Under Sink Water Filter System Market Size

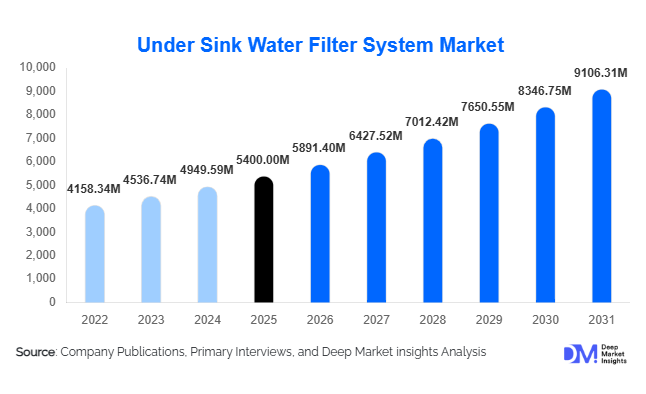

According to Deep Market Insights, the global under-sink water filter system market size was valued at USD 5,400 million in 2025 and is projected to grow from USD 5,891.40 million in 2026 to reach USD 9,106.31 million by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). The under-sink water filter system market growth is primarily driven by rising consumer concerns regarding drinking water contamination, increasing urbanization, and the growing adoption of point-of-use filtration technologies in residential and commercial environments.

Under-sink filtration systems are designed to purify water directly at the source by removing contaminants such as chlorine, heavy metals, sediments, and harmful microorganisms. Unlike countertop or pitcher filters, these systems provide multi-stage purification with higher filtration capacity and longer operational life. As water quality concerns intensify globally due to aging municipal infrastructure, industrial pollution, and microplastic contamination, consumers are increasingly investing in advanced filtration systems installed beneath kitchen sinks.

The market is also benefiting from technological innovations such as reverse osmosis membranes, ultrafiltration modules, and multi-stage filtration cartridges that significantly improve purification efficiency. Additionally, smart filtration systems equipped with sensors and digital monitoring features are gaining popularity among tech-savvy consumers. The increasing shift toward sustainable living and reduced bottled water consumption is further supporting market expansion as households seek long-term water purification solutions that minimize plastic waste.

Key Market Insights

- Reverse osmosis filtration technology dominates the market, accounting for nearly 42% of global system installations due to its superior contaminant removal capability.

- Residential households represent the largest demand segment, contributing approximately 70% of global market revenue.

- North America leads the global market, accounting for about 34% of global demand due to strong consumer awareness regarding water quality.

- Asia-Pacific is the fastest-growing regional market, driven by rapid urbanization and increasing water pollution concerns in China and India.

- Offline retail channels remain the dominant distribution mode, supported by installation services and specialized water treatment retailers.

- Technological integration, including smart monitoring systems, is emerging as a key differentiator among premium filtration products.

What are the latest trends in the under-sink water filter system market?

Smart Water Filtration Systems

The adoption of smart filtration systems is one of the most prominent trends shaping the under-sink water filter system market. Modern filtration units increasingly incorporate digital sensors that monitor water quality, track filtration performance, and notify users when filter cartridges require replacement. These systems often integrate with smartphone applications, allowing consumers to track water consumption and filtration efficiency in real time.

This trend is particularly strong in technologically advanced markets such as the United States, South Korea, and Japan, where smart home ecosystems are rapidly expanding. Manufacturers are also developing connected filtration systems that integrate with home automation platforms, enabling users to monitor water quality alongside other smart household devices. The ability to improve convenience, extend filter life, and ensure consistent water quality is making smart filtration systems highly attractive for premium consumers.

Multi-Stage Hybrid Filtration Systems

Another key trend is the growing adoption of multi-stage hybrid filtration systems that combine multiple purification technologies within a single unit. These systems typically include sediment filtration, activated carbon filtration, reverse osmosis membranes, and UV disinfection stages to remove a wide range of contaminants.

Consumers are increasingly seeking comprehensive water purification solutions rather than basic filtration systems. Hybrid systems offer higher filtration efficiency and improved water taste while removing contaminants such as dissolved solids, heavy metals, bacteria, and chlorine. This trend is particularly significant in urban regions where municipal water sources may contain complex pollutant mixtures.

