UPF Sun Protective Clothing Market Size

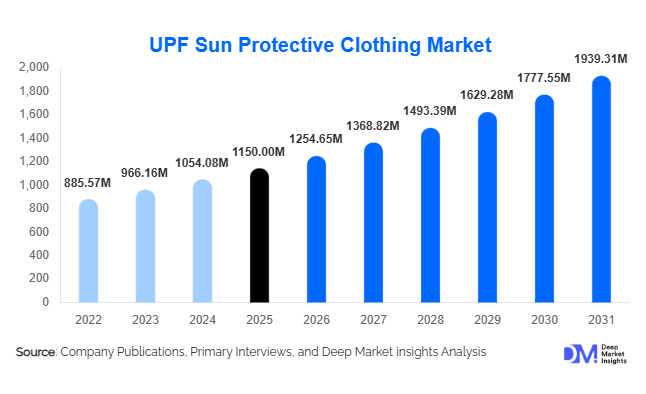

According to Deep Market Insights, the global UPF sun protective clothing market size was valued at USD 1,150 million in 2025 and is projected to grow from USD 1,254.65 million in 2026 to reach USD 1,939.31 million by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). The market growth is primarily driven by increasing awareness of skin cancer prevention, rising participation in outdoor recreational activities, and growing adoption of functional apparel with integrated UV protection.

UPF clothing is transitioning from a niche outdoor segment into a mainstream apparel category as consumers prioritize preventive healthcare and multifunctional clothing. The integration of breathable, lightweight, and sustainable fabrics has significantly enhanced product appeal across demographics. Strong demand in high UV exposure regions such as North America and Australia, along with expanding awareness in the Asia-Pacific, is accelerating market growth. Additionally, the rise of e-commerce and direct-to-consumer brands is improving accessibility and global reach, further supporting the expansion of the UPF sun protective clothing market.

Key Market Insights

- UPF clothing is evolving into everyday lifestyle wear, driven by increasing consumer awareness of UV protection and skin health.

- Sports and outdoor recreation remain the dominant usage segment, accounting for a significant share due to rising fitness and adventure activities globally.

- North America dominates the global market, supported by high awareness levels and strong consumer spending on premium apparel.

- Asia-Pacific is the fastest-growing region, driven by rising disposable incomes and increasing UV exposure awareness.

- Sustainable and recycled fabrics are gaining traction, aligning with global environmental and ethical consumption trends.

- Online retail channels are leading distribution, enabling wider product access and direct brand engagement with consumers.

What are the latest trends in the UPF sun protective clothing market?

Rise of Sustainable and Eco-Friendly UPF Apparel

Sustainability has emerged as a defining trend in the UPF sun protective clothing market. Consumers are increasingly favoring garments made from recycled polyester, organic cotton, and bamboo fibers that offer inherent UV protection. Brands are investing in eco-friendly production processes, reducing chemical treatments while enhancing fabric durability and performance. This trend is particularly strong in Europe and North America, where environmental consciousness is influencing purchasing decisions. Companies are also adopting circular economy models, including recyclable garments and reduced packaging, which strengthens brand positioning and customer loyalty.

Expansion of Athleisure and Everyday Wear Integration

UPF clothing is no longer limited to outdoor or sports use but is increasingly integrated into athleisure and casual fashion. Stylish designs combined with functional UV protection are appealing to urban consumers who seek versatile clothing for daily use. This trend is expanding the addressable market beyond niche outdoor enthusiasts to mainstream consumers. Brands are launching collections that seamlessly blend fashion with performance, making UPF apparel suitable for office wear, travel, and leisure activities.

What are the key drivers in the UPF sun protective clothing market?

Increasing Awareness of Skin Health and UV Protection

The rising incidence of skin cancer and UV-related health issues is a major driver for the market. Health organizations and dermatologists are promoting preventive measures, leading to increased adoption of UPF clothing as a reliable alternative to sunscreen. Consumers are becoming more proactive about long-term skin protection, especially in regions with high UV index levels.

Growth in Outdoor and Fitness Activities

The surge in outdoor lifestyles, including hiking, cycling, water sports, and travel, is significantly boosting demand for UPF apparel. Consumers require performance-oriented clothing that provides comfort, breathability, and protection. This trend has expanded the application of UPF garments across sportswear and recreational segments, driving consistent market growth.

What are the restraints for the global market?

