Tableware Market Size

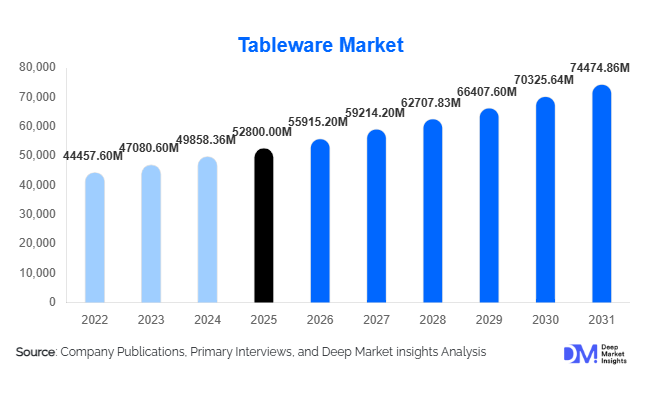

According to Deep Market Insights, the global tableware market size was valued at USD 52,800 million in 2025 and is projected to grow from USD 55,915.20 million in 2026 to reach USD 74,474.86 million by 2031, expanding at a CAGR of 5.9% during the forecast period (2026–2031). The tableware market growth is primarily driven by rising disposable incomes, increasing demand for premium home dining aesthetics, expansion of the hospitality industry, and rapid adoption of sustainable and eco-friendly dining products across residential and commercial sectors.

Key Market Insights

- Premiumization of tableware products is accelerating globally, with consumers increasingly investing in designer and lifestyle-oriented dining collections.

- Sustainable and biodegradable tableware demand is rising, driven by regulations limiting single-use plastics and shifting consumer preferences.

- Asia-Pacific dominates the global tableware market, supported by strong manufacturing bases in China and rising consumption in India.

- Hospitality and foodservice industries remain key demand drivers, particularly post-pandemic recovery in tourism and dining-out culture.

- E-commerce channels are rapidly reshaping distribution, enabling direct-to-consumer growth and global brand expansion.

- Ceramic-based tableware continues to dominate material usage due to durability, aesthetics, and widespread affordability across segments.

What are the latest trends in the tableware market?

Growing Shift Toward Sustainable and Eco-Friendly Tableware

The tableware market is witnessing a strong shift toward sustainable materials such as bamboo, recycled glass, and biodegradable composites. Governments across Europe, North America, and parts of Asia are tightening regulations on single-use plastics, encouraging manufacturers to innovate in eco-friendly alternatives. Hospitality chains and restaurants are increasingly adopting compostable and reusable tableware to reduce environmental footprints. This trend is also supported by rising consumer awareness regarding environmental impact, with younger demographics showing a strong preference for ethically produced dining products. As a result, manufacturers investing in green production processes and certified sustainable materials are gaining a competitive advantage and premium pricing opportunities.

Digitalization and E-Commerce Expansion in Tableware Sales

The rapid expansion of e-commerce platforms has significantly transformed the tableware industry’s distribution structure. Consumers now prefer online platforms for variety comparison, customization options, and doorstep delivery. Direct-to-consumer (D2C) brands are gaining traction by offering personalized dinnerware sets and lifestyle-oriented collections. Technologies such as augmented reality (AR) are being integrated into online shopping experiences, allowing customers to visualize table settings before purchase. Social media-driven marketing and influencer collaborations are also shaping purchasing decisions, especially among younger consumers. This digital transformation is enabling global market penetration for small and mid-sized manufacturers.

What are the key drivers in the tableware market?

Rising Demand from the Hospitality and Foodservice Industry

The global hospitality industry, valued in the multi-trillion-dollar range, is a major driver for tableware demand. Hotels, restaurants, cafes, and catering services require durable, high-quality, and aesthetically appealing tableware for daily operations and premium customer experiences. The rebound in global tourism and the expansion of quick-service restaurants are significantly boosting the bulk procurement of tableware products. Additionally, luxury hospitality brands are increasingly investing in customized and branded tableware to enhance customer experience and brand identity, further strengthening demand.

Increasing Disposable Income and Lifestyle Upgradation

Rising disposable incomes, particularly in emerging economies, are driving household spending on home décor and dining aesthetics. Consumers are increasingly treating tableware as part of lifestyle expression rather than a functional necessity. This shift is encouraging demand for premium and mid-range products, including designer ceramic sets, luxury glassware, and curated dining collections. Urbanization and nuclear family structures are further contributing to increased per-household spending on kitchen and dining products.

