Swimming Gear Market Size

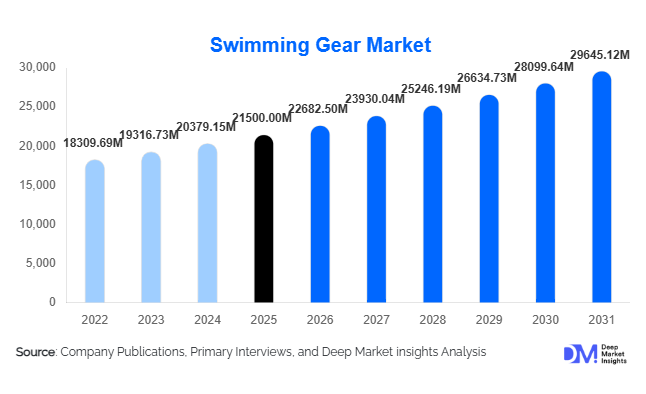

According to Deep Market Insights, the global swimming gear market size was valued at USD 21,500 million in 2025 and is projected to grow from USD 22,682.50 million in 2026 to reach USD 29,645.12 million by 2031, expanding at a CAGR of 5.5% during the forecast period (2026–2031). The swimming gear market growth is primarily driven by increasing participation in aquatic fitness activities, rising investments in sports infrastructure, and the growing popularity of recreational swimming across both developed and emerging economies. Additionally, the integration of advanced materials and smart technologies into swimwear and accessories is further enhancing product appeal and driving premiumization within the market.

Key Market Insights

- Swimming gear demand is increasingly driven by fitness and wellness trends, with swimming recognized as a low-impact, full-body exercise suitable for all age groups.

- Technological innovation in swimwear and accessories is accelerating, with smart goggles, performance-enhancing fabrics, and wearable tracking devices gaining traction.

- North America dominates the global market, supported by strong consumer spending and advanced sports infrastructure.

- Asia-Pacific is the fastest-growing region, driven by rising middle-class income, urbanization, and government-backed sports initiatives.

- Sustainability is emerging as a key differentiator, with increasing adoption of recycled fabrics and eco-friendly manufacturing processes.

- E-commerce channels are rapidly expanding, enabling global brands to penetrate emerging markets and offer wider product accessibility.

What are the latest trends in the swimming gear market?

Shift Toward Sustainable and Eco-Friendly Swimwear

Manufacturers are increasingly focusing on sustainability by introducing swimwear made from recycled materials such as ocean plastics and regenerated nylon. This trend is particularly strong in Europe and North America, where consumers are highly conscious of environmental impact. Brands are also adopting eco-friendly production processes, including reduced water usage and biodegradable packaging. Sustainability is not only a regulatory requirement in some regions but also a key factor influencing purchasing decisions, especially among younger consumers.

Rise of Smart Swimming Gear and Wearables

The adoption of smart swimming gear is transforming the market landscape. Products such as smart goggles with real-time performance metrics, lap tracking, and augmented reality displays are gaining popularity among professional athletes and fitness enthusiasts. Wearable swim trackers integrated with mobile applications provide insights into stroke efficiency, speed, and calorie burn. This technological evolution is enabling companies to differentiate their offerings and cater to a tech-savvy consumer base seeking data-driven fitness solutions.

What are the key drivers in the swimming gear market?

Growing Participation in Fitness and Recreational Swimming

The increasing awareness of health and fitness is a major driver of the swimming gear market. Swimming is widely promoted as a low-impact exercise that improves cardiovascular health, flexibility, and endurance. Urban populations, in particular, are adopting swimming as part of their regular fitness routines, leading to sustained demand for swimwear and accessories. The expansion of fitness clubs and swimming pools further supports this trend.

Expansion of Sports Infrastructure and Government Initiatives

Governments across the globe are investing heavily in sports infrastructure, including public swimming pools and training centers. Initiatives aimed at promoting sports participation, especially among youth, are boosting demand for swimming gear. School-level swimming programs and professional training facilities are contributing to consistent institutional demand, ensuring steady market growth.

Technological Advancements in Materials and Design

Continuous innovation in materials, such as chlorine-resistant fabrics and hydrodynamic designs, is enhancing product performance and durability. Advanced swimwear designed to reduce drag and improve speed is widely adopted by competitive swimmers. These innovations are not only improving user experience but also enabling manufacturers to command premium pricing, thereby increasing revenue potential.