High Cost Compared to Conventional Apparel

UPF clothing often carries a premium price due to advanced fabric technology and certification standards. This limits adoption in price-sensitive markets, particularly in developing economies where affordability remains a key concern. The cost barrier restricts mass-market penetration despite growing awareness.

Lack of Standardized Regulations and Awareness Gaps

Inconsistent labeling standards and varying regulations across regions create confusion among consumers regarding product effectiveness. Limited awareness in emerging markets further slows adoption, as consumers may not fully understand the benefits of UPF-rated clothing.

What are the key opportunities in the UPF sun protective clothing industry?

Expansion in Emerging Markets

Emerging economies such as India, China, and Brazil present significant growth opportunities due to rising disposable incomes and increasing awareness of UV protection. Governments and health organizations are promoting sun safety, creating favorable conditions for market expansion. Affordable product lines tailored to local climates can unlock substantial demand in these regions.

Integration of Smart and Functional Textiles

Technological advancements in smart textiles offer opportunities for innovation. Fabrics with UV sensors, temperature regulation, and moisture management capabilities are gaining attention. These innovations can enhance product differentiation and allow brands to command premium pricing while meeting evolving consumer expectations.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1150 Million |

| Market Size in 2026 | USD 1254.65 Million |

| Market Size in 2031 | USD 1939.31 Million |

| CAGR | 9.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Tops dominate the UPF sun protective clothing market, accounting for approximately 32% of the total market share in 2025, making them the leading product category globally. Their dominance is primarily driven by their versatility across multiple use cases, including casual daily wear, athletic activities, occupational use, and travel applications. UPF shirts, T-shirts, polos, and lightweight hoodies are increasingly preferred by consumers because they offer an ideal combination of sun protection, breathability, and comfort while maintaining style and practicality. The leading growth driver for this segment is the increasing consumer preference for multifunctional apparel that seamlessly transitions between outdoor activity and everyday use. Additionally, manufacturers are continuously innovating with stretchable, moisture-wicking, and odor-resistant fabrics, which further strengthen the appeal of tops. The segment is also benefiting from aggressive product launches by global sportswear brands integrating UPF protection into athleisure collections, making these products more accessible to mainstream consumers. Rising participation in outdoor sports, tourism, and wellness-focused lifestyles is expected to continue supporting the leadership of this segment over the forecast period.

Fabric Type Insights

Synthetic fibers lead the UPF sun protective clothing market with approximately 45% market share in 2025, driven by their superior technical performance compared to natural fibers. Polyester and nylon-based blends dominate this segment due to their inherent UV-blocking capability, excellent durability, moisture management properties, and compatibility with advanced textile engineering processes. The key growth driver for this segment is the increasing demand for high-performance apparel capable of delivering both functional protection and long-term wearability. Synthetic fibers allow manufacturers to incorporate additional performance features such as quick-drying technology, anti-microbial coatings, temperature regulation, and elasticity, making them highly suitable for sports, travel, and occupational applications. Furthermore, advancements in recycled synthetic materials have significantly improved sustainability perceptions, helping brands align with environmentally conscious consumer preferences. The ability of synthetic fabrics to maintain UPF effectiveness even after repeated washing and prolonged use also contributes to their widespread adoption. This segment continues to benefit from innovations in microfiber weaving technologies that enhance UV resistance without compromising fabric softness or comfort.

UPF Rating Insights

Garments with UPF 40–50+ dominate the market, accounting for nearly 50% of global revenue share in 2025. This segment’s leadership is strongly driven by rising consumer awareness regarding maximum sun protection and increasing recommendations from dermatologists and healthcare institutions for high-protection apparel. The leading driver behind this category is the growing incidence of UV-related skin conditions, including skin aging and skin cancer concerns, which has encouraged consumers to prioritize garments offering superior ultraviolet blockage. High-UPF-rated clothing is especially favored in regions with elevated UV exposure levels, such as Australia, North America, and parts of the Asia-Pacific. In addition, institutional buyers, including schools, sports academies, and occupational safety programs, increasingly prefer UPF 50+ certified products to ensure compliance with sun safety standards. The premium positioning of this category also enables brands to achieve higher margins through product differentiation, advanced certification labeling, and performance guarantees. As consumer education around UV protection continues to improve, the demand for the highest-rated protection garments is expected to remain robust.

