Toilet Cleaner Market Size

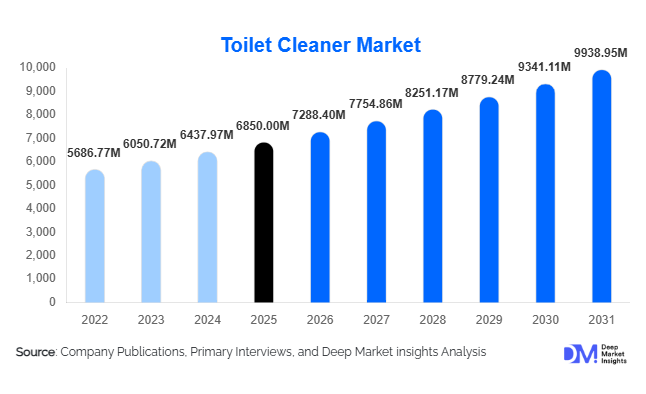

According to Deep Market Insights, the global toilet cleaner market size was valued at USD 6,850 million in 2025 and is projected to grow from USD 7,288.40 million in 2026 to reach USD 9,938.95 million by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The market growth is primarily driven by rising hygiene awareness, increasing urbanization, and growing demand for effective sanitation solutions across residential and commercial sectors. The post-pandemic emphasis on cleanliness and disinfection has significantly boosted product usage frequency, while innovations in eco-friendly formulations and convenient packaging formats continue to reshape consumer preferences globally.

Key Market Insights

- Eco-friendly and biodegradable toilet cleaners are gaining strong traction, driven by regulatory pressure and consumer sustainability preferences.

- The residential segment dominates the market, accounting for nearly 70% of global demand due to widespread household usage.

- Asia-Pacific leads the global market, supported by high population density, sanitation initiatives, and rapid urbanization.

- E-commerce is emerging as a high-growth distribution channel, offering convenience and wider product access.

- Product innovation, such as gel-based and in-tank cleaners, is driving premiumization and differentiation.

- Institutional demand from the healthcare and hospitality sectors continues to provide stable and recurring revenue streams.

What are the latest trends in the toilet cleaner market?

Shift Toward Sustainable and Green Cleaning Solutions

The market is witnessing a strong transition toward eco-friendly toilet cleaners formulated with plant-based and biodegradable ingredients. Regulatory restrictions on harsh chemicals such as hydrochloric acid and bleach are pushing manufacturers to innovate safer alternatives. Consumers are increasingly prioritizing products with minimal environmental impact, recyclable packaging, and reduced toxicity. This trend is particularly prominent in Europe and North America, where sustainability certifications and labeling play a crucial role in purchasing decisions. Companies are also investing in refill packs and concentrated formulations to reduce plastic waste and transportation costs, aligning with global sustainability goals.

Rise of Smart and Automated Cleaning Solutions

Technological advancements are introducing new product categories such as automatic in-tank cleaners, long-lasting disinfectant tablets, and sensor-based dispensing systems. These solutions offer convenience, extended cleaning cycles, and consistent hygiene maintenance. The adoption of such products is increasing in both residential and commercial settings, particularly in developed markets. Additionally, digital marketing and smart home integration are enhancing consumer engagement, enabling brands to position their products as part of modern, tech-enabled lifestyles.

What are the key drivers in the toilet cleaner market?

Growing Hygiene Awareness and Health Concerns

The heightened focus on hygiene, especially after the COVID-19 pandemic, has significantly increased the demand for toilet cleaners. Consumers are prioritizing products that offer strong disinfectant properties and long-lasting protection against germs and bacteria. This shift in behavior has led to higher consumption frequency and increased adoption of premium cleaning solutions.

Urbanization and Expanding Middle-Class Population

Rapid urbanization in emerging economies is driving the adoption of modern sanitation facilities, thereby increasing the demand for toilet cleaning products. Rising disposable incomes and improved living standards are encouraging consumers to shift from traditional cleaning methods to branded and specialized products. The expansion of organized retail and e-commerce platforms further supports market growth.

What are the restraints for the global market?

Environmental and Regulatory Challenges

Strict regulations on chemical usage and environmental impact are posing challenges for manufacturers. Compliance with these regulations often requires significant investment in research and development, increasing production costs and affecting profit margins.

Price Sensitivity in Developing Markets

In many emerging economies, consumers remain highly price-sensitive and often opt for low-cost or unbranded alternatives. This limits the penetration of premium products and creates pricing pressure for established brands.

What are the key opportunities in the toilet cleaner industry?

Expansion in Emerging Markets

Government-led sanitation initiatives and increasing awareness of hygiene are creating significant growth opportunities in regions such as Asia-Pacific, Africa, and Latin America. Companies can tap into these markets by offering affordable and localized product solutions.

Innovation in Eco-Friendly Products

The growing demand for sustainable products presents opportunities for manufacturers to develop plant-based and biodegradable formulations. Brands that successfully position themselves as environmentally responsible can capture premium market segments and enhance brand loyalty.

Product Type Insights

Liquid toilet cleaners dominate the global market, accounting for approximately 42% of the total market share in 2025. This leadership is primarily driven by their superior cleaning efficiency, ability to dissolve tough stains such as limescale and mineral deposits, and ease of application through angled-neck bottles that enhance under-rim reach. The widespread availability of liquid cleaners across both developed and emerging markets, combined with their affordability and strong brand penetration, further strengthens their position. Additionally, manufacturers continue to innovate within this segment by introducing thicker formulations and multi-functional liquids that combine cleaning, disinfection, and fragrance, reinforcing their dominance.