What are the restraints for the global market?

Seasonal Demand Fluctuations

The swimming gear market is highly seasonal, particularly in regions with colder climates. Demand peaks during the summer months and declines significantly during off-seasons, leading to inconsistent revenue streams for manufacturers and retailers. This seasonality poses challenges in inventory management and production planning.

High Cost of Advanced and Premium Products

Premium swimwear and smart swimming gear often come with high price tags, limiting their adoption among price-sensitive consumers. Developing markets, in particular, face affordability challenges, which restrict market penetration. Additionally, the presence of low-cost counterfeit products intensifies competition and impacts brand profitability.

What are the key opportunities in the swimming gear industry?

Expansion in Emerging Markets

Emerging economies such as India, Brazil, and Southeast Asian countries present significant growth opportunities due to increasing investments in sports infrastructure and rising disposable incomes. The growing middle-class population in these regions is driving demand for both recreational and fitness-oriented swimming gear, creating a large untapped market for global players.

Integration of Smart Technologies

The incorporation of IoT and wearable technology into swimming gear offers substantial growth potential. Smart goggles, fitness trackers, and connected swimwear are opening new revenue streams and attracting tech-savvy consumers. Companies investing in innovation and digital ecosystems can gain a competitive edge and improve customer engagement.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 21500 Million |

| Market Size in 2026 | USD 22682.50 Million |

| Market Size in 2031 | USD 29645.12 Million |

| CAGR | 5.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Swimwear continues to dominate the global swimming gear market, accounting for approximately 38% of the total market share in 2025. The segment’s leadership is primarily driven by its essential nature across all user categories, recreational, professional, and institutional, along with a relatively high replacement cycle due to wear and tear from chlorine exposure and frequent usage. Continuous innovation in fabric technology, including chlorine-resistant, UV-protective, and compression-based materials, has further strengthened demand, particularly in the premium segment. Additionally, the growing influence of fashion trends and athleisure has expanded swimwear usage beyond pools and beaches into lifestyle applications.

Swimming accessories, including goggles, caps, earplugs, and nose clips, represent a significant secondary segment, supported by their necessity in both training and leisure swimming. The segment benefits from high-volume sales and relatively low unit costs, making it accessible across all consumer segments. Training equipment such as kickboards, pull buoys, and hand paddles is witnessing steady growth, driven by the increasing adoption of structured swimming programs in schools, fitness centers, and professional training institutions. Meanwhile, safety equipment and smart swimming gear are emerging as high-growth segments. Smart gear, in particular, is gaining traction due to technological advancements such as real-time performance tracking and augmented reality features, enabling manufacturers to target premium consumers and differentiate their offerings.

Application Insights

Fitness and wellness swimming is the leading application segment, contributing nearly 40% of the global market share. This dominance is driven by the growing recognition of swimming as a low-impact, full-body workout that improves cardiovascular health, flexibility, and endurance. Increasing urbanization, rising disposable incomes, and the expansion of fitness clubs and aquatic centers have further accelerated participation in swimming as a regular exercise routine. The demand in this segment is also supported by the growing elderly population, which prefers swimming due to its low injury risk.

Competitive swimming remains a key segment, supported by professional athletes, sports federations, and international competitions. This segment drives innovation in high-performance swimwear and advanced training equipment. Leisure and tourism-based swimming is also expanding rapidly, particularly in resort destinations and coastal regions, where demand for swimwear and accessories is fueled by the hospitality sector. Additionally, emerging applications in rehabilitation and therapy are gaining importance, as swimming is increasingly used in physiotherapy and recovery programs. This diversification of applications is broadening the market scope and creating new revenue streams for manufacturers.

Distribution Channel Insights

Offline retail channels dominate the swimming gear market with around 60% share, primarily due to consumer preference for physically evaluating products such as swimwear for fit, comfort, and material quality before purchase. Specialty sports stores, department stores, and large retail chains play a crucial role in driving sales, particularly in developed markets where brand experience and personalized assistance are valued. These stores also enable cross-selling of accessories and training equipment, enhancing overall revenue.

However, online retail is rapidly emerging as a high-growth channel, driven by increasing internet penetration, smartphone usage, and the convenience of home delivery. E-commerce platforms offer a wider product range, competitive pricing, and access to global brands, making them particularly attractive in emerging markets where offline retail infrastructure may be limited. The integration of virtual fitting tools, customer reviews, and easy return policies is further enhancing consumer confidence in online purchases. As a result, omnichannel strategies are becoming critical for market players to capture both offline and online demand effectively.