End-User Insights

Women represent the largest end-user segment in the UPF sun protective clothing market, accounting for approximately 42% of total market share in 2025. This leadership is primarily driven by heightened awareness of skincare, anti-aging concerns, and stronger engagement with wellness-oriented lifestyle products. Female consumers tend to exhibit higher adoption rates for preventive personal care solutions, including sun-protective apparel, particularly in urban and premium retail markets. The leading growth driver for this segment is the growing availability of fashion-forward UPF clothing collections that blend aesthetics with functionality. Brands are increasingly introducing stylish silhouettes, lightweight fabrics, and versatile designs tailored specifically for women, including dresses, leggings, tunics, and activewear. Social media influence, beauty-conscious purchasing behavior, and endorsements by dermatologists have further accelerated product adoption among female consumers. Additionally, women are often primary purchasing decision-makers for family apparel, indirectly influencing demand across children’s and household sun protection purchases. This segment is expected to remain dominant as fashion brands continue integrating UV-protective features into mainstream womenswear collections.

Usage Type Insights

Sports and outdoor recreation remain the leading usage segment, contributing approximately 38% of total market share in 2025. This segment’s dominance is driven by the rapid expansion of outdoor fitness culture, adventure tourism, and recreational sports participation globally. Activities such as hiking, cycling, running, tennis, fishing, beach sports, and water recreation require prolonged sun exposure, making UPF apparel a critical performance and safety solution. The primary driver for this segment is the increasing consumer emphasis on health-conscious outdoor lifestyles, coupled with the demand for specialized apparel that enhances comfort while minimizing UV risks. Performance-focused product innovations such as ergonomic designs, moisture-wicking technologies, and lightweight stretch fabrics have significantly strengthened adoption within this category. Professional athletes, fitness influencers, and sports communities are also playing a key role in promoting UPF clothing as essential athletic gear. The continued growth of outdoor recreational infrastructure and destination tourism worldwide is expected to sustain the leadership of this segment over the coming years.

Distribution Channel Insights

Online retail dominates the distribution landscape with approximately 48% market share in 2025, making it the largest and fastest-evolving channel in the UPF sun protective clothing market. The primary driver of this segment is the increasing digitalization of consumer purchasing behavior and the convenience offered by direct-to-consumer e-commerce platforms. Consumers prefer online channels due to access to broader product assortments, detailed product specifications, customer reviews, transparent pricing comparisons, and promotional discounts. The expansion of specialized brand websites and marketplace platforms has enabled both established and emerging brands to reach geographically dispersed consumer bases without relying heavily on physical retail infrastructure. Additionally, social media marketing, influencer endorsements, and personalized digital advertising are significantly improving product visibility and conversion rates. Subscription-based apparel models and virtual fitting technologies are further enhancing online consumer engagement. As younger digitally native demographics increasingly dominate apparel spending, online retail is expected to remain the strongest growth engine for market expansion.

End-Use Industry Insights

The demand for UPF sun protective clothing is closely linked to the rapid expansion of outdoor recreation, sports, occupational safety, and lifestyle wellness industries. Outdoor recreation and sports remain the largest end-use sectors, growing at over 8% annually, supported by increasing global participation in fitness, hiking, cycling, water sports, and outdoor travel. The occupational segment is emerging as one of the fastest-growing applications, particularly across construction, agriculture, fisheries, mining, and logistics industries, where worker safety regulations increasingly mandate protective apparel for prolonged outdoor exposure. This segment is projected to expand at a CAGR exceeding 10% during the forecast period, driven by employer-led bulk procurement and stricter workplace safety standards.

Children’s apparel represents another promising growth area, supported by rising parental awareness regarding early-life UV exposure risks and school-based sun safety initiatives. Educational institutions, summer camps, and youth sports organizations are increasingly integrating UPF-certified uniforms and recreational wear into their safety programs. Additionally, hospitality, travel, and wellness sectors are beginning to adopt branded sun-protective apparel as part of premium service offerings, further broadening the application scope of the market.

