Synthetic Hair Wigs Market Size

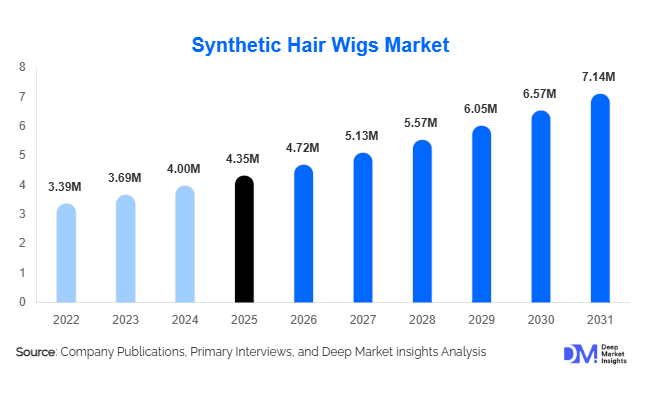

According to Deep Market Insights, the global synthetic hair wigs market size was valued at USD 4.35 billion in 2025 and is projected to grow from USD 4.71 billion in 2026 to reach USD 7.15 billion by 2031, expanding at a CAGR of 8.6% during the forecast period (2026–2031). The synthetic hair wigs market growth is primarily driven by increasing beauty consciousness, rising prevalence of hair loss disorders, rapid growth in online beauty retail, and continuous innovation in heat-resistant and natural-looking synthetic fibers. Growing adoption of wigs as fashion accessories rather than solely medical products is further accelerating market penetration across both developed and emerging economies.

Key Market Insights

- Synthetic wigs are increasingly being adopted as mainstream fashion products, particularly among younger consumers influenced by social media and celebrity styling trends.

- Medical applications are rapidly expanding, driven by increasing cases of alopecia, chemotherapy-related hair loss, and scalp sensitivity disorders.

- North America dominates the global synthetic hair wigs market due to strong beauty spending and high consumer awareness.

- Asia-Pacific remains the fastest-growing regional market, supported by urbanization, expanding e-commerce penetration, and rising disposable incomes.

- Online retail channels are transforming distribution dynamics, enabling direct-to-consumer business models and influencer-led product marketing.

- Advanced fiber technologies, including heat-resistant and lightweight synthetic materials, are reshaping premium product demand globally.

Synthetic Hair Wigs Market Trends

Premium Heat-Resistant Synthetic Fibers Gaining Popularity

The synthetic hair wigs industry is increasingly shifting toward premium heat-resistant fibers that closely replicate the appearance and texture of natural human hair. Consumers are demanding styling flexibility that allows curling, straightening, and long-term wear without compromising durability. Manufacturers are responding by investing in advanced fiber engineering technologies such as Kanekalon and Toyokalon blends, which improve softness, reduce tangling, and increase realism. Premium synthetic wigs are now bridging the quality gap between synthetic and human hair products while maintaining affordability. This trend is particularly strong in North America, Japan, South Korea, and Europe, where consumers prioritize aesthetics, comfort, and long-lasting performance.

Digital and Influencer-Led Wig Commerce

Social media platforms such as TikTok, Instagram, and YouTube are significantly influencing purchasing behavior within the synthetic hair wigs market. Beauty influencers, hairstylists, and celebrities are driving awareness regarding protective hairstyling, fashion experimentation, and color customization through wigs. E-commerce brands are increasingly leveraging live-stream shopping, virtual try-on applications, AI-based style recommendations, and direct-to-consumer websites to improve engagement and conversion rates. Online marketplaces are enabling smaller brands to expand globally while reducing dependence on traditional retail infrastructure. Personalized wig recommendations and subscription-based replacement services are also emerging as high-growth digital retail trends.

Synthetic Hair Wigs Market Drivers

Rising Prevalence of Hair Loss Disorders

One of the major growth drivers for the synthetic hair wigs market is the increasing incidence of hair loss conditions globally. Alopecia, chemotherapy-induced hair loss, hormonal imbalances, stress-related hair thinning, and age-related hair reduction are significantly contributing to sustained demand for wigs and hair systems. Synthetic wigs offer a cost-effective alternative to human hair wigs while requiring lower maintenance. Medical institutions and oncology support organizations are increasingly partnering with wig suppliers to improve accessibility for patients experiencing temporary or permanent hair loss. This trend is especially prominent across North America, Europe, Japan, and South Korea.

