Tabletop Gaming Market Size

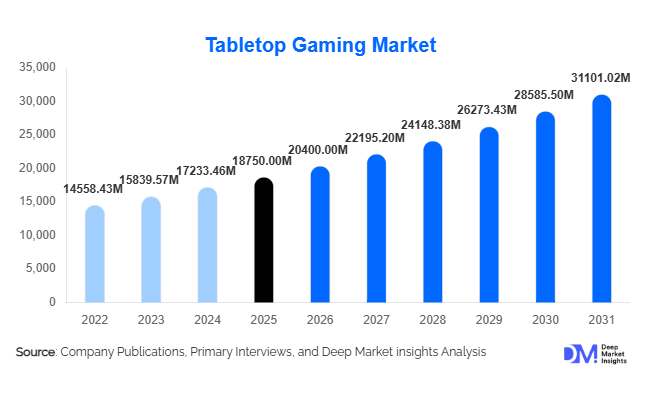

According to Deep Market Insights, the global tabletop gaming market size was valued at USD 18,750 million in 2025 and is projected to grow from USD 20,400.00 million in 2026 to reach USD 31,101.02 million by 2031, expanding at a CAGR of 8.8% during the forecast period (2026–2031). The market growth is primarily driven by the resurgence of offline social entertainment, increasing consumer preference for immersive and interactive experiences, and the growing popularity of board games, card games, and role-playing games among millennials and Gen Z consumers.

Key Market Insights

- Board games dominate the global market, accounting for approximately 42% share due to their universal appeal and accessibility across demographics.

- Online distribution channels are rapidly expanding, contributing nearly 48% of total sales driven by e-commerce growth and direct-to-consumer models.

- North America leads the global market, supported by a strong gaming culture and high consumer spending.

- Asia-Pacific is the fastest-growing region, fueled by rising disposable incomes and increasing awareness of tabletop gaming.

- Strategy-based games are gaining traction, driven by demand for intellectually engaging and immersive gameplay experiences.

- Hybrid tabletop-digital integrations, including companion apps and AR features, are reshaping user engagement and product innovation.

What are the latest trends in the tabletop gaming market?

Hybrid Digital-Physical Gaming Experiences

Tabletop gaming is transforming through the integration of digital technologies such as mobile apps, augmented reality (AR), and companion software. These hybrid experiences enhance gameplay by offering dynamic storytelling, real-time tracking, and interactive tutorials. Game developers are increasingly designing products that combine physical components with digital interfaces, making games more engaging for younger audiences. This trend also enables continuous updates and expansions without requiring entirely new physical products, improving customer retention and lifecycle value.

Rise of Community-Driven Gaming Ecosystems

The expansion of gaming cafés, hobby stores, and organized play events is fostering strong community engagement. These ecosystems provide players with opportunities to discover new games, participate in tournaments, and build social connections. Crowdfunding platforms have also empowered independent developers to launch innovative games while building loyal communities. This trend is strengthening brand loyalty and driving repeat purchases, making community engagement a key pillar of market growth.

What are the key drivers in the tabletop gaming market?

Growing Demand for Offline Social Entertainment

As digital fatigue increases, consumers are actively seeking offline, face-to-face entertainment experiences. Tabletop games provide a unique value proposition by promoting social interaction, teamwork, and strategic thinking. This shift toward experiential entertainment is significantly boosting demand across all age groups, particularly among millennials and Gen Z consumers.

Innovation in Game Design and Premiumization

Modern tabletop games feature high-quality components, intricate storytelling, and advanced gameplay mechanics. This innovation has elevated the overall gaming experience and allowed companies to introduce premium-priced products. Limited editions, expansions, and collectible items are further driving revenue growth, particularly in developed markets where consumers are willing to spend more on hobby-based entertainment.

What are the restraints for the global market?

High Cost of Premium Games

Premium tabletop games, especially miniature and role-playing games, often come with high price tags exceeding $50. This limits accessibility in price-sensitive markets and restricts adoption among casual consumers. The cost of production, including high-quality materials and detailed components, further contributes to pricing challenges.

Competition from Digital Gaming Platforms

The widespread availability of mobile, console, and PC gaming presents a significant challenge to tabletop gaming. Digital games offer convenience, scalability, and instant accessibility, which can divert consumer attention. While tabletop games offer unique social benefits, competing with the ease of digital platforms remains a key restraint.

What are the key opportunities in the tabletop gaming industry?

Expansion in Emerging Markets

Emerging economies such as India, Brazil, and Indonesia present significant growth opportunities due to rising disposable incomes and urbanization. Localization of game content and affordable pricing strategies can help companies penetrate these markets effectively. Increasing internet penetration is also supporting awareness and adoption through online communities and e-commerce platforms.

Direct-to-Consumer and Subscription Models

The rise of direct-to-consumer (DTC) sales channels is enabling companies to build stronger relationships with customers. Subscription-based models, exclusive releases, and limited-edition products are becoming popular strategies for driving recurring revenue. These models also provide valuable consumer insights, helping companies refine product offerings and marketing strategies.

Product Type Insights

Board games remain the dominant segment, accounting for approximately 42% of the global tabletop gaming market in 2025. This leadership is primarily driven by their broad demographic appeal, ease of accessibility, and continuous innovation in game design, including legacy-style gameplay, cooperative mechanics, and narrative-driven formats. The rise of family-oriented entertainment and social gaming has further reinforced demand for board games across both developed and emerging markets. Additionally, publishers are increasingly introducing localized content and themed editions, enhancing regional adoption.