What are the key drivers in the under-sink water filter system market?

Rising Consumer Awareness of Water Quality

Growing public awareness regarding drinking water contamination is one of the primary drivers of market growth. Increasing reports of pollutants such as lead, pesticides, microplastics, and industrial chemicals in municipal water supplies have heightened consumer concerns globally. Households are increasingly investing in point-of-use filtration systems to ensure the safety and quality of drinking water.

In many developed countries, aging water infrastructure is contributing to contamination risks. Consumers are therefore seeking reliable household purification solutions that provide immediate access to clean drinking water without relying solely on centralized municipal treatment systems.

Expansion of Residential Construction and Urbanization

Rapid urbanization and residential construction growth are also driving demand for under-sink water filtration systems. As urban populations expand, new housing developments are incorporating advanced kitchen appliances and plumbing fixtures. Under-sink filtration systems are increasingly included as standard components in modern kitchen installations.

The construction of apartment complexes, smart homes, and residential communities is creating substantial opportunities for filtration system manufacturers. Builders and real estate developers are increasingly integrating water purification solutions as value-added features in residential properties.

What are the restraints for the global market?

High Initial Installation Costs

Despite their advantages, under-sink water filtration systems remain relatively expensive compared to basic filtration alternatives such as pitcher filters or faucet-mounted units. Advanced reverse osmosis systems often require professional installation and additional plumbing components, increasing upfront costs for consumers.

This cost barrier can limit adoption among price-sensitive consumers, particularly in developing economies where household budgets may be constrained.

Recurring Maintenance and Filter Replacement Costs

Another major challenge in the market is the ongoing cost associated with filter replacement and system maintenance. Filtration cartridges typically require replacement every six to twelve months, depending on water usage and contamination levels.

These recurring expenses can discourage long-term adoption among some consumers and create price sensitivity in competitive markets. Manufacturers are increasingly addressing this challenge by offering subscription-based filter replacement programs to improve customer retention.

What are the key opportunities in the under-sink water filter system industry?

Growth in Emerging Urban Markets

Rapid urbanization across emerging economies such as India, Indonesia, Brazil, and Vietnam presents substantial growth opportunities for filtration system manufacturers. Rising populations, increasing industrial pollution, and inconsistent municipal water treatment infrastructure are encouraging households to invest in point-of-use purification solutions.

Growing middle-class populations and rising disposable incomes are also expanding the consumer base for home filtration appliances. Manufacturers that establish localized production and distribution networks in emerging markets can capture significant long-term demand.

Commercial and Hospitality Sector Expansion

The hospitality and food service industries are increasingly adopting under-sink filtration systems to ensure high water quality for cooking, beverage preparation, and customer consumption. Restaurants, cafés, and hotels require reliable filtration systems to maintain food safety standards and improve beverage taste.

Additionally, many commercial establishments are reducing reliance on bottled water as part of sustainability initiatives aimed at minimizing plastic waste. This shift toward permanent water purification systems is creating strong opportunities for commercial-grade under-sink filtration systems with higher flow rates and filtration capacity.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5400 Million |

| Market Size in 2026 | USD 5891.40 Million |

| Market Size in 2031 | USD 9106.31 Million |

| CAGR | 9.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Filtration Technology Insights

Reverse osmosis filtration systems represent the dominant technology in the under-sink water filter system market, accounting for approximately 42% of global market share in 2025. The segment leads the market due to its superior purification capability and ability to remove a broad range of contaminants, including dissolved solids, heavy metals, bacteria, nitrates, and chemical pollutants. Reverse osmosis systems operate through semi-permeable membranes that effectively eliminate microscopic impurities, making them highly suitable for regions where municipal water quality may vary or where groundwater contamination is prevalent. The increasing demand for comprehensive purification solutions is a key driver supporting the dominance of reverse osmosis systems. Many modern under sink systems now incorporate multi-stage filtration architectures that combine sediment filtration, activated carbon filters, and reverse osmosis membranes to deliver high purification efficiency and improved taste quality. Consumers are increasingly prioritizing long-term water safety and reliability, which has encouraged widespread adoption of multi-stage RO-based systems across both developed and emerging markets.

