Training Dancewear Market Size

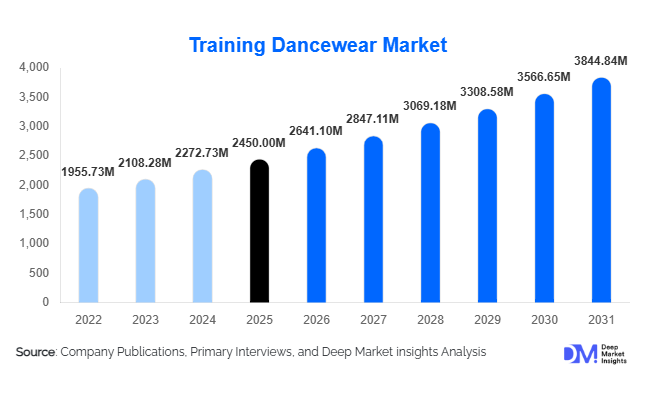

According to Deep Market Insights, the global Training Dancewear Market was valued at approximately USD 2,450 million in 2025 and is projected to grow from around USD 2,641.10 million in 2026 to reach nearly USD 3,844.84 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The market growth is primarily driven by rising global participation in dance-based fitness activities, increasing enrollment in professional dance academies, and continuous innovation in performance-oriented fabrics that enhance comfort, flexibility, and durability.

Key Market Insights

- Dancewear demand is expanding beyond professional dancers, with fitness enthusiasts and recreational users becoming a major consumer base.

- Leotards and nylon-spandex blended fabrics dominate product and material categories due to high elasticity and performance suitability.

- North America leads the global market due to a strong dance education infrastructure and high consumer spending.

- Asia-Pacific is the fastest-growing region, supported by rising disposable incomes and the increasing popularity of dance academies.

- Online retail channels are rapidly expanding, driven by direct-to-consumer strategies and wider product accessibility.

- Sustainability and eco-friendly fabrics are emerging as key trends, influencing product innovation and brand positioning.

What are the latest trends in the Training Dancewear Market?

Shift Toward Sustainable and Performance Fabrics

The market is witnessing a strong shift toward sustainable materials such as organic cotton and recycled polyester. Brands are increasingly adopting eco-friendly production methods to align with environmental concerns and regulatory pressures, particularly in Europe. At the same time, innovation in performance fabrics, such as moisture-wicking, compression-based, and stretch-enhanced textiles, is improving durability and comfort. This dual focus on sustainability and performance is reshaping product development strategies across leading manufacturers.

Digitalization and Direct-to-Consumer Growth

E-commerce platforms and brand-owned online stores are becoming the dominant distribution channels in the training dancewear market. Digital-first strategies, including virtual try-ons, influencer marketing, and AI-driven size recommendations, are improving customer engagement. Social media platforms also play a major role in influencing purchasing decisions, particularly among younger consumers. This shift is enabling brands to bypass traditional retail intermediaries and improve profit margins.

What are the key drivers in the Training Dancewear Market?

Rising Participation in Dance and Fitness Activities

The growing popularity of dance as a fitness activity is one of the strongest drivers of market growth. Programs such as Zumba, barre, and contemporary dance workouts are expanding the consumer base beyond traditional dancers. Increasing health awareness and lifestyle-focused fitness trends are significantly contributing to higher demand for specialized training apparel globally.

Expansion of Dance Education Infrastructure

The proliferation of dance academies, schools, and professional training institutions is generating consistent demand for standardized dancewear. Institutional bulk purchasing, particularly for uniforms and practice wear, plays a major role in sustaining stable revenue streams. Emerging economies are also investing in performing arts education, further supporting long-term market expansion.

Innovation in Fabric and Apparel Design

Technological advancements in textile engineering have significantly improved product functionality. Features such as enhanced elasticity, sweat resistance, and body-contouring designs are making dancewear more performance-oriented. These innovations improve user experience and encourage repeat purchases, particularly among professional dancers.

