Tennis Shoes Market Size

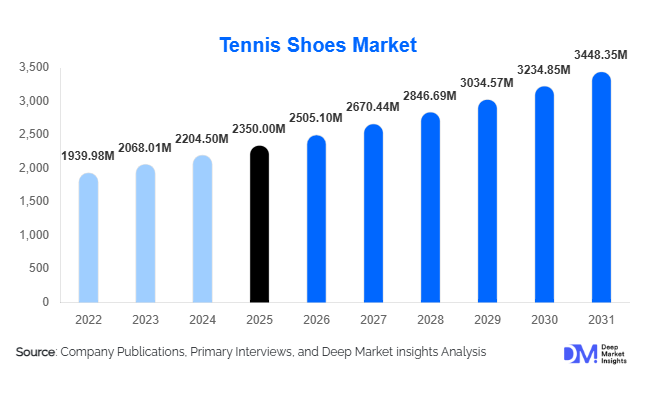

According to Deep Market Insights, the global tennis shoes market size was valued at USD 2,350 million in 2025 and is projected to grow from USD 2,505.10 million in 2026 to reach USD 3,448.35 million by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The tennis shoes market growth is primarily driven by increasing participation in tennis and racquet sports, the rapid expansion of athleisure as a lifestyle trend, and continuous innovation in footwear technology aimed at enhancing performance, comfort, and durability.

Key Market Insights

- Performance-oriented tennis shoes dominate the market, driven by demand from professional and serious amateur players requiring court-specific features.

- Athleisure adoption is expanding the consumer base, with tennis shoes increasingly used for casual and everyday wear.

- North America leads the global market, supported by high sports participation rates and strong purchasing power.

- Asia-Pacific is the fastest-growing region, driven by rising disposable incomes and expanding sports infrastructure in countries like China and India.

- Synthetic materials are the most widely used, offering durability, flexibility, and cost advantages over traditional materials.

- E-commerce channels are rapidly gaining traction, although offline retail remains dominant due to fitting preferences.

What are the latest trends in the tennis shoes market?

Rise of Athleisure and Lifestyle Integration

Tennis shoes are increasingly transitioning beyond sports-specific applications into everyday fashion. The global athleisure movement has positioned tennis footwear as a versatile product suitable for both performance and casual use. Consumers are prioritizing comfort, style, and brand identity, leading to increased demand for hybrid designs that combine functionality with aesthetics. Brands are collaborating with designers and influencers to create limited-edition collections that appeal to fashion-conscious buyers. This trend has significantly expanded the addressable market, with lifestyle consumers accounting for a growing share of total demand.

Technological Advancements in Performance Footwear

Innovation in cushioning systems, stability features, and lightweight materials is reshaping the tennis shoes market. Technologies such as energy-return foams, gel-based cushioning, and advanced outsole grip patterns are enhancing player performance while reducing injury risks. Manufacturers are also leveraging biomechanics research to design shoes tailored to specific playing styles and court surfaces. Digital tools, including AI-based foot scanning and customization platforms, are enabling personalized footwear solutions, further strengthening consumer engagement and brand differentiation.

What are the key drivers in the tennis shoes market?

Growing Participation in Tennis and Recreational Sports

The increasing global interest in tennis as both a professional and recreational activity is a major growth driver. Rising health awareness and fitness trends are encouraging individuals across age groups to engage in sports, boosting demand for specialized footwear. International tournaments and media visibility are further enhancing the sport’s popularity, creating aspirational demand for high-performance tennis shoes.

Expansion of Athleisure and Casual Footwear Markets

The convergence of sportswear and casual fashion has significantly expanded the tennis shoes market. Consumers are increasingly adopting sports footwear for daily use, driven by comfort and style preferences. This shift has led to higher sales volumes, particularly in mid-range and premium segments, as brands focus on versatile designs that cater to both athletes and lifestyle users.

What are the restraints for the global market?