Explore more data points, trends and opportunities Download Free Sample Report

UPF Sun Protective Clothing Market Segmentations

By Product Type

- Tops

- Bottoms

- Outerwear

- Accessories

- Full-body suits/swimwear

By Fabric Type

- Synthetic fibers

- Natural fibers

- Treated fabrics

- Inherent UV-protective fabrics

By End-User

- Men

- Women

- Kids & infants

By Usage Type

- Everyday wear

- Sports & outdoor recreation

- Water sports

- Occupational use

By Distribution Channel

- Online retail

- Specialty stores

- Department stores

- Hypermarkets/supermarkets

Regional Insights

North America

North America holds the largest share of the global UPF sun protective clothing market at approximately 35% in 2025, with the United States accounting for the majority of regional revenue. The primary driver of regional growth is high awareness regarding skin cancer prevention, supported by active public health campaigns from dermatology associations and healthcare institutions. The U.S. experiences strong demand due to its deeply established outdoor recreation culture, high consumer spending on premium activewear, and widespread adoption of functional apparel. Coastal states such as California and Florida are particularly significant demand centers due to year-round sun exposure and beach tourism. Canada contributes meaningfully to market growth through increasing participation in hiking, camping, and outdoor sports, supported by rising consumer preference for performance-based apparel. The region also benefits from strong retail infrastructure, advanced e-commerce penetration, and the presence of leading global brands continuously innovating in UV-protective textiles.

Asia-Pacific

Asia-Pacific accounts for approximately 28% of the global market and is the fastest-growing regional market, projected to expand at a CAGR exceeding 11%. The leading growth driver is the combination of increasing UV exposure awareness, expanding middle-class disposable incomes, and rapid urbanization across major economies. Australia leads in per capita consumption due to some of the world’s highest UV radiation levels and long-standing government-led sun safety campaigns such as “Slip-Slop-Slap.” China is witnessing strong growth driven by rising premium apparel consumption, increased participation in outdoor fitness, and growing consumer preference for technologically advanced textiles. India represents a major emerging opportunity due to intense climatic conditions, expanding awareness of skin protection, and the rapid growth of digital retail channels. Japan contributes through strong demand for high-quality, lightweight, and innovative protective apparel, supported by consumer preference for technologically sophisticated garments. Regional manufacturing strength and cost-efficient textile production also support long-term market expansion.

Europe

Europe contributes approximately 22% of the global market share, with Germany, France, the United Kingdom, Italy, and Spain serving as key contributors. The primary driver of regional growth is the strong consumer preference for sustainable, ethically produced, and multifunctional apparel. European consumers increasingly seek garments that combine UV protection with eco-friendly materials and transparent supply chains. Rising outdoor leisure participation, travel recovery, and increased demand for wellness-oriented lifestyles are further accelerating product adoption. Germany leads due to its highly developed outdoor sports market, while France and Italy benefit from strong resort and travel-related apparel demand. The UK demonstrates steady growth driven by increasing awareness of preventive skin health and growing participation in recreational sports. Stringent environmental regulations and growing support for sustainable textile innovation are expected to further strengthen regional demand over the forecast period.

Latin America

Latin America holds approximately 8% market share, with Brazil and Mexico emerging as the primary regional demand centers. The leading growth driver is the region’s high year-round sun exposure, combined with expanding beach tourism and outdoor leisure activities. Brazil, with its strong coastal tourism economy and outdoor lifestyle culture, represents the largest market within the region. Mexico is witnessing increasing demand due to rising awareness of UV protection and expanding retail penetration of international sportswear brands. However, affordability remains a key market challenge, leading to stronger growth within mid-range product categories. The continued expansion of e-commerce platforms and local manufacturing capabilities is expected to improve product accessibility and support future growth.

Middle East & Africa

The Middle East & Africa region accounts for approximately 7% of the global market share. The primary driver of growth is the region’s harsh climatic conditions, extreme sunlight exposure, and increasing occupational demand for protective apparel. The UAE leads regional demand due to strong premium apparel consumption, rising outdoor tourism, and growing awareness of preventive skin health. Saudi Arabia is emerging as a key growth market driven by economic diversification initiatives, expanding retail infrastructure, and increasing participation in outdoor recreational activities. South Africa contributes significantly due to a growing activewear market and rising consumer awareness of sun safety. Additionally, occupational sectors such as construction, energy, and mining are creating consistent institutional demand for UV-protective clothing across the broader region.

Key Players in the UPF Sun Protective Clothing Market

- Columbia Sportswear Company

- Coolibar Inc.

- Patagonia Inc.

- Nike Inc.

- Adidas AG

- Under Armour Inc.

- The North Face (VF Corporation)

- Decathlon S.A.

- Uniqlo (Fast Retailing Co.)

- REI Co-op

- Mountain Hardwear

- Helly Hansen

- Solbari

- UV Skinz

- Kanu Surf