Ultra-High Definition (UHD) Panel 4K Market Size

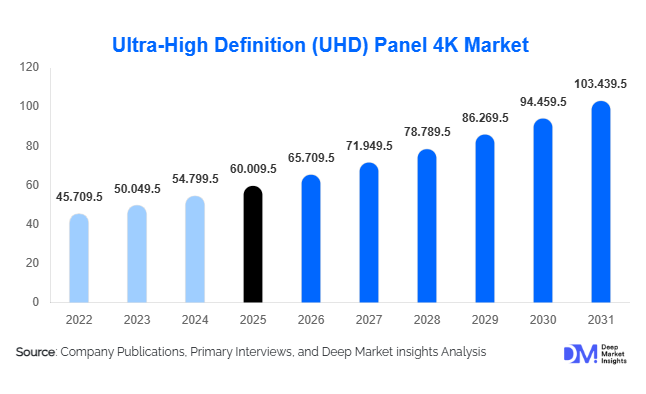

According to Deep Market Insights, the global Ultra-High Definition (UHD) Panel 4K market was valued at USD 60 billion in 2025 and is projected to grow from USD 65.70 billion in 2026 to reach USD 103.43 billion by 2031, expanding at a CAGR of 9.5% during the forecast period (2026–2031). The UHD panel 4K market growth is primarily driven by increasing adoption of 4K content in consumer electronics, rapid expansion in gaming and esports, and integration of UHD panels in commercial, automotive, and healthcare applications worldwide.

Key Market Insights

- LCD remains the dominant technology, due to its cost-effectiveness and mature manufacturing base, capturing over 62% of the market share in 2025.

- 4K resolution leads the market, accounting for approximately 83% of overall panel revenue, even as 8K UHD begins to emerge in premium segments.

- Consumer electronics segment dominates, driven by TV upgrades, monitors, and laptops, representing roughly 62% of total revenue.

- Asia-Pacific is the largest and fastest-growing region, contributing around 37% of global market share in 2025, fueled by manufacturing capacity in China, South Korea, and Japan.

- North America maintains significant demand, with the U.S. alone accounting for nearly 28% of the global market, primarily in premium and gaming segments.

- Technological innovation, including OLED, QLED, and Mini/MicroLED, along with AI-based display enhancements, is reshaping panel performance and consumer adoption patterns.

What are the latest trends in the UHD Panel 4K market?

Premium Technology Adoption

Manufacturers are increasingly shifting toward OLED, QLED, and MiniLED technologies to meet demand for higher contrast ratios, deeper blacks, and energy-efficient displays. Consumers and professional users prioritize premium display experiences for gaming, content creation, and professional applications, pushing growth in advanced UHD panels.

Integration with Gaming and Professional Workstations

The proliferation of esports, 4K content production, and professional creative applications is driving demand for high refresh rate, HDR-capable, and color-accurate panels. Gaming monitors, professional workstations, and high-end TVs are now primary drivers of UHD panel adoption globally.

Commercial and Automotive Deployments

UHD panels are increasingly integrated into digital signage, interactive retail displays, and automotive infotainment dashboards. High-resolution panels improve consumer engagement and safety in vehicles while expanding industrial adoption beyond consumer electronics.

What are the key drivers in the UHD Panel 4K market?

Rising Consumer Demand for High-Resolution Displays

Consumers increasingly prefer sharper visuals, richer color reproduction, and immersive experiences in TVs, monitors, and laptops. UHD panels provide four times the resolution of Full HD displays, accelerating replacement cycles and boosting demand across both residential and commercial segments.

Advancements in Panel Technologies

Adoption of OLED, MicroLED, and Quantum Dot technologies is driving growth in premium and professional segments. These advancements deliver superior contrast, wider color gamut, and energy efficiency, enhancing user experience in gaming, professional, and commercial applications.

Growth in OTT Content and Gaming Applications

The global expansion of 4K streaming content and high-definition gaming has created strong demand for UHD panels. Users in both emerging and developed markets are upgrading displays to meet content standards, driving higher unit shipments and market revenue growth.