What are the restraints for the global market?

Volatility in Raw Material and Energy Costs

The tableware industry is highly sensitive to fluctuations in raw material prices, such as ceramics, metals, glass, and plastics. Energy-intensive production processes, particularly in ceramic firing and glass molding, further increase cost volatility. Rising fuel and electricity prices directly impact manufacturing costs, forcing companies to either absorb margin pressures or pass costs to consumers. This creates pricing instability, particularly in the mid and low-end segments.

Intense Market Fragmentation and Price Competition

The global tableware market is highly fragmented, with numerous regional and local players competing on price. This results in intense price competition, particularly in mass-market products such as plastic and basic ceramic tableware. Smaller manufacturers often struggle to achieve economies of scale, limiting profitability. The presence of low-cost imports further intensifies competition, creating challenges for premium players trying to maintain brand positioning in value-sensitive markets.

What are the key opportunities in the tableware industry?

Expansion of Eco-Friendly and Reusable Product Lines

The increasing global push toward sustainability presents a major opportunity for manufacturers investing in eco-friendly tableware. Products made from bamboo, palm leaf, recycled glass, and biodegradable materials are gaining rapid acceptance across households and foodservice sectors. Governments promoting bans on single-use plastics are further accelerating demand. Companies that establish strong, sustainable branding and certifications can capture premium market segments and long-term contracts with hospitality chains.

Growth of Hospitality and Organized Foodservice Sector in Emerging Markets

Rapid urbanization in Asia-Pacific, the Middle East, and Latin America is fueling the expansion of hotels, restaurants, and catering services. This is significantly increasing the bulk demand for durable and standardized tableware products. Emerging economies such as India, Indonesia, and Vietnam are witnessing strong growth in food delivery and quick-service restaurant chains, further boosting institutional demand. This creates strong opportunities for both global and local manufacturers to expand B2B supply networks.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 52800 Million |

| Market Size in 2026 | USD 55915.20 Million |

| Market Size in 2031 | USD 74474.86 Million |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Dinnerware continues to dominate the global tableware market, accounting for approximately 38% of total market share in 2025. This leadership is primarily driven by its indispensable role across both household and commercial dining environments. The segment benefits from high replacement frequency, growing consumer inclination toward aesthetically appealing dining setups, and increased spending on home décor. Additionally, the expansion of the global hospitality sector, particularly restaurants, hotels, and catering services, has significantly boosted bulk procurement of dinnerware products. Ceramic-based dinnerware leads within this category due to its optimal balance of durability, cost-effectiveness, and premium visual appeal, making it suitable across price segments.

Drinkware represents the second-largest segment, supported by rising consumption of beverages across residential and commercial settings. Increasing demand for premium glassware, specialty mugs, and barware in urban households and hospitality establishments is driving growth. Flatware and cutlery maintain steady demand due to consistent replacement cycles and the widespread adoption of stainless steel products known for longevity and hygiene. Meanwhile, serveware is gaining traction in premium dining, catering, and event management applications, where presentation plays a critical role. The disposable tableware segment is witnessing rapid expansion, driven by the growth of food delivery services, quick-service restaurants, and a shift toward biodegradable alternatives, positioning it as a high-growth niche within the broader market.

Application Insights

Household applications dominate the tableware market, accounting for over 52% of global demand, primarily driven by evolving lifestyle preferences, increased home dining, and growing consumer interest in curated dining experiences. The rise of social hosting culture and the influence of social media trends have further encouraged consumers to invest in visually appealing tableware. Additionally, urbanization and rising disposable incomes, particularly in emerging economies, have expanded the consumer base for mid-range and premium products.

The commercial segment is the fastest-growing, fueled by the rapid expansion of global tourism, hotels, restaurants, and organized foodservice chains. Increasing penetration of quick-service restaurants (QSRs), cafés, and cloud kitchens is significantly driving demand for durable, cost-efficient, and standardized tableware. Institutional applications, including corporate offices, hospitals, and educational institutions, contribute a stable and recurring demand due to bulk purchasing patterns. Emerging applications such as food delivery platforms and shared kitchen spaces are further accelerating demand for both reusable and disposable tableware, particularly in densely populated urban markets where convenience and scalability are critical.

