Global Tabletop Kitchen Products Market Size

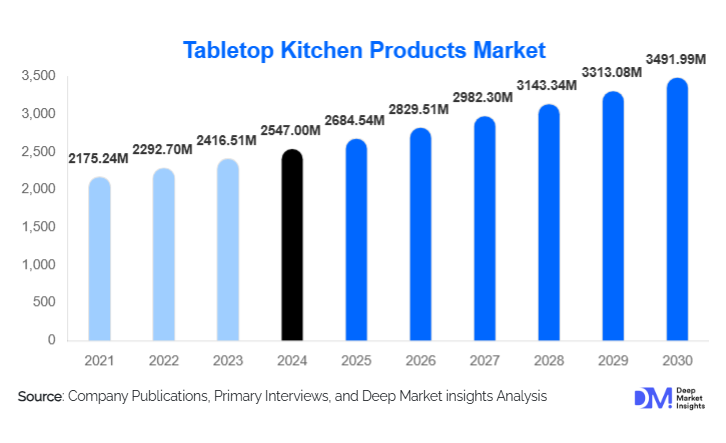

According to Deep Market Insights, the global tabletop kitchen products market size was valued at USD 63.8 billion in 2025 and is projected to grow from USD 68.52 billion in 2026 to reach USD 97.91 billion by 2031, expanding at a CAGR of 7.4% during the forecast period (2026–2031). The market growth is primarily driven by rising demand for premium dining aesthetics, expansion of the global hospitality and foodservice industry, increasing consumer spending on home décor, and rapid adoption of sustainable and eco-friendly tabletop materials across residential and commercial applications.

Key Market Insights

- Premiumization of dining experiences is reshaping consumer demand, with growing preference for designer dinnerware, artisanal ceramics, and luxury glassware.

- Hospitality and foodservice expansion across hotels, cafés, and QSR chains is significantly increasing bulk procurement of durable tabletop products.

- Sustainability trends are driving adoption of recyclable glass, bamboo-based products, BPA-free plastics, and lead-free ceramics.

- Asia Pacific dominates global production and consumption, supported by strong manufacturing hubs in China, India, and Southeast Asia.

- E-commerce channels are accelerating growth, enabling direct-to-consumer sales and wider global product accessibility.

- Customization and lifestyle branding are becoming key differentiators in premium tabletop collections.

What are the latest trends in the tabletop kitchen products market?

Rise of Premium and Aesthetic Dining Culture

Consumers are increasingly treating dining as a lifestyle experience rather than a functional activity. This has led to strong demand for coordinated dinnerware sets, designer cutlery, and visually appealing serveware. Social media platforms such as Instagram and Pinterest are influencing purchase behavior, encouraging consumers to invest in stylish table settings that reflect personal aesthetics. Minimalist, Scandinavian-inspired, and artisanal handcrafted collections are gaining traction globally, particularly in urban households and premium hospitality environments.

Sustainability and Eco-Friendly Product Innovation

Manufacturers are rapidly shifting toward sustainable materials such as recycled glass, bamboo fiber, biodegradable composites, and energy-efficient ceramics. Regulatory pressure in Europe and North America, combined with rising consumer awareness, is accelerating this transformation. Hospitality chains are increasingly adopting eco-certified tabletop products to align with ESG goals. Sustainable packaging and low-emission manufacturing processes are becoming standard practices among leading global players.

Digital Commerce and Direct-to-Consumer Growth

The rapid expansion of e-commerce platforms is transforming the distribution landscape. Consumers now prefer online shopping due to wider product variety, competitive pricing, and convenience. Brands are investing in digital storefronts, augmented reality visualization tools, and AI-driven product recommendations. Social commerce and influencer-led marketing are also playing a crucial role in driving impulse purchases, especially among younger demographics.

What are the key drivers in the tabletop kitchen products market?

Expansion of Hospitality and Foodservice Industry

The global hospitality sector is a major growth driver for tabletop kitchen products. Hotels, restaurants, cafés, and catering services continuously upgrade their tableware to enhance customer experience and brand positioning. Luxury hotels, in particular, are driving demand for premium ceramics, crystal glassware, and designer serveware. Rapid growth in tourism and urban dining culture across Asia Pacific and the Middle East is further strengthening this demand base.