End-User Insights

Recreational users represent the largest end-user segment, accounting for approximately 45% of the market share. This segment is primarily driven by the increasing popularity of leisure swimming and fitness activities among urban populations. The rise in disposable incomes, coupled with growing awareness of health and wellness, has significantly boosted participation in recreational swimming. Additionally, the expansion of residential complexes with swimming facilities and public aquatic centers has further supported demand.

Professional athletes form a smaller but high-value segment, characterized by demand for technologically advanced and performance-oriented gear. This segment plays a crucial role in driving innovation and setting industry standards. Institutional buyers, including schools, sports clubs, hotels, and fitness centers, contribute significantly to bulk procurement, ensuring stable and recurring demand for manufacturers. The children and beginners segment is also witnessing strong growth, supported by increasing emphasis on early-age swimming education and safety awareness programs. This segment is particularly important in emerging markets, where governments are promoting swimming as a life skill.

Explore more data points, trends and opportunities Download Free Sample Report

Swimming Gear Market Segmentations

By Product Type

- Swimwear

- Swimming Accessories

- Training Equipment

- Safety Equipment

- Footwear

- Smart Swimming Gear

By Application

- Fitness and Wellness Swimming

- Competitive Swimming

- Leisure and Tourism-Based Swimming

- Water Sports and Adventure Activities

- Rehabilitation and Therapy

By Distribution Channel

- Online Retail

- Specialty Sports Stores

- Supermarkets and Hypermarkets

- Department Stores

- Direct Institutional Sales

By End User

- Recreational Users

- Professional Athletes

- Children and Beginners

- Institutional Buyers

Regional Insights

North America

North America holds approximately 30% of the global swimming gear market share in 2025, making it the leading regional market. The United States dominates demand due to its well-established sports culture, high participation in competitive and recreational swimming, and strong consumer spending on premium products. The presence of advanced sports infrastructure, including Olympic-standard training facilities and widespread access to public and private swimming pools, further supports market growth. Additionally, increasing adoption of fitness-oriented lifestyles and demand for technologically advanced swimming gear are key drivers. Canada also contributes significantly, driven by a strong emphasis on physical fitness and government-supported community sports programs.

Asia-Pacific

Asia-Pacific accounts for around 28% of the market share and is the fastest-growing region, with a projected CAGR exceeding 6.5%. Growth in this region is driven by rapid urbanization, rising disposable incomes, and increasing government investments in sports infrastructure. China leads both production and consumption, supported by its strong manufacturing base and growing middle-class population. India is emerging as a high-growth market due to initiatives promoting sports participation, expanding urban infrastructure, and increasing awareness of swimming as a fitness activity. Japan and Australia are mature markets with strong swimming cultures, high participation rates, and demand for premium products. Additionally, the expansion of tourism and hospitality sectors across Southeast Asia is further boosting demand for swimming gear.

Europe

Europe represents approximately 25% of the global market, with countries such as Germany, the UK, and France leading demand. The region’s growth is primarily driven by high awareness of health and fitness, widespread participation in aquatic sports, and strong regulatory support for sustainable products. European consumers are increasingly adopting eco-friendly swimwear made from recycled materials, reflecting a broader shift toward sustainability. The presence of established brands and a well-developed retail network further supports market expansion. Additionally, government initiatives promoting sports and physical activity across the European Union are contributing to steady demand.

Latin America

Latin America holds a smaller share of around 7%, with Brazil and Mexico being key contributors. The region’s growth is largely driven by its extensive coastline, favorable climate, and strong culture of water-based activities. Coastal tourism plays a significant role in driving demand for swimwear and accessories, particularly in Brazil, which has a well-established beach culture. Increasing investments in sports infrastructure and rising participation in water sports are also supporting market growth. However, economic volatility and price sensitivity remain key challenges in this region.

Middle East & Africa

The Middle East & Africa region is an emerging market, characterized by growing investments in luxury tourism, hospitality, and sports infrastructure. Countries such as the UAE and Saudi Arabia are investing heavily in recreational facilities, including swimming pools and water parks, to boost tourism and improve the quality of life. This is driving demand for premium swimming gear, particularly in the hospitality sector. South Africa is another key market, supported by its established sports culture and growing participation in swimming. Additionally, rising awareness of water safety and increasing urbanization across parts of Africa are contributing to gradual market expansion.