What are the restraints for the global market?

High Manufacturing Complexity and Costs

Advanced panel technologies like OLED and MicroLED require complex fabrication processes, high-quality materials, and strict production controls. Elevated production costs result in higher retail prices, slowing adoption in price-sensitive markets.

Content and Infrastructure Limitations

Emerging regions face limitations in high-speed broadband infrastructure and availability of 4K content, restricting UHD panel adoption. Uneven network capabilities can impede seamless streaming, particularly in areas with developing digital infrastructure.

What are the key opportunities in the UHD Panel 4K industry?

Emerging Commercial and Public Display Deployments

Smart city initiatives, transportation hubs, and retail sectors are increasingly adopting UHD panels for digital signage and interactive displays. Governments and enterprises investing in smart infrastructure provide long-term stable demand for UHD panels, offering growth beyond traditional consumer markets.

Automotive and Healthcare Applications

Automotive infotainment, head-up displays, and healthcare imaging solutions present high-value opportunities for UHD panels. These sectors prioritize resolution, color accuracy, and reliability, enabling manufacturers to target premium segments with higher profit margins and longer replacement cycles.

Integration with Streaming and Gaming Ecosystems

The rising availability of 4K content across OTT platforms and demand for immersive gaming experiences continue to create opportunities for UHD panel manufacturers. Bundled solutions, optimized monitors for streaming and gaming, and professional workstations offer differentiated market entry points.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 60 Billion |

| Market Size in 2026 | USD 65.70 Billion |

| Market Size in 2031 | USD 103.43 Billion |

| CAGR | 9.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

In the global UHD Panel 4K market, LCD technology dominates in volume due to its cost-effectiveness, mature manufacturing ecosystem, and wide availability across consumer and commercial segments. LCD panels account for the bulk of shipments, particularly for mid-range TVs, laptops, and monitors. Meanwhile, OLED, QLED, and MiniLED panels cater to premium users who prioritize superior color accuracy, contrast ratios, and energy efficiency. These advanced technologies are increasingly adopted in high-end TVs, gaming monitors, professional workstations, and large-format commercial displays. Mid-sized displays (40–60 inches) are the most widely shipped, balancing affordability and immersive viewing, while large-format panels (>75 inches) are gaining traction in commercial signage, corporate conference rooms, and creative professional applications, reflecting a trend toward larger, high-resolution deployments in premium and enterprise segments.

Application Insights

Consumer electronics such as televisions, laptops, and monitors remain the largest application for UHD 4K panels, driven by growing demand for home entertainment, remote work, and gaming. Gaming monitors and professional workstations represent fast-growing segments, where high refresh rates, HDR capabilities, and color accuracy are critical. Additionally, commercial digital signage is emerging as a major growth driver, particularly in retail, hospitality, and transportation sectors, as businesses upgrade legacy displays to UHD solutions to enhance customer engagement. Automotive infotainment systems and healthcare imaging applications are emerging niches, with UHD panels improving driver experience, in-cabin displays, and diagnostic accuracy, respectively. The diversification of applications across industries is a key factor sustaining long-term market growth.

Distribution Channel Insights

The UHD panel 4K market is predominantly driven by OEM and direct manufacturer sales, which supply large-scale consumer electronics brands and commercial clients. Retail and e-commerce channels complement these sales by offering consumers the convenience of online comparisons, transparent pricing, and delivery services. System integrators and value-added resellers (VARs) cater to commercial and industrial end-users, supplying customized panel solutions for signage, workstations, and corporate installations. Premium panels increasingly leverage direct channels, allowing manufacturers to protect margins, ensure quality control, and establish brand loyalty. Emerging trends include subscription-based B2B models and online configurators, which enhance customer engagement and enable tailored UHD panel solutions for diverse requirements.

