Tennis Racquet Market Size

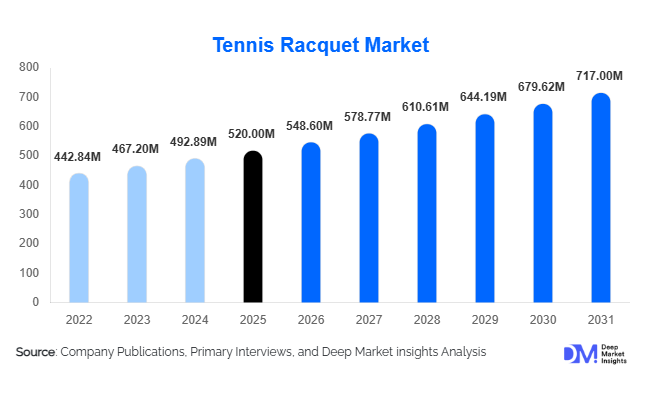

According to Deep Market Insights, the global tennis racquet market size was valued at USD 520 million in 2025 and is projected to grow from USD 548.60 million in 2026 to reach USD 717.00 million by 2031, expanding at a CAGR of 5.5% during the forecast period (2026–2031). The tennis racquet market growth is primarily driven by increasing global participation in tennis, rising health and fitness awareness, and continuous advancements in racquet materials and performance technologies. The expansion of tennis academies, the growing popularity of professional tournaments, and increased accessibility through e-commerce platforms are further contributing to steady market expansion.

Key Market Insights

- Graphite and carbon fiber racquets dominate the market, accounting for over 65% share due to superior performance and lightweight properties.

- Mid-range racquets lead in volume sales, driven by affordability and balanced performance for intermediate players.

- North America holds the largest market share, supported by a strong tennis culture and high consumer spending.

- Asia-Pacific is the fastest-growing region, fueled by rising participation and sports infrastructure investments.

- Technological innovation, including smart racquets and performance analytics, is reshaping product development.

- E-commerce channels are rapidly expanding, improving accessibility and boosting global distribution.

What are the latest trends in the tennis racquet market?

Shift Toward Lightweight and High-Performance Materials

The market is witnessing a strong shift toward advanced materials such as graphite and carbon fiber composites. These materials enhance power, control, and maneuverability while reducing player fatigue. Manufacturers are investing heavily in R&D to develop racquets with improved aerodynamics, larger sweet spots, and vibration-dampening technologies. This trend is particularly prominent among intermediate and professional players seeking competitive advantages. Additionally, hybrid material designs combining fiberglass and Kevlar are gaining traction for durability and performance optimization.

Emergence of Smart and Connected Racquets

Smart racquets integrated with sensors and IoT capabilities are gaining popularity, especially among advanced players and training academies. These racquets provide real-time data on swing speed, impact location, and shot accuracy, enabling performance analysis through mobile applications. This trend is aligned with the broader adoption of wearable technology in sports. Companies are leveraging digital ecosystems to enhance user engagement, offering coaching insights and personalized recommendations. As technology costs decline, smart racquets are expected to penetrate mid-range segments as well.

What are the key drivers in the tennis racquet market?

Growing Global Participation in Tennis

The increasing number of recreational and professional tennis players is a major driver for market growth. Tennis is gaining popularity as a fitness-oriented sport suitable for all age groups. Governments and sports organizations are promoting tennis through grassroots programs, tournaments, and school-level participation, expanding the consumer base globally.

Technological Advancements in Racquet Design

Continuous innovation in materials and design is significantly enhancing racquet performance. Features such as improved string patterns, shock absorption systems, and customizable grip sizes are attracting players across skill levels. These advancements are encouraging frequent product upgrades, particularly among serious players and professionals.

Expansion of Tennis Infrastructure and Academies

The growth of tennis academies, clubs, and international tournaments is driving equipment demand. Emerging markets are investing in sports infrastructure, while established regions continue to host high-profile tournaments that influence consumer purchasing behavior. Endorsements by professional athletes also play a critical role in boosting brand visibility and demand.

What are the restraints for the global market?

