deliver real-time product visualization with relatively lower computational complexity compared to full mixed-reality systems. AR-based solutions allow consumers to instantly try apparel, cosmetics, eyewear, or accessories using live camera feeds, significantly enhancing engagement while maintaining fast processing speeds and cost efficiency for retailers.

Retailers prefer AR-based virtual mirrors because they integrate seamlessly with existing digital infrastructure, require minimal hardware upgrades, and provide immediate ROI through reduced return rates and higher conversion ratios. The maturity of AR software development kits and increasing compatibility with mobile devices and in-store displays further strengthen this segment’s dominance.

Component Insights

Software constitutes the largest component of the virtual mirrors market, accounting for approximately 42% of the global market share in 2025. The dominance of software is driven by recurring revenue models, including subscription-based licensing, cloud services, AI upgrades, and analytics dashboards. Retailers continuously invest in software enhancements to improve visualization accuracy, personalization algorithms, and omnichannel integration, making software the primary value-generating layer of the ecosystem.

Hardware demand remains stable, supported by the installation of smart mirrors, high-resolution displays, depth cameras, and sensors in physical retail environments. While hardware represents a significant upfront investment, cost optimization and modular hardware designs are helping retailers scale deployments more efficiently. Services, including system integration, customization, maintenance, and post-deployment upgrades, are gaining importance as adoption expands globally. As enterprise-scale rollouts increase, retailers increasingly rely on service providers to ensure system reliability, regulatory compliance, and long-term performance optimization, making services a critical supporting component of market growth.

Deployment Mode Insights

Cloud-based virtual mirrors dominate deployment models, accounting for nearly 60% of total deployments in 2025. The leadership of cloud-based solutions is driven by scalability, faster software updates, centralized data management, and lower capital expenditure requirements. Cloud deployment allows retailers to roll out virtual mirror solutions across multiple locations simultaneously while continuously improving performance through AI model updates and analytics.

Cloud-based platforms also support omnichannel retail strategies by enabling consistent customer experiences across online, mobile, and in-store touchpoints. Retailers benefit from real-time insights into customer behavior, inventory performance, and conversion metrics, reinforcing the preference for cloud-based architectures. On-premise deployment remains relevant for luxury retailers, automotive showrooms, and enterprises with strict data sovereignty or privacy requirements. These solutions are often chosen in regions with stringent data regulations or where retailers require full control over consumer biometric data, particularly in high-end or regulated environments.

End-Use Industry Insights

Retail and fashion remain the largest end-use segment, accounting for approximately 55% of the global virtual mirrors market in 2025. High footfall, frequent product trials, and the need to reduce fitting room congestion and product returns make this segment the primary driver of adoption. Apparel, footwear, and accessories brands leverage virtual mirrors to enhance customer engagement and optimize inventory utilization.

Beauty and cosmetics represent the fastest-growing end-use segment, expanding at a CAGR exceeding 26%. Growth is fueled by rising demand for hygienic, contactless product trials and the increasing influence of social media-driven beauty trends. Virtual mirrors enable real-time makeup simulation and personalized skincare recommendations, driving strong adoption among global beauty brands. Automotive, fitness, and healthcare are emerging as high-potential segments. Automotive showrooms use virtual mirrors for vehicle configuration and customization, while fitness and healthcare applications focus on posture analysis, rehabilitation, and training feedback, expanding the market beyond traditional retail use cases.

Explore more data points, trends and opportunities Download Free Sample Report

Virtual Mirrors Market Segmentations

By Technology Type

- Augmented Reality (AR)-Based Virtual Mirrors

- Artificial Intelligence (AI)-Enabled Virtual Mirrors

- Computer Vision-Based Virtual Mirrors

- Mixed Reality (MR)-Integrated Virtual Mirrors

By Component

- Hardware

- Software

- Services

By Deployment Mode

- Cloud-Based Virtual Mirrors

- On-Premise Virtual Mirrors

By End-Use Industry

- Retail & Fashion

- Beauty & Cosmetics

- Eyewear & Jewelry

- Automotive Showrooms

- Fitness & Wellness

- Healthcare & Rehabilitation

- Hospitality & Smart Homes

By Application

- Virtual Try-On

- Product Visualization

- Personalized Styling Recommendations

- Interactive Advertising & Digital Signage

- Training & Simulation

Regional Insights

North America

North America accounts for approximately 38% of the global virtual mirrors market in 2025, led by the United States. Regional dominance is driven by early adoption of AR and AI technologies, high consumer spending on experiential retail, and strong omnichannel retail penetration. Major retailers actively invest in digital transformation initiatives to enhance in-store experiences and reduce operational inefficiencies. Additionally, strong venture capital funding and the presence of leading technology providers accelerate innovation and large-scale deployment across the region.

Europe

Europe holds around 27% of the global market share, with strong demand from the UK, Germany, and France. Growth is driven by sustainability-focused retail strategies, increasing emphasis on reducing fashion returns, and widespread adoption of omnichannel models. European retailers prioritize virtual mirrors as tools for minimizing waste and improving inventory efficiency, aligning with regional sustainability regulations and consumer preferences for ethical consumption.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at a CAGR of over 25%. Growth is fueled by rapid e-commerce expansion, mobile-first consumer behavior, and increasing investments in smart retail infrastructure across China, Japan, South Korea, and India. Government-led digitalization initiatives, rising middle-class incomes, and aggressive expansion by global and regional retail brands further support large-scale adoption of virtual mirrors in both online and offline retail formats.

Latin America

Latin America represents an emerging growth market, with Brazil and Mexico leading adoption. Growth is supported by rising internet penetration, expanding organized retail formats, and increasing interest from global fashion and beauty brands entering the region. Retailers are adopting virtual mirrors to differentiate customer experiences and improve conversion rates amid growing competition in urban retail hubs.

Middle East & Africa

The Middle East, particularly the UAE and Saudi Arabia, is witnessing increasing adoption of virtual mirrors in the luxury retail and hospitality sectors. High disposable income levels, strong demand for premium shopping experiences, and smart city initiatives are key growth drivers. Africa remains a nascent market; however, expanding modern retail infrastructure and gradual digital transformation in key economies are expected to support long-term growth opportunities.