High Cost of Premium Tennis Shoes

Advanced technologies and premium branding contribute to higher prices, limiting accessibility for price-sensitive consumers. This is particularly evident in emerging markets, where affordability remains a key concern. High product costs can restrict market penetration among entry-level players and casual users.

Intense Competition and Price Pressure

The market is highly competitive, with numerous global and regional players offering similar products. This leads to price competition, especially in the mid-range segment, impacting profit margins. Differentiation becomes challenging, requiring continuous investment in innovation and marketing.

What are the key opportunities in the tennis shoes industry?

Expansion in Emerging Markets

Emerging economies such as India, China, and Brazil present significant growth opportunities due to increasing sports participation and rising disposable incomes. Government initiatives promoting fitness and sports infrastructure development are further supporting market expansion. Companies can tap into these markets by offering affordable, performance-driven products tailored to local needs.

Sustainable and Eco-Friendly Footwear

Sustainability is becoming a critical focus area, with consumers demanding environmentally responsible products. Manufacturers are adopting recycled materials, bio-based components, and low-emission production processes. Circular economy initiatives, including recycling programs and sustainable packaging, are expected to enhance brand loyalty and regulatory compliance.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2350 Million |

| Market Size in 2026 | USD 2505.10 Million |

| Market Size in 2031 | USD 3448.35 Million |

| CAGR | 6.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Performance tennis shoes continue to dominate the global market, accounting for approximately 62% of the total market share in 2025. The leadership of this segment is primarily driven by the increasing demand for sport-specific footwear that enhances on-court performance and minimizes injury risks. These shoes are engineered for different court surfaces, such as clay, hard, and grass, incorporating specialized outsole patterns, lateral stability features, and advanced cushioning systems. The growing participation of competitive and semi-professional players globally, along with rising awareness of the importance of proper footwear in preventing injuries, has significantly contributed to the segment’s dominance. Additionally, endorsements by professional athletes and innovations in performance technologies further strengthen consumer preference for this category.

On the other hand, lifestyle or tennis-inspired shoes are gaining strong momentum, particularly among urban consumers. Their versatility, comfort, and alignment with athleisure trends have made them popular for everyday wear. This segment is benefiting from increasing crossover between sportswear and fashion, with brands launching stylish, multi-functional designs that appeal to a broader, non-athletic audience.

Application Insights

Recreational and amateur usage represents the largest application segment, contributing nearly 50% of the total demand. This segment is leading due to the growing adoption of tennis as a leisure and fitness activity across all age groups. Increasing health awareness, the rise of community sports clubs, and greater accessibility to tennis courts have significantly boosted participation rates, especially in emerging economies. Recreational players tend to replace footwear more frequently due to regular usage, further supporting volume growth in this segment.

Professional applications continue to hold a strong position, particularly in the premium segment, where demand is driven by performance requirements and brand endorsements. Meanwhile, athleisure applications are witnessing rapid growth, accounting for around 30% of total demand. This growth is fueled by changing consumer lifestyles, where tennis shoes are increasingly used for casual wear, travel, and light physical activities, thereby expanding their utility beyond traditional sports applications.

Distribution Channel Insights

Offline retail channels dominate the tennis shoes market with approximately 58% share in 2025. The leading position of this segment is largely attributed to consumer preference for physical product trials, particularly for sports footwear, where fit, comfort, and performance are critical purchase factors. Specialty sports stores and multi-brand outlets provide expert guidance, personalized fitting services, and immediate product availability, which enhances consumer confidence and drives higher conversion rates.

However, online retail channels are rapidly gaining traction and are expected to witness the fastest growth over the forecast period. The increasing penetration of e-commerce platforms, availability of detailed product information, customer reviews, and competitive pricing are key drivers of this shift. Additionally, advancements in virtual fitting technologies and easy return policies are reducing barriers associated with online purchases, particularly among younger, tech-savvy consumers.