Growing Fashion and Beauty Consciousness

The transformation of wigs into mainstream beauty and fashion products is strongly accelerating market growth. Consumers increasingly utilize synthetic wigs for protective hairstyling, color experimentation, convenience, and appearance enhancement. Celebrity endorsements, entertainment culture, cosplay trends, and social media beauty tutorials have normalized everyday wig usage among younger demographics. The popularity of lace front wigs, vibrant color styles, and customizable textures continues to expand the consumer base. Rising disposable income and growing spending on personal grooming products in emerging economies are further supporting adoption rates.

Synthetic Hair Wigs Market Restraints

Fluctuating Raw Material Costs

Synthetic hair wigs rely heavily on petrochemical-derived fibers such as acrylic, polyester, and specialized synthetic compounds. Volatility in crude oil prices and disruptions in petrochemical supply chains can significantly impact manufacturing costs and profit margins. Smaller manufacturers often struggle to maintain pricing stability during periods of raw material inflation, leading to reduced competitiveness and operational pressure. Freight cost fluctuations and international trade disruptions further contribute to pricing instability across the supply chain.

Perception Gap Compared to Human Hair Wigs

Despite significant advancements in fiber technologies, some consumers continue to perceive synthetic wigs as less natural and less durable than human hair alternatives. Lower-cost products may still exhibit excessive shine, reduced heat tolerance, and shorter lifespans, which can negatively impact customer satisfaction. Counterfeit and low-quality imports in price-sensitive markets also affect brand trust and overall industry reputation. Overcoming these quality perception challenges remains important for long-term premium segment expansion.

Synthetic Hair Wigs Market Opportunities

Expansion of Medical Wig Solutions

The increasing prevalence of cancer treatments, alopecia, and scalp-related conditions presents significant opportunities for synthetic wig manufacturers. Healthcare providers and support organizations are increasingly recognizing wigs as part of emotional and cosmetic rehabilitation for patients experiencing hair loss. Companies that develop lightweight, hypoallergenic, breathable, and medically certified synthetic wigs are expected to gain strong market traction. Insurance reimbursement programs in some developed countries are also improving affordability for medical users, creating additional growth potential for specialized product categories.

Growth of Sustainable and Eco-Friendly Synthetic Fibers

Sustainability is becoming an important purchasing consideration among beauty consumers. Manufacturers investing in recyclable fibers, low-emission production methods, and bio-based synthetic materials are likely to strengthen their competitive positioning. Consumers are increasingly seeking reusable and long-lasting wigs that reduce environmental impact without compromising aesthetics. Sustainable packaging solutions and ethical manufacturing practices are also becoming key brand differentiators. This trend is expected to create premiumization opportunities while aligning with broader environmental goals across the beauty and personal care industry.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.35 Million |

| Market Size in 2026 | USD 4.72 Million |

| Market Size in 2031 | USD 7.14 Million |

| CAGR | 8.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Full cap synthetic wigs dominate the market, accounting for nearly 38% of total global revenues in 2025. Their leadership is supported by broad applicability across fashion, medical, and entertainment uses. Lace front synthetic wigs are particularly popular because they offer realistic hairlines and styling flexibility while remaining more affordable than human hair alternatives. Partial hairpieces and synthetic extensions are also experiencing rapid demand growth due to increasing consumer preference for lightweight and temporary styling solutions. Costume and cosplay wigs continue to expand steadily, supported by entertainment industries, gaming culture, anime conventions, and digital content creation trends globally.

Fiber Material Insights

Kanekalon fiber wigs account for approximately 34% of global demand due to their softness, durability, heat tolerance, and natural appearance. Premium wig manufacturers increasingly utilize Kanekalon-based fibers for mid-range and premium product categories. Toyokalon fibers are also gaining traction because of their lightweight properties and styling flexibility. Heat-resistant synthetic fibers represent one of the fastest-growing categories as consumers seek products compatible with curling and straightening tools. Blended synthetic fibers are becoming increasingly common as manufacturers aim to balance affordability with premium aesthetics and durability.

Distribution Channel Insights

Online retail channels account for nearly 46% of global synthetic hair wig sales and continue to gain market share rapidly. E-commerce platforms, brand-owned websites, and social commerce channels are reshaping purchasing behavior by enabling broader product access, influencer-led promotions, and price transparency. Digital-native wig brands are increasingly leveraging AI-powered virtual try-on tools, targeted advertising, and direct-to-consumer business models to improve profitability and customer retention. Offline retail, including wig boutiques, beauty supply stores, salons, and department stores, remains important for consumers seeking in-person consultations and product fitting services.

End-User Insights

Women remain the largest consumer segment in the synthetic hair wigs market, accounting for more than 72% of total demand globally. Female consumers primarily drive purchases related to fashion styling, protective hairstyling, beauty enhancement, and medical applications. Men’s hair systems are among the fastest-growing categories due to increasing awareness regarding male grooming and hair restoration aesthetics. Medical users, including chemotherapy and alopecia patients, continue to represent a steadily growing segment supported by rising healthcare awareness and emotional wellness initiatives. Entertainment and media professionals also contribute significantly to premium wig demand, particularly in film production, cosplay, theater, and social media content creation industries.