High Cost of Premium Racquets

Premium racquets with advanced materials and technologies often exceed USD 150–200, limiting accessibility for price-sensitive consumers. This creates a barrier to entry for beginners and casual players, particularly in developing regions.

Competition from Alternative Sports

The growing popularity of sports such as badminton, padel, and pickleball is posing a challenge to tennis racquet demand. These sports require lower initial investment and are often perceived as easier to learn, attracting new players who might otherwise choose tennis.

What are the key opportunities in the tennis racquet industry?

Expansion in Emerging Markets

Asia-Pacific and Latin America present significant growth opportunities due to rising disposable incomes and increasing sports participation. Countries such as India, China, and Brazil are investing in tennis infrastructure and promoting grassroots development. Companies that adopt localized pricing and distribution strategies can capture substantial market share in these regions.

Adoption of Smart Racquet Technology

The integration of sensors and analytics into racquets offers opportunities for premium product differentiation. Smart racquets enable players to track performance metrics and improve gameplay, appealing to tech-savvy consumers. This trend also opens avenues for subscription-based coaching platforms and digital ecosystems.

Sustainability and Eco-Friendly Manufacturing

Growing environmental awareness is encouraging manufacturers to adopt sustainable materials and production processes. The use of recycled carbon fiber and bio-based composites can enhance brand image and attract environmentally conscious consumers, particularly in Europe and North America.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 520 Million |

| Market Size in 2026 | USD 548.60 Million |

| Market Size in 2031 | USD 717 Million |

| CAGR | 5.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Tweener racquets dominate the global tennis racquet market, accounting for approximately 38% of the total market share in 2025. The primary driver behind this leadership position is their balanced combination of power and control, making them highly versatile across a wide spectrum of players. This segment is particularly favored by intermediate players, who represent the largest and fastest-expanding consumer base globally. As more recreational players transition toward performance-oriented gameplay, the demand for tweener racquets continues to rise. Power racquets remain popular among beginners due to their larger head sizes and enhanced shot assistance, reducing the learning curve. Control racquets, on the other hand, cater to advanced and professional players who prioritize precision and shot placement. Spin racquets are witnessing increasing adoption among competitive players, driven by the growing emphasis on aggressive baseline play and topspin techniques. Entry-level racquets continue to generate steady demand, supported by new player participation and grassroots tennis development programs worldwide.

Material Insights

Graphite and carbon fiber racquets lead the material segment, commanding nearly 65% of the global market share in 2025. The dominance of this segment is driven by superior strength-to-weight ratio, enhanced durability, and improved performance characteristics, including better shock absorption and swing speed. Manufacturers are continuously innovating with advanced carbon layering technologies to further optimize performance. Composite racquets, combining materials such as fiberglass and Kevlar, are gaining traction due to their cost-effectiveness and balanced durability, making them suitable for intermediate players. Aluminum racquets remain relevant in the beginner segment, primarily due to their affordability and robustness, especially in emerging markets. Titanium racquets offer incremental strength benefits but occupy a smaller niche due to higher costs. Wooden racquets, while largely obsolete in competitive play, continue to serve niche markets such as collectors and training applications, reflecting a heritage-driven demand rather than performance-based adoption.

Distribution Channel Insights

Offline retail channels continue to dominate the market, accounting for around 60% of total sales in 2025. This leadership is primarily driven by the ability of specialty sports stores to provide personalized recommendations, physical product trials, and immediate availability, which are critical factors influencing purchase decisions, especially for high-value racquets. Consumers often prefer in-store experiences to evaluate grip, weight, and balance before purchasing. However, online retail is emerging as the fastest-growing distribution channel, fueled by increasing internet penetration, competitive pricing, and access to a broader range of products. E-commerce platforms and brand-owned websites are enabling global reach and direct consumer engagement. Additionally, direct-to-consumer (D2C) strategies are gaining momentum, allowing manufacturers to improve margins, offer customization options, and build stronger brand loyalty through digital ecosystems and targeted marketing campaigns.