Rising Home Décor and Lifestyle Spending

Consumers are increasingly investing in home aesthetics, with dining spaces becoming a key focus of interior design. The growing popularity of home entertaining, festive dining, and themed table settings is driving demand for coordinated tabletop collections. Urbanization and rising disposable incomes, particularly in emerging economies, are significantly contributing to market expansion.

Material Innovation and Product Durability Improvements

Technological advancements in ceramics, glass tempering, and metal finishing have significantly improved product durability and usability. Scratch-resistant coatings, microwave-safe materials, and lightweight designs are enhancing consumer convenience. These innovations are also reducing replacement cycles in the hospitality sector, supporting long-term demand stability.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in the prices of ceramics, metals, glass, and energy inputs continue to impact manufacturing costs. Supply chain disruptions and global inflationary pressures have increased production expenses, thereby affecting profit margins across mid- and low-tier manufacturers.

Intense Market Competition and Price Pressure

The market faces strong competition from unorganized local manufacturers offering low-cost alternatives. This creates pricing pressure for global brands and limits margin expansion in price-sensitive markets, particularly in developing economies across Asia and Latin America.

What are the key opportunities in the tabletop kitchen products industry?

Growth of Sustainable and Eco-Certified Tableware

Rising environmental awareness is creating strong opportunities for eco-friendly tabletop products. Companies that invest in biodegradable materials, recyclable packaging, and energy-efficient manufacturing processes are gaining competitive advantage. Hospitality chains are increasingly prioritizing sustainability-certified suppliers, creating long-term procurement opportunities.

Expansion of Premium Hospitality Infrastructure

Global expansion of luxury hotels, resorts, and fine-dining restaurants is generating high-value demand for premium tabletop products. The Middle East and Asia Pacific are leading regions for hospitality infrastructure investments, driving strong demand for customized and high-end tableware solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 63.80 Billion |

| Market Size in 2026 | USD 68.52 Billion |

| Market Size in 2031 | USD 97.91 Billion |

| CAGR | 7.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Dinnerware continues to stand as the most influential and revenue-dominant product category in the global tabletop kitchen products market, accounting for approximately 31% of total market share in 2026. Its leadership is primarily driven by its essential role in everyday dining routines across both residential and commercial environments. The recurring replacement cycles of dinnerware, influenced by wear and tear, changing aesthetic preferences, seasonal home décor updates, and lifestyle upgrades, significantly contribute to sustained demand. In urban households, particularly in emerging economies, rising disposable incomes and growing aspirations toward premium dining experiences have further accelerated the adoption of designer dinnerware sets. In commercial spaces such as hotels and restaurants, standardized procurement cycles and bulk purchasing behavior reinforce stable and predictable demand patterns, making dinnerware a foundational revenue pillar within the product landscape.Flatware and cutlery continue to experience steady and resilient expansion, supported by their indispensable use across household and institutional dining. Growth in this segment is strongly linked to the rising penetration of organized hospitality, cloud kitchens, and large-scale catering services, all of which require durable, cost-efficient, and standardized utensils. The increasing consumer preference for ergonomic, corrosion-resistant, and aesthetically refined designs has also contributed to product innovation, particularly in stainless steel and silver-plated variants. Moreover, sustainability concerns are gradually influencing demand for recyclable and long-life cutlery solutions, especially in developed markets.Serveware and decorative tabletop accessories represent a high-value and design-driven segment that is increasingly gaining traction in premium household and gifting markets. This category benefits significantly from the growing influence of home décor trends, social media-driven lifestyle aesthetics, and the rising importance of presentation in dining experiences. Urban households, particularly among middle- and high-income groups, are increasingly investing in visually appealing serveware that complements interior design themes. In the hospitality sector, luxury hotels and fine-dining establishments use serveware as a differentiator to enhance guest experience and brand positioning. The segment is also strongly supported by seasonal gifting demand during festivals, weddings, and corporate events, further reinforcing its premium positioning within the broader market.