End-User Insights

The men’s segment represents the largest end-user category, accounting for around 48% of the market in 2025. This dominance is driven by higher participation rates in competitive and recreational tennis among male consumers, as well as greater spending on performance-oriented sports footwear. Men are also more likely to invest in premium and technologically advanced products, contributing to a higher revenue share.

The women’s segment is emerging as the fastest-growing category, supported by increasing female participation in sports and fitness activities worldwide. Brands are actively expanding their women-specific product lines, focusing on design, fit, and performance enhancements tailored to female athletes. The kids’ segment is also witnessing steady growth, driven by rising enrollment in junior tennis programs, school-level sports initiatives, and parental focus on early sports training, which is creating sustained demand for youth-specific tennis footwear.

Explore more data points, trends and opportunities Download Free Sample Report

Tennis Shoes Market Segmentations

By Product Type

- Performance Tennis Shoes

- Lifestyle / Casual Tennis-Inspired Shoes

By Application

- Professional / Competitive Use

- Recreational / Amateur Use

- Athleisure / Casual Wear

By Distribution Channel

- Online Retail

- Offline Retail

By End User

- Men

- Women

- Kids / Junior Players

By Material Type

- Synthetic Materials

- Mesh & Knit Materials

- Leather

- Sustainable / Recycled Materials

Regional Insights

North America

North America holds the largest market share of approximately 32% in 2025, with the United States contributing the majority of regional demand. The region’s dominance is driven by a well-established sports culture, high participation in tennis at both recreational and professional levels, and strong purchasing power among consumers. The presence of leading global brands, extensive retail networks, and frequent product innovation further supports market growth. Additionally, the popularity of tennis tournaments and increasing adoption of athleisure fashion trends continue to drive demand for both performance and lifestyle tennis shoes. Canada complements regional growth through rising participation in recreational sports and increasing health consciousness.

Europe

Europe accounts for around 27% of the global market, with key demand coming from countries such as Germany, France, the United Kingdom, Spain, and Italy. The region benefits from a strong tennis heritage, supported by globally recognized tournaments and a well-developed sports infrastructure. High disposable incomes and a growing preference for premium and sustainable footwear are key growth drivers. Additionally, European consumers are highly inclined toward eco-friendly products, encouraging manufacturers to introduce sustainable tennis shoe lines. The increasing popularity of fitness-oriented lifestyles and government initiatives promoting sports participation are further strengthening market demand across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the tennis shoes market, with a CAGR exceeding 8% during the forecast period. China leads the region in both manufacturing and consumption, benefiting from large-scale production capabilities and rising domestic demand. India is emerging as a high-growth market due to increasing disposable incomes, rapid urbanization, and growing awareness of sports and fitness. Japan and Australia represent mature markets with steady demand driven by established sports cultures and high consumer spending on premium footwear. Key growth drivers in the region include expanding middle-class populations, increasing government investments in sports infrastructure, and the rising influence of Western lifestyle trends, which are boosting demand for both performance and athleisure footwear.

Latin America

Latin America holds a moderate share of around 6–8%, with Brazil and Mexico being the primary markets. Growth in this region is driven by urbanization, rising youth population, and increasing participation in sports and recreational activities. The growing influence of global sports brands and improving retail penetration are also contributing to market expansion. However, economic volatility and price sensitivity remain key challenges, encouraging demand for mid-range and affordable tennis shoes. Despite these constraints, the region presents long-term growth potential due to increasing sports awareness and infrastructure development.

Middle East & Africa

The Middle East & Africa region accounts for approximately 5% of the global market, with growth concentrated in countries such as the United Arab Emirates, Saudi Arabia, and South Africa. The market is being driven by increasing investments in sports infrastructure, rising disposable incomes, and growing awareness of fitness and healthy lifestyles. The Middle East, in particular, is witnessing strong demand for premium and branded footwear due to high consumer spending and a preference for international brands. In Africa, gradual improvements in economic conditions and expanding urban populations are supporting demand, although growth remains moderate compared to other regions. Government initiatives promoting sports participation and international sporting events are expected to further accelerate market growth in the coming years.