What are the restraints for the global market?

High Cost of Premium Dancewear

Premium training dancewear products often come at high prices due to advanced materials and specialized designs. This limits adoption in price-sensitive regions, particularly in developing economies where consumers prioritize affordability over performance features.

Substitution from General Activewear

A major restraint is the increasing substitution of specialized dancewear with general activewear. Many recreational users prefer multipurpose sports apparel instead of dedicated dancewear, which reduces demand in the non-professional segment and intensifies competition from broader sportswear brands.

What are the key opportunities in the Training Dancewear Market?

Expansion in Emerging Economies

Emerging markets in Asia-Pacific and Latin America present significant growth opportunities due to rising disposable incomes and increasing participation in structured dance programs. Countries like India, China, and Brazil are witnessing rapid expansion in dance academies and fitness studios, creating strong demand for affordable yet performance-oriented dancewear.

Sustainability-Driven Product Innovation

Growing consumer preference for eco-friendly apparel is opening opportunities for brands investing in sustainable fabrics and ethical manufacturing. Companies that adopt circular fashion models, recycled materials, and low-impact production processes are likely to gain a competitive advantage and premium positioning.

Customization and Smart Apparel Integration

The emergence of customizable dancewear and smart textiles presents a new frontier for innovation. Personalized fits, color customization, and integration of wearable technology for posture correction or performance tracking are expected to attract premium customers and professional dancers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2450 Million |

| Market Size in 2026 | USD 2641.10 Million |

| Market Size in 2031 | USD 3844.84 Million |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Leotards continue to dominate the training dancewear market, accounting for approximately 28% of the global market in 2025. Their leadership is primarily driven by their indispensable role in ballet and structured dance training, where strict dress codes and performance requirements mandate their use. The segment benefits from consistent institutional demand, particularly from dance academies and professional schools, ensuring stable volume growth. Additionally, ongoing innovation in stretchable, breathable, and body-contouring fabrics has enhanced their functionality, further strengthening their dominance.

Tops and bottoms (including leggings and shorts) collectively represent a significant share of the market, supported by their versatility across multiple dance disciplines such as contemporary, hip-hop, and fitness-based dance formats. These products are increasingly favored by recreational users and fitness enthusiasts due to their crossover appeal with activewear. Warm-up apparel, including jackets, wraps, and sweaters, is gaining traction as dancers place greater emphasis on injury prevention and muscle conditioning. Meanwhile, dance footwear such as ballet and jazz shoes remains a specialized yet essential category, with steady demand driven by professional and institutional usage, although its growth rate is comparatively moderate due to longer replacement cycles.

Application Insights

Professional training applications dominate the market, particularly in ballet, contemporary, and jazz disciplines, where standardized attire is mandatory. This segment’s leadership is driven by the structured nature of dance education and the need for performance-oriented apparel that supports movement precision and durability. Institutional demand from academies and performing arts schools ensures recurring purchases, reinforcing its market position.

Dance fitness applications are the fastest-growing segment, fueled by the global rise of programs such as Zumba, barre, and aerobics-based dance workouts. This growth is supported by increasing health awareness and the integration of dance into mainstream fitness routines. Recreational usage is also expanding rapidly, particularly among younger demographics influenced by social media platforms and dance-centric content. Additionally, performance and stage-use applications continue to sustain steady demand, driven by production companies, competitions, and cultural events, ensuring a balanced contribution across both professional and entertainment-driven segments.

Distribution Channel Insights

Online retail has emerged as the fastest-growing distribution channel, accounting for nearly 40% of the global market share. Its growth is driven by increasing internet penetration, convenience, and the expansion of direct-to-consumer (D2C) strategies by leading brands. Features such as virtual fitting tools, personalized recommendations, and global accessibility are further accelerating online adoption, particularly among younger consumers.