Application Insights

Fashion and beauty applications remain the dominant segment in the synthetic hair wigs market, supported by evolving beauty standards, social media trends, and increasing adoption of wigs for everyday styling. Hair loss treatment support represents one of the fastest-growing applications as synthetic wigs become more realistic, comfortable, and affordable for medical users. Entertainment and cosplay applications are expanding steadily due to rising popularity of anime, gaming culture, film production, and K-pop-inspired styling trends. Religious and cultural usage also contributes to stable demand across specific geographic regions and demographic groups.

Explore more data points, trends and opportunities Download Free Sample Report

Synthetic Hair Wigs Market Segmentations

By Product Type

- Full Cap Synthetic Wigs

- Partial Hairpieces

- Hair Extensions

- Fashion & Costume Wigs

- Medical Synthetic Wigs

- Men’s Hair Systems

By Fiber Material

- Kanekalon Fiber Wigs

- Toyokalon Fiber Wigs

- Heat-Resistant Synthetic Fibers

- Polyester & Acrylic Fibers

- Blended Synthetic Fibers

By Cap Construction

- Lace Front Caps

- Full Lace Caps

- Monofilament Caps

- Basic Cap Construction

- Hybrid Caps

By Distribution Channel

- Online Retail (E-commerce, D2C Websites, Social Commerce)

- Specialty Wig Stores

- Beauty Supply Stores

- Salons & Professional Studios

- Department & Retail Stores

By End User

- Women

- Men

- Children

- Medical Patients

- Entertainment & Cosplay Industry

Regional Insights

North America

North America accounted for approximately 33% of the global synthetic hair wigs market in 2025, making it the largest regional market. The United States dominates regional demand due to strong beauty spending, advanced e-commerce infrastructure, and high awareness regarding alopecia and medical hair loss conditions. African-American consumers contribute significantly to wig and extension demand through protective hairstyling practices and fashion-driven adoption. Canada also represents a stable growth market due to rising multicultural beauty trends and increasing demand for medical wigs.

Europe

Europe represents nearly 22% of global synthetic hair wig demand, with the United Kingdom, Germany, France, and Italy serving as key markets. European consumers increasingly prefer premium synthetic wigs with breathable cap construction and hypoallergenic materials. Rising demand for fashion-oriented styling products and medical wigs is supporting steady regional growth. Sustainability and ethical sourcing are becoming increasingly important purchasing considerations among European consumers, encouraging manufacturers to adopt environmentally friendly production methods.

Asia-Pacific

Asia-Pacific held nearly 31% of global market share in 2025 and is projected to remain the fastest-growing region during the forecast period. China serves as the largest manufacturing hub globally due to strong export capabilities, integrated textile ecosystems, and cost-efficient production infrastructure. Japan and South Korea drive premium demand through advanced beauty culture and entertainment industries. India is emerging as a major growth market due to rapid urbanization, rising disposable income, expanding salon networks, and increasing social media influence on beauty trends. Southeast Asia is also witnessing strong online sales growth through social commerce platforms.

Latin America

Latin America represents a steadily growing market led primarily by Brazil and Mexico. Brazil’s strong beauty culture and high spending on personal grooming products support consistent synthetic wig demand. Online beauty retail and influencer-driven marketing are accelerating adoption among younger consumers. Mexico and Argentina are also experiencing rising demand for affordable fashion wigs and synthetic extensions through e-commerce platforms.

Middle East & Africa

The Middle East and Africa region is witnessing robust growth supported by rising beauty spending, urbanization, and expanding salon networks. Gulf countries such as the UAE and Saudi Arabia are generating increasing demand for premium synthetic wigs and luxury styling products. African markets, particularly South Africa and Nigeria, remain major consumers of textured synthetic wigs and extensions due to strong adoption of protective hairstyling practices. Increasing local retail expansion and online accessibility are supporting further regional market penetration.

Key Players in the Synthetic Hair Wigs Market

- Aderans Co., Ltd.

- Artnature Inc.

- Henan Rebecca Hair Products Co., Ltd.

- HairUWear Inc.

- Shake-N-Go Fashion Inc.

- Evergreen Products Group Limited

- Godrej Consumer Products Limited

- Ruimei Hair Products Co., Ltd.

- Qingdao Emeda Arts & Crafts Co., Ltd.

- JIFA Group

- Donna Bella Hair

- Paula Young

- Outre Hair

- Janet Collection

- Sensationnel