Vehicle Telematics Market Size

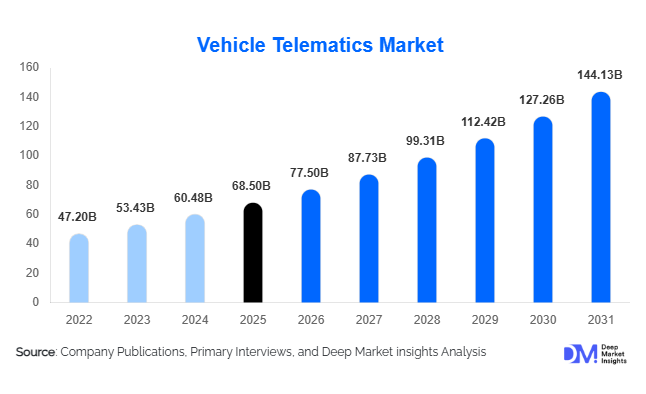

According to Deep Market Insights, the global vehicle telematics market size was valued at USD 68.5 billion in 2025 and is projected to grow from USD 77.5 billion in 2026 to reach USD 144.13 billion by 2031, expanding at a CAGR of 13.2% during the forecast period (2026–2031). The vehicle telematics market growth is primarily driven by the increasing adoption of connected vehicles, rising demand for fleet optimization, and the integration of advanced technologies such as AI, IoT, and 5G connectivity. The rapid expansion of e-commerce and logistics sectors, coupled with regulatory mandates for vehicle safety and tracking, is further accelerating global telematics deployment.

Key Market Insights

- Fleet management remains the dominant application, driven by logistics expansion and the need for operational efficiency.

- Embedded telematics systems are increasingly becoming standard in new vehicles due to OEM integration and regulatory requirements.

- North America dominates the market, supported by advanced infrastructure and high connected vehicle penetration.

- Asia-Pacific is the fastest-growing region, fueled by China and India’s expanding automotive and logistics sectors.

- Cloud-based telematics platforms are gaining traction, offering scalability and real-time analytics capabilities.

- AI and predictive analytics integration is transforming telematics into a proactive decision-making tool.

What are the latest trends in the vehicle telematics market?

AI-Driven Predictive Telematics Solutions

The integration of artificial intelligence and machine learning into telematics platforms is revolutionizing vehicle data analytics. Predictive maintenance, driver behavior analysis, and real-time route optimization are becoming standard features. These capabilities allow fleet operators to minimize downtime, reduce operational costs, and improve safety outcomes. AI-enabled telematics platforms are increasingly being adopted across logistics, construction, and public transport sectors, enhancing overall efficiency and productivity.

5G-Enabled Connected Vehicle Ecosystems

The rollout of 5G technology is enabling faster and more reliable communication between vehicles and infrastructure. This advancement supports real-time data processing, enhanced navigation, and autonomous driving capabilities. Telematics systems powered by 5G are facilitating seamless connectivity, improving vehicle-to-everything (V2X) communication, and enabling advanced safety features. This trend is expected to significantly enhance the performance and scalability of telematics solutions in the coming years.

What are the key drivers in the vehicle telematics market?

Growing Demand for Fleet Optimization

The expansion of global logistics and e-commerce industries is driving the demand for efficient fleet management solutions. Telematics systems enable real-time tracking, route optimization, and fuel management, resulting in cost savings and improved operational efficiency. Businesses are increasingly adopting telematics to gain competitive advantages in supply chain management.

Rising Adoption of Connected Vehicles

The increasing penetration of connected vehicles is a major growth driver for the telematics market. Automotive manufacturers are integrating telematics systems into vehicles to enhance safety, navigation, and infotainment features. This trend is supported by advancements in IoT and wireless communication technologies, enabling seamless data exchange between vehicles and external systems.

What are the restraints for the global market?

Data Privacy and Cybersecurity Concerns

Telematics systems collect sensitive data, including location and driver behavior, making them vulnerable to cyber threats. Ensuring data security and compliance with privacy regulations is a major challenge for market participants, potentially hindering adoption.

High Implementation Costs

The initial cost of telematics hardware, software integration, and maintenance can be significant, particularly for small and medium-sized enterprises. This cost barrier limits adoption in price-sensitive markets, despite long-term benefits.

What are the key opportunities in the vehicle telematics industry?

Expansion of Usage-Based Insurance (UBI)

Telematics is enabling insurance companies to offer personalized policies based on driver behavior. This shift toward usage-based insurance is improving risk assessment and creating new revenue opportunities for insurers and telematics providers.

Growth of Electric and Autonomous Vehicles

The increasing adoption of electric and autonomous vehicles is creating new opportunities for telematics solutions. These systems are essential for monitoring battery performance, enabling remote diagnostics, and supporting autonomous functionalities.

Offering Insights

Hardware dominates the vehicle telematics market, accounting for approximately 42% of the global share in 2025. This leadership is primarily driven by regulatory mandates and OEM-level integration of telematics control units (TCUs), GPS tracking devices, and advanced sensor systems across both passenger and commercial vehicles. Governments across regions are mandating vehicle tracking and safety systems, directly accelerating hardware deployment. Additionally, the rise in connected vehicle production and aftermarket installations in emerging economies further strengthens hardware demand. Meanwhile, software solutions are witnessing rapid growth, particularly in areas such as fleet analytics, AI-driven insights, and real-time monitoring platforms. Services, including integration, consulting, and maintenance, are also gaining traction as telematics ecosystems become increasingly complex and require continuous optimization and support.