Distribution Channel Insights

Offline retail channels continue to dominate the tableware market, accounting for nearly 58% of total sales. This dominance is driven by consumer preference for physically evaluating product quality, design, and durability before purchase. Supermarkets, hypermarkets, and specialty stores remain key distribution points, especially for mid-range and premium products. These channels also benefit from strong brand visibility and impulse purchasing behavior.

However, online retail is emerging as the fastest-growing channel, supported by the rapid expansion of e-commerce platforms and increasing digital adoption. Consumers are increasingly attracted to the convenience, competitive pricing, and wide product assortment available online. Brand-owned websites and direct-to-consumer (D2C) platforms are enabling manufacturers to offer customized products and enhance customer engagement. B2B distribution channels remain critical for hospitality and institutional buyers, where long-term contracts and bulk procurement drive significant volumes. The shift toward omnichannel strategies is becoming prominent, with companies integrating online and offline experiences to optimize reach and profitability.

Explore more data points, trends and opportunities Download Free Sample Report

Tableware Market Segmentations

By Product Type

- Dinnerware

- Drinkware

- Flatware & Cutlery

- Serveware

- Disposable Tableware

By Material Type

- Ceramic

- Glass

- Metal

- Plastic

- Wood & Bamboo

- Eco-friendly & Composite Materials

By Distribution Channel

- Offline Retail

- Online Retail

- B2B/Institutional Sales

By End-Use

- Household/Residential

- Commercial

- Institutional

Regional Insights

North America

North America holds approximately 24% of the global tableware market, with the United States being the primary contributor. The region’s growth is driven by high disposable income levels, strong consumer focus on home aesthetics, and a well-established hospitality industry. The trend toward premiumization and lifestyle branding is particularly pronounced, with consumers willing to invest in high-quality and designer tableware. Additionally, increasing awareness of sustainability is driving demand for eco-friendly products. The expansion of e-commerce and D2C channels further supports market growth by improving accessibility and product variety.

Europe

Europe accounts for around 22% of the global market share, led by countries such as Germany, France, and the United Kingdom. The region is characterized by strong demand for premium, design-oriented, and artisanal tableware products. Growth is driven by stringent environmental regulations promoting sustainable materials, as well as a cultural emphasis on fine dining and table presentation. European consumers exhibit a high preference for ceramic and porcelain tableware, particularly in premium segments. Additionally, the region’s mature hospitality industry and increasing focus on eco-conscious consumption are key drivers supporting steady market expansion.

Asia-Pacific

Asia-Pacific dominates the global tableware market with approximately 41% share and is also the fastest-growing region. China leads both in terms of production and consumption, benefiting from a strong manufacturing ecosystem and a large domestic market. India is emerging as a high-growth market, driven by rapid urbanization, rising disposable incomes, and an expanding middle-class population. Southeast Asian countries are witnessing increased demand due to growth in the tourism and foodservice industries. Key growth drivers in the region include the expansion of organized retail, the rising adoption of Western dining practices, and the increasing penetration of e-commerce platforms. Additionally, cost-effective manufacturing capabilities in the region support large-scale exports, further strengthening its global dominance.

Latin America

Latin America is experiencing steady growth, with Brazil and Mexico leading regional demand. Rising middle-class populations, urbanization, and improving economic conditions are key drivers supporting increased consumption of tableware products. The expansion of organized retail and foodservice sectors, along with the growing popularity of home dining and social gatherings, is further boosting demand. Additionally, increasing adoption of online retail platforms is improving product accessibility, particularly in urban areas. While the market remains price-sensitive, demand for mid-range and affordable products continues to grow steadily.

Middle East & Africa

The Middle East & Africa region is emerging as a high-potential market, driven primarily by tourism-led economic growth and large-scale hospitality investments. Countries such as the UAE and Saudi Arabia are witnessing significant expansion in luxury hotels, restaurants, and entertainment infrastructure, driving demand for premium tableware. In Africa, South Africa is a key market, supported by both residential consumption and tourism-driven demand. Additional growth drivers include increasing urbanization, rising disposable incomes, and government initiatives to promote tourism and infrastructure development. The region also shows growing interest in premium and customized tableware products, particularly within high-end hospitality segments.

Key Players in the Tableware Market

- Villeroy & Boch

- Arc Group

- Libbey Inc.

- Fiskars Group

- Lenox Corporation

- Noritake Co., Ltd.

- Churchill China plc

- Steelite International

- Rosenthal GmbH

- Portmeirion Group

- Homer Laughlin China Company

- Denby Pottery Company

- Corelle Brands

- Royal Doulton

- Wedgwood