Vacuum Cleaner Market Size

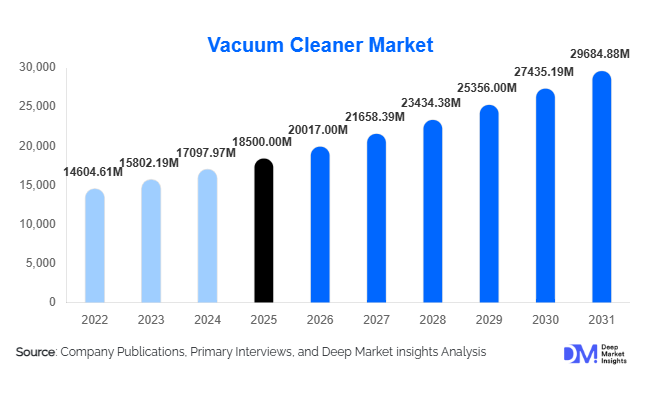

According to Deep Market Insights, the global vacuum cleaner market size was valued at USD 18,500 million in 2025 and is projected to grow from USD 20,017.00 million in 2026 to reach USD 29,684.88 million by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). The vacuum cleaner market growth is primarily driven by increasing urbanization, rising awareness of hygiene and indoor air quality, and rapid technological advancements such as smart and robotic cleaning solutions. The growing penetration of cordless and automated appliances across residential and commercial sectors is further accelerating market expansion globally.

Key Market Insights

- Robotic and smart vacuum cleaners are gaining rapid traction, driven by increasing adoption of smart home ecosystems and automation technologies.

- Asia-Pacific dominates the global market, supported by strong manufacturing capabilities and rising household adoption in China and India.

- Residential applications account for the largest share, driven by growing urban households and demand for convenience-driven appliances.

- Online distribution channels are expanding rapidly, supported by e-commerce penetration and competitive pricing strategies.

- Demand for cordless and lightweight devices is increasing, particularly among urban consumers seeking portability and ease of use.

- Technological innovations such as AI navigation and HEPA filtration are enhancing product differentiation and consumer preference.

What are the latest trends in the vacuum cleaner market?

Rise of Smart and Robotic Cleaning Solutions

The adoption of robotic vacuum cleaners is transforming the market landscape. These devices leverage artificial intelligence, machine learning, and IoT connectivity to deliver automated cleaning with minimal human intervention. Features such as room mapping, obstacle detection, and app-based controls are becoming standard. Integration with voice assistants and smart home ecosystems is further enhancing user convenience. This trend is particularly strong in developed markets such as North America and Europe, but is rapidly gaining momentum in the Asia-Pacific due to falling prices and increasing awareness.

Shift Toward Cordless and Energy-Efficient Devices

Consumers are increasingly favoring cordless vacuum cleaners due to their portability, ease of use, and compact design. Advancements in battery technology have improved runtime and suction power, making cordless models viable alternatives to traditional corded systems. Additionally, energy efficiency and eco-friendly designs are becoming key considerations, particularly in Europe, where regulatory standards are stringent. Manufacturers are focusing on lightweight materials, recyclable components, and low-noise operation to meet evolving consumer expectations.

What are the key drivers in the vacuum cleaner market?

Growing Demand for Smart Home Appliances

The increasing adoption of smart home technologies is a major driver of the vacuum cleaner market. Consumers are seeking integrated solutions that offer automation and remote control capabilities. Robotic vacuum cleaners, in particular, are benefiting from this trend, as they align with the broader shift toward connected living environments. The ability to schedule cleaning tasks and monitor performance through mobile applications is driving widespread adoption.

Rising Awareness of Hygiene and Indoor Air Quality

Heightened awareness of cleanliness and health has significantly boosted demand for vacuum cleaners. Consumers are increasingly investing in appliances equipped with advanced filtration systems, such as HEPA filters, which effectively remove allergens and fine dust particles. This trend is particularly prominent in urban areas with high pollution levels, where maintaining indoor air quality is a priority.

What are the restraints for the global market?

High Cost of Advanced Vacuum Cleaners

Premium vacuum cleaners, particularly robotic and high-end cordless models, are relatively expensive. This limits their adoption in price-sensitive markets, especially in developing regions. While prices are gradually declining due to technological advancements and increased competition, affordability remains a key barrier to widespread penetration.