End-Use Insights

Recreational players represent the largest end-use segment, contributing to over 55% of total market demand in 2025. This dominance is driven by the growing popularity of tennis as a fitness and leisure activity, particularly among urban populations seeking active lifestyles. The accessibility of tennis courts and community programs further supports this segment’s growth. Sports academies and clubs are the fastest-growing end-use segment, expanding at a CAGR of over 6.5%, driven by structured training programs, youth development initiatives, and increasing professional aspirations among players. These institutions generate consistent demand for high-performance racquets and bulk procurement. Educational institutions are also contributing significantly, especially in North America and Europe, where tennis is integrated into school and university sports programs. This segment not only drives volume sales but also fosters long-term consumer engagement by introducing the sport at an early age.

Explore more data points, trends and opportunities Download Free Sample Report

Tennis Racquet Market Segmentations

By Product Type

- Power Racquets

- Control Racquets

- Tweener Racquets

- Spin Racquets

- Beginner/Entry-Level Racquets

By Material

- Graphite/Carbon Fiber Racquets

- Composite Racquets

- Aluminum Racquets

- Titanium Racquets

- Wooden Racquets

By Distribution Channel

- Online Retail

- Offline Retail (Specialty Stores)

- Direct-to-Consumer Channels

By End-Use

- Recreational Players

- Professional Players

- Sports Academies & Clubs

- Educational Institutions

Regional Insights

North America

North America holds approximately 32% of the global tennis racquet market share in 2025, with the United States accounting for the majority of regional demand. The region’s dominance is driven by a well-established tennis culture, high disposable income levels, and widespread access to advanced sports infrastructure. Additionally, the strong presence of professional tournaments and tennis leagues significantly influences consumer purchasing behavior. The region also leads in premium racquet adoption, supported by a consumer base willing to invest in high-performance equipment. Technological innovation, including smart racquets and customization features, is rapidly adopted in this market. Furthermore, the growth of tennis academies and collegiate sports programs continues to sustain long-term demand.

Europe

Europe accounts for around 28% of the global market share, with key contributions from countries such as France, Germany, the United Kingdom, and Spain. The region’s growth is driven by a deep-rooted tennis heritage, strong club culture, and the presence of major international tournaments. Government support for sports participation and well-developed training infrastructure further enhance market expansion. Europe also demonstrates a strong preference for technically advanced and sustainable racquets, aligning with increasing environmental awareness among consumers. The popularity of tennis at both amateur and professional levels ensures consistent demand across all product categories, while rising participation among younger demographics is supporting future growth.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 7% during the forecast period. China and India are the primary growth engines, driven by rapid urbanization, rising middle-class income, and increasing government investments in sports infrastructure. National initiatives promoting physical fitness and youth engagement in sports are significantly expanding the player base. Japan contributes strongly through its focus on technological innovation and high-quality manufacturing, while countries such as Australia maintain steady demand due to established tennis traditions. The increasing influence of international tournaments and social media is also encouraging participation, making the region a key target for global manufacturers.

Latin America

Latin America is experiencing steady growth, led by Brazil, Argentina, and Mexico. The region’s expansion is supported by growing sports participation, improving economic conditions, and increasing investments in grassroots tennis programs. Rising interest in international tennis events and the emergence of local talent are also contributing to market development. While price sensitivity remains a challenge, demand for mid-range and entry-level racquets is increasing. Additionally, the expansion of sports retail networks and e-commerce platforms is improving product accessibility across the region.

Middle East & Africa

The Middle East and Africa region is emerging as a promising market, with countries such as the UAE, Saudi Arabia, and South Africa leading demand. Growth in this region is driven by increasing investments in sports infrastructure, rising disposable incomes, and government initiatives promoting international sporting events. The Middle East, in particular, is witnessing a surge in premium sports consumption, supported by luxury lifestyles and global sporting partnerships. In Africa, the development of tennis academies and grassroots programs is gradually expanding the player base. Although the market is still in its early stages, improving infrastructure and growing awareness are expected to drive long-term growth.

Key Players in the Tennis Racquet Market

- Wilson Sporting Goods

- Babolat

- Head

- Yonex

- Tecnifibre

- Prince Global Sports

- Dunlop Sports

- Volkl Tennis

- Pacific Sports

- ProKennex

- Gamma Sports

- Solinco

- Snauwaert

- Angell Sports

- Artengo (Decathlon)