Application Insights

Household dining remains the largest application segment in the tabletop kitchen products market, driven by continuous urbanization, evolving lifestyle patterns, and increasing consumer inclination toward aesthetic and functional dining experiences at home. The growing influence of nuclear families, coupled with rising disposable incomes and exposure to global design trends, has led to higher spending on kitchenware that blends utility with visual appeal. The demand is further reinforced by the increasing frequency of home dining occasions, weekend gatherings, and at-home entertainment culture, which encourages consumers to invest in coordinated and premium tabletop solutions.The hospitality sector represents the fastest-growing application segment, supported by the rapid expansion of hotels, restaurants, cafés, resorts, and experiential dining establishments worldwide. The surge in global tourism, business travel recovery, and lifestyle dining experiences has created sustained demand for high-quality, durable, and aesthetically differentiated tabletop products. Hospitality operators increasingly prioritize product consistency, brand alignment, and guest experience enhancement, driving large-scale procurement of customized dinnerware, drinkware, and serveware solutions. Additionally, the rise of boutique hotels and themed restaurants has further intensified demand for unique and design-centric tabletop collections that enhance brand identity.Export-driven demand continues to serve as a critical growth pillar for the global tabletop kitchen products market. Asia-based manufacturing hubs, particularly in China and India, play a dominant role in supplying cost-competitive and increasingly high-quality products to global markets. The integration of global supply chains, expansion of e-commerce exports, and growing private-label manufacturing arrangements have strengthened cross-border trade flows. This export orientation not only supports volume growth but also encourages manufacturers to align with diverse international design preferences and regulatory standards, thereby enhancing global competitiveness.

Distribution Channel Insights

Offline retail channels continue to maintain dominance in the distribution landscape, primarily due to consumer preference for physical inspection of tabletop products before purchase. Supermarkets, specialty kitchenware stores, department stores, and home décor outlets remain key touchpoints where consumers evaluate product quality, texture, weight, and design compatibility. This tactile purchasing behavior is particularly strong among older demographics and premium buyers who prioritize trust, durability, and aesthetic alignment with home interiors. Offline retail also benefits from in-store merchandising strategies, seasonal promotions, and curated product displays that influence impulse purchasing behavior.However, online retail has emerged as the fastest-growing distribution channel, fundamentally transforming purchasing behavior across global markets. The expansion of e-commerce platforms, coupled with improved logistics infrastructure and digital payment systems, has enabled seamless access to a wide range of tabletop products. Consumers are increasingly drawn to the convenience, competitive pricing, and extensive product variety offered by online channels. Direct-to-consumer (DTC) brand strategies have further strengthened this shift by allowing manufacturers to build stronger brand narratives, offer customization options, and engage directly with end users. Social commerce, influencer marketing, and visual discovery platforms are also playing an increasingly influential role in shaping purchasing decisions, particularly among younger, digitally native consumers.

End-Use Insights

Residential households account for approximately 62% of total demand, largely driven by lifestyle upgrades, home décor trends, and frequent replacement cycles. Increasing disposable income, urbanization, and the rise of nuclear families have also contributed to residential demand. The HoReCa segment is the fastest-growing end-use category, expanding at nearly 6.8% CAGR. This growth is supported by the global expansion of the hospitality sector, increased dining out trends, and rising consumer expectations for premium dining experiences in hotels and restaurants. Institutional end users, including educational facilities, hospitals, and corporate cafeterias, provide stable, volume-driven demand through standardized procurement and long-term supply contracts, further stabilizing the market.