Maintenance and Battery Limitations

Maintenance requirements and battery-related issues pose challenges for consumers. Cordless and robotic vacuum cleaners often require periodic battery replacement, and limited runtime can affect usability. Additionally, repair and servicing costs can deter potential buyers, particularly in emerging markets where after-sales infrastructure may be limited.

What are the key opportunities in the vacuum cleaner industry?

Expansion in Emerging Markets

Emerging economies such as India, China, and Southeast Asia present significant growth opportunities. Rising disposable incomes, rapid urbanization, and increasing awareness of modern home appliances are driving demand. Companies can capitalize on this opportunity by offering affordable and localized product variants tailored to regional preferences.

Growth in Commercial and Industrial Applications

The expansion of sectors such as healthcare, hospitality, and retail is creating demand for advanced cleaning solutions. Commercial establishments require high-performance vacuum cleaners to maintain hygiene standards, particularly in post-pandemic environments. Industrial applications are also growing, with demand for heavy-duty and wet & dry vacuum systems in manufacturing and logistics facilities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18500 Million |

| Market Size in 2026 | USD 20017 Million |

| Market Size in 2031 | USD 29684.88 Million |

| CAGR | 8.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Robotic vacuum cleaners have emerged as the leading product segment, accounting for approximately 28% of the global market in 2025, driven primarily by the rapid adoption of smart home ecosystems and increasing consumer preference for automation. The integration of advanced technologies such as artificial intelligence (AI), LiDAR-based navigation, and IoT connectivity has significantly enhanced product efficiency, enabling features such as real-time mapping, obstacle detection, and app-based scheduling. This segment is further propelled by rising demand in developed markets and growing affordability in emerging economies.

Stick and cordless vacuum cleaners are the fastest-growing sub-segments, supported by improvements in lithium-ion battery technology, which have enhanced runtime and suction capabilities. Their lightweight, compact design and ease of storage make them highly suitable for urban households, particularly in apartments and smaller living spaces. Meanwhile, traditional upright and canister vacuum cleaners continue to maintain stable demand, especially in commercial and industrial environments where high suction power, durability, and continuous operation are critical. These segments are also benefiting from upgrades in motor efficiency and filtration technologies, ensuring their continued relevance in professional applications.

Application Insights

The residential segment dominates the vacuum cleaner market, contributing nearly 65% of total demand in 2025. This dominance is driven by increasing urbanization, rising disposable incomes, and the growing penetration of household appliances across developing economies. The shift toward dual-income households and busy lifestyles has further accelerated demand for convenient cleaning solutions, particularly robotic and cordless vacuum cleaners. Additionally, heightened awareness of indoor air quality and allergen control is encouraging the adoption of advanced filtration systems in residential settings.

Commercial applications represent the fastest-growing segment, fueled by stringent hygiene standards across industries such as hospitality, healthcare, and corporate offices. Post-pandemic sanitation protocols have led to increased investments in high-performance cleaning equipment, particularly in hospitals and hotels. Industrial applications, although smaller in share, are witnessing steady growth due to the expansion of the manufacturing and logistics sectors. Demand in this segment is driven by the need for specialized cleaning solutions capable of handling heavy debris, hazardous materials, and large-scale operations, particularly in industries such as automotive, food processing, and pharmaceuticals.

Distribution Channel Insights

Online distribution channels are rapidly gaining prominence, accounting for approximately 35% of global sales, and are expected to expand further due to increasing digital penetration and consumer preference for convenient purchasing options. E-commerce platforms provide access to a wide range of products, competitive pricing, customer reviews, and doorstep delivery, making them highly attractive to modern consumers. The growth of direct-to-consumer (D2C) strategies by manufacturers has also strengthened online sales, enabling brands to enhance customer engagement and control pricing strategies.

Offline channels, including hypermarkets, supermarkets, and specialty stores, continue to play a crucial role, particularly in emerging markets where consumers prefer physical product demonstrations before purchase. These channels are also important for high-value products, where in-store assistance and after-sales support influence buying decisions. Additionally, direct sales and exclusive brand outlets are expanding globally, allowing manufacturers to build stronger brand presence and offer personalized customer experiences. The coexistence of online and offline channels is creating an omnichannel retail environment that enhances market reach and customer accessibility.