Gel-based cleaners are gaining traction, particularly in premium segments, due to their higher viscosity, which allows longer surface contact time and improved cleaning performance. This makes them highly effective for deep cleaning and targeted application. Meanwhile, tablets and in-tank cleaners are emerging as fast-growing sub-segments, especially in developed regions such as North America and Europe. Their convenience, automated cleaning action, and long-lasting performance appeal to time-constrained consumers seeking low-maintenance hygiene solutions. This shift toward convenience-driven products is expected to gradually increase their market penetration.

Application Insights

Disinfection and germ-kill applications lead the market, capturing approximately 35% of the global share in 2025. This dominance is strongly driven by heightened hygiene awareness and increased consumer focus on eliminating bacteria and viruses, particularly in the post-pandemic environment. Products that offer proven antimicrobial efficacy, including those with bleach or advanced disinfectant formulations, are witnessing sustained demand across both residential and institutional segments. Regulatory emphasis on sanitation in commercial spaces such as hospitals and food service establishments further reinforces this segment’s leadership.

Limescale and stain removal applications remain critical, particularly in regions with hard water conditions such as parts of Europe and the Asia-Pacific. These products are specifically formulated with strong acids to remove mineral buildup, making them essential in maintaining toilet hygiene and longevity. Deodorization is another rapidly evolving application area, as consumers increasingly prefer products that combine cleaning with long-lasting freshness. Fragrance innovation, including multi-layered scent profiles and odor-neutralizing technologies, is becoming a key differentiator in product development.

Distribution Channel Insights

Offline retail channels dominate the market, accounting for approximately 65% of global sales in 2025. Supermarkets, hypermarkets, and convenience stores remain the primary purchase points due to their wide product assortment, immediate availability, and strong consumer trust. The dominance of offline channels is particularly evident in developing markets, where traditional retail formats continue to play a central role in consumer purchasing behavior. In-store promotions, bulk purchase discounts, and brand visibility further drive sales through these channels.

However, online retail is the fastest-growing distribution segment, supported by increasing internet penetration, smartphone usage, and the convenience of home delivery. E-commerce platforms offer competitive pricing, subscription models, and access to a broader range of products, including niche and eco-friendly brands. Direct-to-consumer (D2C) channels are also gaining prominence, allowing manufacturers to build stronger customer relationships and offer personalized product bundles. This shift toward digital channels is particularly strong in urban areas and among younger demographics.

End-Use Insights

The residential segment dominates the toilet cleaner market, contributing nearly 70% of total demand in 2025. This is primarily driven by the universal need for household sanitation and increasing consumer awareness of hygiene practices. The growing adoption of modern toilets and improved living standards, especially in emerging economies, further supports this segment’s growth. Frequent usage and repeat purchases make residential consumers the backbone of the market.

The commercial segment is witnessing faster growth, particularly in healthcare, hospitality, and corporate facilities. Stringent hygiene regulations, especially in hospitals and clinics, are driving demand for high-performance disinfectant cleaners. The hospitality sector, including hotels and restaurants, is also a key contributor due to the need to maintain cleanliness standards and enhance customer experience. Additionally, public infrastructure projects such as airports, railways, and smart city developments are creating new demand avenues, supported by government investments in sanitation and urban development.

| By Product Type | By Chemical Composition | By Application | By Distribution Channel | By End-Use |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global toilet cleaner market with approximately 38% share in 2025, driven by large population bases in countries such as China and India. Rapid urbanization, rising disposable incomes, and increased awareness of hygiene are key growth drivers in this region. Government-led sanitation initiatives, such as large-scale public cleanliness campaigns, have significantly boosted product adoption. Additionally, expanding retail infrastructure and the growing penetration of e-commerce platforms are enhancing product accessibility. The region’s strong manufacturing base also supports cost-effective production, making products more affordable and widely available.

North America

North America accounts for around 22% of the global market, with the United States leading demand. Growth in this region is driven by high consumer awareness, strong preference for premium and specialized products, and widespread adoption of advanced cleaning solutions such as gel-based and automated cleaners. The presence of major global brands and continuous product innovation further supports market expansion. Additionally, increasing demand for eco-friendly and non-toxic formulations is shaping product development, as consumers prioritize sustainability and safety.

Europe

Europe holds nearly 20% of the global market share, led by countries such as Germany, the UK, and France. The region’s growth is strongly influenced by stringent environmental regulations, which are driving the adoption of eco-friendly and biodegradable cleaning products. Consumers in Europe are highly conscious of sustainability, leading to increased demand for green formulations and recyclable packaging. Furthermore, the presence of established retail networks and high penetration of premium products contribute to steady market growth.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth, supported by increasing investments in infrastructure and urban development. Countries in the Gulf Cooperation Council (GCC) are investing heavily in public sanitation, hospitality, and tourism infrastructure, driving demand for toilet cleaning products. Rising awareness of hygiene, particularly in urban areas, and improving economic conditions are also contributing to market expansion. In Africa, gradual improvements in sanitation access and government initiatives aimed at enhancing public health are expected to support long-term growth.

Latin America

Latin America is witnessing moderate but consistent growth, with Brazil and Mexico as key markets. Urbanization, improving economic conditions, and increasing consumer awareness of hygiene are primary drivers in this region. The expansion of modern retail formats and growing e-commerce adoption are enhancing product availability. Additionally, rising investments in residential and commercial infrastructure are contributing to increased demand for toilet cleaning products. Price sensitivity remains a factor, encouraging manufacturers to offer a mix of affordable and mid-range product options to cater to diverse consumer segments.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Toilet Cleaner Market

- Reckitt Benckiser

- Procter & Gamble

- Unilever

- Henkel

- SC Johnson

- Colgate-Palmolive

- Kao Corporation

- Church & Dwight

- Godrej Consumer Products

- Dabur India

- Amway

- Lion Corporation

- Clorox

- Liby Group

- Nice Group