Explore more data points, trends and opportunities Download Free Sample Report

Tabletop Kitchen Products Market Segmentations

By Product Type

- Dinnerware

- Drinkware

- Flatware & Cutlery

- Serveware

- Table Accessories

- Storage & Organization

- Premium & Decorative Tabletop Products

By Material Type

- Ceramic

- Glass

- Metal

- Plastic & Polymer

- Wood & Bamboo

- Silicone

- Composite & Sustainable Materials

By Price Range

- Economy

- Mid-Range

- Premium

- Luxury

By Distribution Channel

- Offline Retail

- Online Retail

By End Use

- Household Dining

- Hospitality Industry

- Foodservice Chains

- Corporate & Institutional Dining

- Event Management & Catering

Regional Insights

Asia Pacific

Asia Pacific dominates the global tabletop kitchen products market with approximately 39% share in 2026, making it the most influential regional contributor in both production and consumption. The region’s leadership is primarily driven by its strong manufacturing base, cost-efficient production capabilities, and rapidly expanding domestic demand. China remains the largest contributor, serving as both a global manufacturing hub and a massive consumption market fueled by urbanization, rising middle-class incomes, and evolving lifestyle preferences. India represents one of the fastest-growing markets within the region, supported by increasing disposable income, rapid expansion of organized retail, and growing penetration of e-commerce platforms in both urban and semi-urban areas. Japan and South Korea contribute significantly to the premium segment, where consumers exhibit strong preferences for high-quality, minimalist, and design-oriented tabletop products. The region’s growth is further supported by cultural emphasis on dining aesthetics, expanding hospitality infrastructure, and increasing export integration with global markets.

North America

North America accounts for approximately 24% of the global market, with the United States serving as the primary growth engine. The region’s expansion is strongly influenced by high consumer spending power, strong home décor culture, and a well-established hospitality industry. A key driver of demand is the increasing adoption of e-commerce platforms, which has reshaped retail dynamics and enabled consumers to access a wide variety of premium and niche tabletop products. Sustainability trends are particularly strong in this region, with consumers showing a growing preference for eco-friendly materials, recyclable packaging, and ethically sourced products. Additionally, the rise of home entertaining culture, fueled by lifestyle changes and increased focus on indoor social gatherings, has significantly boosted demand for aesthetically appealing dinnerware and serveware.

Europe

Europe holds around 27% share of the global market and is characterized by a strong tradition of craftsmanship, design innovation, and premium product consumption. Key markets such as Germany, France, Italy, and the United Kingdom play a central role in shaping regional demand patterns. The region is widely recognized as a hub for luxury and artisanal tabletop products, where design, heritage, and sustainability are key purchasing drivers. European consumers exhibit strong preferences for environmentally responsible production processes, including recyclable materials, reduced carbon footprints, and long-life product usage cycles. The hospitality sector in Europe is also highly developed, with a strong emphasis on fine dining experiences, boutique hotels, and culturally themed restaurants, all of which contribute to sustained demand for high-end tabletop solutions. Innovation in design, particularly through collaborations with designers and lifestyle brands, further enhances market differentiation.

Middle East & Africa

The Middle East & Africa region is experiencing strong growth driven by rapid hospitality sector expansion, luxury tourism development, and large-scale urban infrastructure projects. Countries such as the United Arab Emirates and Saudi Arabia are at the forefront of this growth, supported by high-income consumer bases and government-led diversification strategies focused on tourism and entertainment. The rise of luxury hotels, fine dining establishments, and large-scale event venues has significantly increased demand for premium tabletop products. Additionally, cultural emphasis on hospitality and large family gatherings contributes to strong domestic consumption patterns. In Africa, gradual urbanization, expansion of retail infrastructure, and increasing penetration of international hotel chains are contributing to steady market development, albeit from a lower base.

Latin America

Latin America demonstrates steady and consistent growth in the tabletop kitchen products market, led primarily by Brazil and Mexico. The region’s expansion is supported by rising urbanization, improving economic conditions, and increasing consumer exposure to global lifestyle trends. The hospitality sector is gradually expanding, particularly in tourism-driven economies, which is contributing to demand for durable and cost-effective tabletop solutions. Retail penetration is also improving, with the growth of organized retail formats and increasing adoption of online shopping platforms. Consumers in the region are gradually shifting toward aesthetically pleasing and coordinated dining sets, reflecting broader lifestyle upgrades and increasing influence of international design trends. While price sensitivity remains an important factor, there is a noticeable shift toward mid-range and premium product adoption among urban consumers.

Key Players in the Global Tabletop Kitchen Products Market

- Villeroy & Boch AG

- Arc Holdings

- Fiskars Group

- Lenox Corporation

- Lifetime Brands Inc.

- Steelite International

- Rosenthal GmbH

- Noritake Co., Limited

- Libbey Inc.

- Oneida Group

- Portmeirion Group PLC

- Churchill China PLC

- WMF Group

- Degrenne SA

- Corelle Brands