End-Use Insights

The residential segment remains the largest consumer of UHD panels, fueled by replacement cycles for TVs, gaming monitors, and high-end laptops. Commercial and industrial applications, including digital signage, professional workstations, and enterprise displays, are among the fastest-growing segments, benefiting from increased digitalization and the need for high-resolution visual solutions. Emerging sectors, such as automotive infotainment and medical imaging, offer high-value growth opportunities, where premium panels command superior pricing. Export-driven demand is led by Asia-Pacific manufacturing hubs, particularly China, South Korea, and Japan, which supply panels globally to North America, Europe, and other high-demand regions. The combined effect of residential replacement cycles, commercial modernization, and export expansion sustains the overall market momentum.

Explore more data points, trends and opportunities Download Free Sample Report

Ultra-High Definition (UHD) Panel 4K Market Segmentations

By Product Type

- LCD

- OLED

- QLED

- MiniLED

- MicroLED

By Resolution

- 4K UHD (3840×2160)

- 8K UHD (7680×4320)

- Others (e.g., 5K)

By Application

- Consumer Electronics

- Commercial Displays

- Gaming & Esports Displays

- Professional & Creative Workstations

- Automotive Displays

- Healthcare & Medical Imaging

- Education & Corporate Training

By End-User

- Residential

- Commercial

- Industrial

- Enterprise/Corporate

- Public Sector

By Distribution Channel

- OEM & Direct Manufacturer Sales

- Retail & E-Commerce

- System Integrators

- Value-Added Resellers (VARs)

- B2B Contract Sales

Regional Insights

North America

The U.S. dominates regional UHD panel demand, with strong adoption of premium TVs, gaming monitors, and professional displays, representing approximately 28% of global market share in 2025. Canada also contributes significantly. Key growth drivers include high household incomes, widespread availability of 4K content, and the surge in esports and streaming platforms, which increase the need for high-resolution displays. Enterprise adoption in corporate offices and digital signage further supports market expansion. Consumer preference for large-format and high-end monitors, along with ongoing replacements of older HD panels, ensures sustained regional demand.

Europe

Europe accounts for 20% of the global market, with Germany, the U.K., and France as leading contributors. Drivers for growth include high penetration of premium displays, consumer awareness of high-resolution benefits, and eco-conscious purchasing trends that favor energy-efficient panels such as OLED and QLED. Commercial adoption of UHD panels in corporate offices, retail spaces, and public institutions further fuels demand. Government incentives for energy-efficient electronics and smart city infrastructure initiatives are also contributing to the adoption of UHD panel technology in both residential and commercial applications.

Asia-Pacific

Asia-Pacific is the largest and fastest-growing region (37% of global market) due to production hubs in China, South Korea, and Japan. Growth drivers include rapid urbanization, rising middle-class incomes, high digital content consumption, and strong export capabilities. China and South Korea are leading manufacturing nations, supplying panels for both domestic and global consumption. Expanding OTT platforms, gaming penetration, and corporate digitalization drive domestic adoption, while export-oriented production ensures strong regional growth. Government initiatives supporting advanced display technology and smart infrastructure also stimulate market expansion across APAC.

Latin America

Brazil, Mexico, and Argentina are gradually adopting UHD panels, primarily for consumer electronics and commercial applications. Growth drivers include increased disposable incomes, rising interest in 4K content and gaming, and modern retail and signage upgrades. While adoption is slower compared to developed markets, government initiatives promoting digital infrastructure and retail modernization are expected to accelerate regional growth.

Middle East & Africa

Key countries include the UAE, Saudi Arabia, and South Africa. Drivers for growth in the Middle East include high-income populations, rising demand for premium TVs and monitors, and expanding corporate and retail infrastructure requiring UHD panels. Africa primarily serves as a production hub and benefits from tourism-driven installations. The combination of growing consumer wealth, infrastructure development, and high-end commercial deployment supports regional market expansion. Intra-regional trade and urbanization are expected to further enhance adoption over the forecast period.

Key Players in the UHD Panel 4K Market

- Samsung Electronics

- LG Display

- BOE Technology Group

- AU Optronics

- Innolux

- Sony Corporation

- Panasonic

- Hisense

- Philips

- Sharp

- TCL Technology

- Vizio

- Hitachi

- Toshiba

- Acer Corporation