Specialty dance stores continue to play a critical role, especially for professional dancers who require expert fitting, high-quality assurance, and personalized guidance. These stores maintain strong relevance in premium and institutional segments. Sports apparel chains and department stores contribute significantly to mid-range demand, offering accessibility and competitive pricing for casual and fitness-oriented users. Institutional procurement channels, including direct sales to dance academies and schools, remain a stable offline segment, driven by bulk purchasing and long-term supplier relationships.

End-Use Insights

Dance academies and institutions represent the largest end-use segment, accounting for approximately 38% of total demand. Their dominance is driven by bulk procurement requirements, standardized uniforms, and consistent enrollment in dance programs globally. This segment provides a stable and recurring revenue base for manufacturers.

Professional dancers form a high-value segment, characterized by demand for premium, performance-enhancing apparel with advanced fabric technologies. Fitness enthusiasts are the fastest-growing end-user group, driven by the increasing popularity of dance-based fitness programs and wellness trends. Recreational users and hobbyists also contribute significantly to market growth, particularly in urban areas where dance is increasingly viewed as a lifestyle activity. The diversification of end-use applications is expanding the market beyond traditional professional boundaries.

Explore more data points, trends and opportunities Download Free Sample Report

Training Dancewear Market Segmentations

By Product Type

- Leotards

- Tops

- Bottoms

- Tights & Hosiery

- Warm-up Apparel

- Dance Footwear

- Dance Undergarments

By Application

- Professional Training

- Dance Fitness

- Recreational Use

- Performance & Stage Use

By End-User

- Dance Academies & Institutions

- Professional Dancers

- Fitness Enthusiasts

- Recreational Users

By Distribution Channel

- Online Retail

- Specialty Dance Stores

- Sports & Apparel Chains

- Department Stores

Regional Insights

North America

North America holds approximately 35% of the global market share in 2025, with the United States being the largest contributor. The region’s dominance is driven by a well-established performing arts ecosystem, high enrollment in dance academies, and strong consumer spending power. Additionally, the presence of leading dancewear brands and advanced retail infrastructure supports product availability and innovation. The growing popularity of dance-based fitness programs and the increasing adoption of premium apparel further reinforce regional demand.

Europe

Europe accounts for around 28% of the global market, led by countries such as the UK, France, Germany, and Italy. The region’s strong heritage in ballet and contemporary dance serves as a key growth driver, supported by government funding for performing arts and cultural programs. Sustainability trends are particularly influential in Europe, with consumers increasingly preferring eco-friendly and ethically produced dancewear. Additionally, the presence of renowned dance institutions and consistent participation in cultural events sustains long-term demand.

Asia-Pacific

Asia-Pacific is the fastest-growing region, driven by rapid urbanization, rising disposable incomes, and increasing awareness of dance as both a career and fitness activity. Key markets such as China, India, Japan, and South Korea are witnessing significant growth in dance academies and fitness studios. Social media influence and the popularity of dance reality shows are further accelerating participation rates. Additionally, strong local manufacturing capabilities enable cost-effective production, making dancewear more accessible to a broader consumer base.

Latin America

Latin America, led by Brazil, Mexico, and Argentina, is experiencing steady growth driven by its deep-rooted cultural affinity for dance forms such as salsa and samba. Increasing participation in structured fitness programs and the gradual expansion of dance academies are key growth drivers. The region’s demand is primarily concentrated in mid-range and recreational segments, with affordability and accessibility playing a crucial role in shaping purchasing behavior.

Middle East & Africa

The Middle East & Africa region is emerging as a promising market, supported by increasing investments in arts education, fitness infrastructure, and lifestyle development. Countries such as the UAE, Saudi Arabia, and South Africa are leading growth, driven by rising disposable incomes and growing interest in wellness and performing arts. Government initiatives promoting cultural diversification and international events are also contributing to market expansion. Additionally, the growing presence of premium retail outlets and international brands is enhancing product availability across the region.