Card games, particularly trading and collectible card games (TCGs/CCGs), are witnessing strong growth due to their competitive ecosystem, organized tournaments, and recurring revenue models through expansion packs. These games benefit from strong community engagement and digital tie-ins, which sustain long-term player retention. Miniature and role-playing games (RPGs) represent premium segments with higher margins, driven by dedicated hobbyists, collectors, and immersive storytelling experiences. These segments are also benefiting from crowdfunding platforms and niche publisher innovation. Accessories such as dice, tokens, playmats, and storage solutions are experiencing steady demand, supported by increasing consumer investment in personalized gaming setups and premium gaming experiences.

Application Insights

Strategy-based tabletop games lead the market with approximately 35% share in 2025, driven by increasing consumer preference for intellectually engaging and skill-based entertainment. The growing popularity of complex, replayable games among adult consumers and hobbyists has significantly contributed to this segment’s dominance. Strategy games also tend to have higher price points and longer product lifecycles, enhancing their revenue contribution.

Casual and party games continue to attract a wide consumer base, particularly for social gatherings, family entertainment, and entry-level gamers. Their simplicity, shorter playtime, and accessibility make them highly popular in emerging markets. Fantasy and thematic games are gaining traction due to their immersive storytelling, licensed content, and cross-media integration with movies, TV shows, and digital platforms. Educational games are increasingly being adopted by schools and parents as tools for cognitive development, problem-solving, and collaborative learning. This diversification of applications is expanding the market beyond traditional gaming audiences and creating new growth avenues.

Distribution Channel Insights

Online retail channels dominate the tabletop gaming market, contributing approximately 48% of total sales in 2025. This dominance is driven by the rapid expansion of e-commerce platforms, increased digital penetration, and the ability to offer a wide variety of products with global accessibility. Direct-to-consumer (DTC) models are gaining momentum, allowing publishers to improve profit margins, control branding, and engage directly with customers through exclusive releases and subscription offerings.

Offline retail channels, including specialty gaming stores, hobby shops, and supermarkets, continue to play a vital role in product discovery, customer engagement, and community building. These stores often host events, demos, and tournaments, fostering a strong local gaming ecosystem. Hybrid distribution models that combine online convenience with offline experiences are becoming increasingly popular, enabling companies to optimize reach while maintaining customer interaction and brand loyalty.

End-Use Insights

Individual consumers dominate the tabletop gaming market, accounting for nearly 68% of total demand in 2025. This dominance is driven by the growing popularity of home-based entertainment and increasing consumer interest in social and family-oriented activities. The rise of remote work and lifestyle changes has further accelerated demand for at-home gaming experiences.

Commercial establishments such as gaming cafés, board game lounges, and entertainment centers represent the fastest-growing segment, supported by the rising demand for experiential and community-driven entertainment. These venues encourage group participation and enable consumers to explore new games before purchase, driving incremental sales. Educational institutions are emerging as a promising end-use segment, integrating tabletop games into curricula to enhance critical thinking, teamwork, and problem-solving skills. This trend is particularly strong in developed markets and is gradually expanding into emerging economies.

| By Product Type | By Application | By Distribution Channel | By End-Use |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America holds the largest share of the global tabletop gaming market at approximately 38% in 2025, with the United States accounting for the majority of regional demand. The region’s dominance is driven by a well-established gaming culture, high disposable incomes, and a strong presence of leading publishers and designers. Additionally, the widespread availability of specialty gaming stores and organized gaming events supports community engagement and product adoption. The increasing popularity of premium and collector-oriented games, along with strong e-commerce infrastructure, further accelerates regional growth.

Europe

Europe accounts for around 29% of the global market, with Germany, the United Kingdom, and France serving as key demand centers. Germany’s strong heritage in board game design and manufacturing positions it as a global innovation hub, while the UK and France benefit from mature retail networks and high consumer awareness. Growth in this region is driven by increasing demand for strategy and family games, as well as a strong cultural inclination toward social and educational gaming. Additionally, sustainability trends and demand for eco-friendly products are influencing purchasing decisions, encouraging manufacturers to adopt sustainable materials and production processes.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 11% during the forecast period. Key markets such as China, Japan, South Korea, and India are driving growth due to rising disposable incomes, rapid urbanization, and increasing exposure to global gaming trends. The expansion of middle-class populations and growing youth demographics are key demand drivers. In China and India, the adoption of tabletop gaming is being supported by e-commerce growth and increasing localization of content. Japan and South Korea, with their established gaming cultures, are contributing through innovation and premium product demand. Social media influence and gaming cafés are further accelerating awareness and adoption in the region.

Latin America

Latin America holds approximately 6% of the global market, with Brazil and Mexico leading regional demand. Growth in this region is supported by expanding retail infrastructure, increasing internet penetration, and rising interest in affordable entertainment options. The growing middle class and youth population are key drivers, along with increasing exposure to global gaming trends through digital platforms. Localization strategies and cost-effective product offerings are essential for market penetration in this price-sensitive region.

Middle East & Africa

The Middle East & Africa region accounts for around 5% of the global market, with the UAE and South Africa as contributors. Growth in this region is driven by expanding premium retail sectors, increasing expatriate populations, and rising interest in leisure and entertainment activities. In the Middle East, high disposable incomes and demand for luxury and premium products are supporting market expansion. In Africa, gradual improvements in retail infrastructure and increasing urbanization are fostering market growth. The introduction of gaming cafés and community-driven initiatives is also helping to build awareness and expand the consumer base across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Tabletop Gaming Market

- Hasbro

- Mattel

- Asmodee Group

- Ravensburger

- Spin Master

- CMON Limited

- Fantasy Flight Games

- Games Workshop

- IELLO

- Kosmos

- Z-Man Games

- Indie Boards & Cards

- Rio Grande Games

- Czech Games Edition

- Alderac Entertainment Group