Activated carbon filtration systems also hold a significant share of the market, particularly in regions where chlorine removal and taste improvement are primary consumer concerns. These systems are commonly used in areas with relatively safe municipal water supplies where consumers primarily seek to enhance water taste and remove organic compounds. Activated carbon filters are also cost-effective and require minimal maintenance, making them attractive for budget-conscious consumers. Ultrafiltration and ultraviolet purification technologies are gaining traction as complementary filtration stages, particularly in hybrid systems designed for urban environments with complex contamination challenges. Ultrafiltration systems are increasingly used in regions where microbial contamination is a concern, while UV purification technologies provide additional disinfection by eliminating bacteria and viruses. The growing popularity of hybrid filtration systems that combine RO, UV, and carbon filtration technologies is expected to further strengthen technological innovation within this segment.

Application Insights

Residential applications dominate the under-sink water filter system market, representing nearly 70% of total global demand in 2025. The leading position of this segment is driven by increasing awareness regarding drinking water quality, rising health consciousness among households, and growing consumer concerns regarding contaminants such as heavy metals, pesticides, and microplastics. As urban households increasingly prioritize safe drinking water, under-sink filtration systems are emerging as a preferred solution due to their high purification capacity and discreet installation beneath kitchen sinks. The residential segment is also benefiting from global trends in home improvement and smart kitchen appliance adoption. Consumers are increasingly investing in integrated kitchen systems that improve convenience and functionality. Under-sink water filtration units provide continuous access to purified water without occupying countertop space, making them particularly suitable for modern urban apartments and compact kitchen environments.

The commercial sector, including restaurants, cafés, hotels, and office buildings, accounts for approximately 22% of market demand. This segment is expanding steadily as businesses prioritize water quality for food preparation, beverage production, and employee consumption. Water filtration systems are especially critical in the food service industry, where purified water improves beverage taste and helps maintain food safety standards. Institutional applications such as hospitals, schools, universities, and government buildings represent an emerging segment as public organizations increasingly prioritize safe drinking water infrastructure. Growing regulatory focus on water safety and sanitation standards is encouraging institutions to adopt permanent water purification systems to ensure consistent water quality for large populations.

Distribution Channel Insights

Offline retail channels continue to dominate the distribution landscape, accounting for nearly 62% of total market sales. Specialty water treatment retailers, home improvement stores, and appliance retailers remain key sales channels due to the installation assistance and technical consultation they provide. Since under-sink filtration systems often require plumbing integration and professional installation, consumers frequently prefer purchasing these products through retailers that offer after-sales support and installation services. Large home improvement retail chains and appliance stores play a crucial role in educating consumers regarding filtration technologies, system compatibility, and maintenance requirements. Additionally, offline retail outlets provide opportunities for product demonstrations and direct comparison between different filtration systems, which further encourages consumer purchases.

Online sales channels are expanding rapidly as consumers increasingly research and purchase home appliances through e-commerce platforms. Direct-to-consumer brand websites and major online marketplaces are enabling manufacturers to reach wider audiences while reducing reliance on traditional retail distribution networks. Online platforms also allow consumers to compare filtration technologies, read product reviews, and access subscription-based filter replacement services. The rise of digital retail ecosystems and smart home product marketplaces is expected to accelerate online sales growth over the coming years, particularly in technologically advanced markets such as North America, Europe, and parts of Asia-Pacific.

End-User Insights

Residential consumers represent the largest end-user segment in the under-sink water filter system market. Increasing awareness regarding waterborne diseases, aging municipal water infrastructure, and rising concerns over drinking water contamination are encouraging households to install permanent filtration solutions. Many consumers are also shifting away from bottled water consumption due to environmental concerns and plastic waste reduction initiatives, further supporting the adoption of home filtration systems. Small commercial establishments such as restaurants, cafés, and coffee shops are also adopting filtration systems to improve water quality for cooking and beverage preparation. Purified water enhances beverage flavor consistency, particularly for coffee and tea preparation, which has become a key driver for filtration system adoption in the hospitality sector.