Connectivity Type Insights

Embedded telematics leads the market with around 55% share, driven by the growing trend of automotive OEMs integrating telematics systems directly into vehicles during the manufacturing process. This segment is benefiting from increasing demand for seamless connectivity, enhanced vehicle safety features, and compliance with global regulations such as eCall and AIS-140. Embedded systems provide higher reliability, better data accuracy, and improved cybersecurity compared to tethered or smartphone-based alternatives. In contrast, tethered and smartphone-based solutions are gradually losing market share due to their dependence on external devices, limited scalability, and inconsistent performance, particularly in commercial fleet operations.

Vehicle Type Insights

Passenger vehicles account for the largest share of the market at approximately 48%, driven by rising consumer demand for connected car features such as infotainment, navigation, real-time diagnostics, and advanced driver assistance systems (ADAS). Increasing disposable income, urbanization, and consumer preference for enhanced in-vehicle experiences are key drivers supporting this segment’s dominance. However, commercial vehicles, especially heavy-duty trucks, are emerging as the fastest-growing segment due to the rising need for fleet optimization, regulatory compliance, and cost reduction in logistics and transportation operations. The expansion of e-commerce and last-mile delivery services is further accelerating telematics adoption in commercial fleets.

Application Insights

Fleet management remains the leading application segment, holding around 30% of the market share. This dominance is driven by the growing need for route optimization, fuel efficiency, driver behavior monitoring, and asset tracking in logistics and transportation industries. The surge in global trade and e-commerce has significantly increased the demand for efficient fleet operations, making telematics an essential tool for businesses. Additionally, applications such as usage-based insurance (UBI) and predictive maintenance are gaining momentum, supported by advancements in data analytics and increasing adoption by insurance providers and fleet operators seeking to reduce operational risks and costs.

Deployment Mode Insights

Cloud-based deployment dominates the market with approximately 60% share, driven by its scalability, cost-effectiveness, and ability to provide real-time data access and analytics. Organizations are increasingly shifting toward cloud platforms to leverage centralized data management, seamless integration with other enterprise systems, and reduced infrastructure costs. The growing adoption of Software-as-a-Service (SaaS) models in telematics is further accelerating this trend. On-premises solutions, while still relevant in highly regulated industries, are gradually declining as businesses prioritize flexibility, remote accessibility, and faster deployment cycles offered by cloud-based systems.

End-Use Industry Insights

Transportation and logistics is the largest end-use industry, accounting for around 35% of the market. The rapid growth of e-commerce, global trade, and last-mile delivery services is significantly driving telematics adoption in this sector. Companies are leveraging telematics to enhance supply chain visibility, reduce delivery times, and optimize operational efficiency. The insurance sector is also emerging as a key contributor, driven by the adoption of usage-based insurance models that rely on telematics data for risk assessment and premium pricing. Additionally, automotive OEMs are integrating telematics solutions to differentiate their offerings and enhance customer experience, while sectors such as construction, mining, and public transportation are increasingly adopting telematics for asset tracking and operational monitoring.

| By Offering | By Connectivity Type | By Vehicle Type | By Application | By End-Use Industry |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds the largest share of the vehicle telematics market at approximately 35% in 2025, with the United States leading regional demand. Growth in this region is driven by advanced technological infrastructure, high penetration of connected vehicles, and strong presence of leading telematics solution providers. The widespread adoption of fleet management solutions across logistics, transportation, and construction industries further supports market expansion. Additionally, favorable regulatory frameworks, increasing focus on driver safety, and early adoption of AI and IoT technologies are key drivers accelerating telematics deployment in the region. Canada is also witnessing steady growth, supported by rising demand for fleet optimization and cross-border logistics efficiency.

Europe

Europe accounts for around 28% of the global market, with major contributions from Germany, the UK, and France. The region’s growth is primarily driven by stringent regulatory mandates such as the eCall system, which requires telematics integration in all new vehicles for emergency response. Strong automotive manufacturing capabilities, coupled with increasing investments in connected and autonomous vehicle technologies, are further boosting market growth. Additionally, Europe’s focus on sustainability, emission reduction, and smart mobility initiatives is encouraging the adoption of telematics solutions for efficient fleet and traffic management.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 15%, driven by rapid urbanization, expanding automotive production, and increasing government initiatives promoting connected mobility. China dominates the regional market due to its large-scale vehicle manufacturing and strong investments in smart transportation infrastructure. India is emerging as a high-growth market, supported by regulatory mandates such as AIS-140, growth in logistics and e-commerce sectors, and increasing adoption of fleet tracking solutions. Japan and South Korea are also contributing significantly through technological advancements and early adoption of connected vehicle technologies.

Latin America

Latin America is experiencing steady growth, with Brazil and Mexico leading adoption. The region’s growth is driven by increasing demand for fleet management solutions in logistics, mining, and transportation industries. Rising fuel costs and the need for operational efficiency are encouraging businesses to adopt telematics systems. Additionally, improving digital infrastructure and growing awareness about vehicle safety and tracking are supporting market expansion across the region.

Middle East & Africa

The Middle East and Africa region is witnessing moderate growth, particularly in countries such as the UAE and Saudi Arabia. Growth in this region is driven by increasing investments in smart city projects, expanding logistics networks, and rising adoption of telematics for fleet and asset management. Government initiatives aimed at improving transportation efficiency and safety, along with growing construction and oil & gas activities, are further supporting telematics adoption. In Africa, gradual improvements in infrastructure and increasing demand for vehicle tracking in logistics and security applications are contributing to market growth.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Vehicle Telematics Market

- Verizon Communications

- AT&T Inc.

- Robert Bosch GmbH

- Continental AG

- Geotab Inc.

- Trimble Inc.

- TomTom NV

- Harman International

- Valeo SA

- LG Electronics

- Samsung Electronics

- Teletrac Navman

- Mix Telematics

- Octo Telematics

- Sierra Wireless