End-User Insights

Households remain the primary end users of vacuum cleaners, driven by increasing awareness of cleanliness, convenience, and health-related benefits. The rising adoption of smart and automated cleaning solutions is further strengthening demand in this segment. The commercial sector, including hospitality, healthcare, and retail, is experiencing rapid growth due to heightened sanitation requirements and regulatory compliance. Hospitals and healthcare facilities, in particular, are investing in advanced vacuum systems equipped with HEPA filters to maintain sterile environments.

Industrial end users are increasingly adopting specialized vacuum cleaners to improve operational efficiency and workplace safety. These systems are designed to handle heavy-duty cleaning tasks, including dust extraction, hazardous waste removal, and large-scale debris management. Emerging applications in industries such as pharmaceuticals, electronics manufacturing, and food processing are expanding the scope of vacuum cleaner usage, driven by the need for contamination control and compliance with stringent quality standards.

Explore more data points, trends and opportunities Download Free Sample Report

Vacuum Cleaner Market Segmentations

By Product Type

- Upright Vacuum Cleaners

- Canister Vacuum Cleaners

- Stick Vacuum Cleaners

- Handheld Vacuum Cleaners

- Robotic Vacuum Cleaners

- Central Vacuum Systems

By Application

- Residential

- Commercial

- Industrial

By Distribution Channel

- Online Retail

- Hypermarkets & Supermarkets

- Specialty Stores

- Direct Sales / Brand Stores

Regional Insights

North America

North America accounts for approximately 25% of the global vacuum cleaner market, with the United States representing the largest share. The region’s growth is primarily driven by high disposable incomes, strong consumer awareness, and early adoption of smart home technologies. The widespread use of robotic and premium vacuum cleaners is supported by a well-established e-commerce infrastructure and a high penetration of connected devices. Additionally, increasing demand for energy-efficient and high-performance appliances, along with growing concerns about indoor air quality, is driving innovation and replacement demand in the region.

Europe

Europe holds around 22% of the global market share, with key contributions from Germany, the United Kingdom, and France. Growth in this region is strongly influenced by stringent environmental regulations related to energy efficiency, noise levels, and sustainability. Consumers in Europe demonstrate a strong preference for eco-friendly and technologically advanced products, driving demand for energy-efficient vacuum cleaners with advanced filtration systems. The region is also witnessing increased adoption of robotic vacuum cleaners, supported by high living standards and a growing emphasis on smart home integration.

Asia-Pacific

Asia-Pacific dominates the global market with a share of approximately 38% in 2025, making it the largest and fastest-growing region. China is the leading contributor, accounting for nearly 18% of global demand, driven by strong manufacturing capabilities, large-scale domestic consumption, and export dominance. India and Southeast Asia are emerging as high-growth markets due to rapid urbanization, rising middle-class populations, and increasing awareness of modern home appliances. Government initiatives promoting domestic manufacturing and smart city development are further supporting market growth. The region’s expansion is also fueled by the availability of cost-effective products and the increasing penetration of e-commerce platforms.

Latin America

Latin America contributes approximately 8% of the global market, with Brazil and Mexico leading demand. Growth in this region is driven by urbanization, improving living standards, and increasing adoption of household appliances. However, price sensitivity remains a key challenge, influencing demand for mid-range and economy products. The expansion of retail infrastructure and rising internet penetration are supporting the growth of online sales channels. Additionally, increasing awareness of hygiene and cleanliness is gradually driving market penetration across urban centers.

Middle East & Africa

The Middle East & Africa region accounts for around 7% of the global market, with significant demand from countries such as the UAE, Saudi Arabia, and South Africa. Growth in this region is driven by expanding hospitality and tourism sectors, particularly in the Gulf countries, where high standards of cleanliness are essential. Infrastructure development, rising urbanization, and increasing disposable incomes are also contributing to market expansion. In Africa, gradual economic development and improving access to modern appliances are supporting growth, although affordability and distribution challenges persist. The region presents long-term growth potential as awareness and accessibility continue to improve.

Key Players in the Vacuum Cleaner Market

- Dyson Ltd.

- iRobot Corporation

- Miele Group

- Panasonic Corporation

- LG Electronics

- Samsung Electronics

- Philips N.V.

- Electrolux AB

- SharkNinja Operating LLC

- Bissell Inc.

- Hoover (Techtronic Industries)

- Eureka Forbes Ltd.

- Nilfisk Group

- Kärcher

- Hitachi Appliances