Large commercial facilities, including hotels, corporate offices, and food processing facilities, require high-capacity filtration systems to support large-scale water consumption. These facilities often install multi-stage filtration systems to ensure reliable water quality for employees, customers, and operational processes. Institutional facilities such as hospitals, educational institutions, and government buildings are increasingly prioritizing water purification systems to ensure public health safety. In healthcare environments, access to clean and contaminant-free water is essential for patient care, food preparation, and medical equipment sanitation, which is driving adoption within this segment.

Explore more data points, trends and opportunities Download Free Sample Report

Under Sink Water Filter System Market Segmentations

By Filtration Technology

- Reverse Osmosis (RO) Filtration Systems

- Activated Carbon Filtration Systems

- Ultrafiltration (UF) Systems

- Ultraviolet (UV) Filtration Systems

- Ion Exchange Filtration Systems

- Ceramic Filtration Systems

- Multi-Stage Hybrid Filtration Systems

By Application

- Residential Household Filtration

- Commercial Filtration

- Institutional Filtration

By Distribution Channel

- Online Retail

- Offline Retail

By End User

- Residential Consumers

- Small Commercial Establishments

- Large Commercial Facilities

- Institutional Facilities

Regional Insights

North America

North America represents the largest regional market, accounting for approximately 34% of global demand in 2025. The United States is the dominant country within the region, contributing nearly 28% of global market revenue. Strong consumer awareness regarding water contamination, aging municipal water infrastructure, and high disposable incomes are major factors supporting market growth. Several high-profile water contamination incidents over the past decade have significantly increased public awareness regarding drinking water safety, prompting households to adopt point-of-use filtration technologies. In addition, the growing popularity of smart home appliances and connected water filtration systems is further driving demand for advanced under-sink filtration systems in the region.

Europe

Europe accounts for roughly 27% of the global market share. Countries such as Germany, the United Kingdom, France, and Italy are leading adopters of home water filtration technologies. The region benefits from strong environmental awareness and strict regulatory frameworks related to water safety and environmental protection. The increasing emphasis on sustainability and the reduction of single-use plastic consumption is encouraging households to adopt permanent water purification solutions rather than relying on bottled water. Additionally, the expansion of energy-efficient home appliances and eco-friendly housing developments across Europe is supporting the integration of advanced filtration systems into residential kitchens.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market for under-sink water filtration systems. Rapid urbanization, industrial pollution, and increasing concerns regarding drinking water quality are major factors driving market growth across the region. China and India represent the largest markets due to their large populations and rapidly expanding middle-class consumer base. Increasing awareness regarding waterborne diseases and growing consumer spending on home appliances are accelerating the adoption of filtration systems in urban households. Government initiatives aimed at improving water infrastructure and sanitation standards are also indirectly supporting market growth. In addition, the expansion of e-commerce platforms and direct-to-consumer appliance sales channels is enabling filtration system manufacturers to penetrate emerging markets more effectively.

Latin America

Latin America accounts for approximately 6% of global market demand, with Brazil and Mexico representing the largest markets in the region. Rapid urban population growth and increasing awareness regarding drinking water quality are driving the adoption of household filtration systems. In several Latin American countries, inconsistent municipal water treatment infrastructure and concerns regarding groundwater contamination are encouraging consumers to install point-of-use filtration systems. The growing middle-class population and expansion of modern retail channels are further supporting market penetration across the region.

Middle East & Africa

The Middle East and Africa region represents roughly 5% of global market demand. Water scarcity and heavy dependence on desalinated water sources in countries such as Saudi Arabia, the United Arab Emirates, and Israel are key factors driving the adoption of advanced household filtration systems. Desalinated water often contains mineral imbalances or residual chemicals, which encourages consumers to install additional filtration systems at the household level. Additionally, rapid urban development and rising residential construction across Gulf Cooperation Council (GCC) countries are creating new opportunities for under-sink filtration system adoption. Increasing investment in water treatment infrastructure and sustainability initiatives is also supporting market growth across the region.

Key Players in the Under-Sink Water Filter System Market

- A. O. Smith Corporation

- 3M Company

- Pentair plc

- Culligan International

- Brita GmbH

- LG Electronics

- Panasonic Corporation

- Kent RO Systems Ltd.

- Coway Co., Ltd.

- Eureka Forbes Ltd.

- Whirlpool Corporation

- GE Appliances

- Aquasana Inc.

- Amway Corporation

- Toray Industries