Sweat Pad Market Size

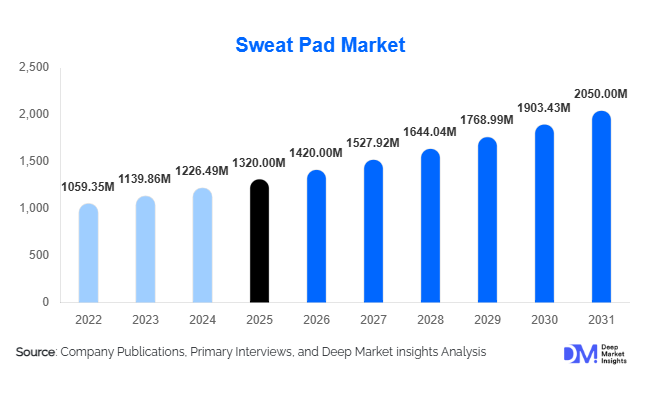

According to Deep Market Insights, the global sweat pad market size was valued at USD 1,320 million in 2025 and is projected to grow from USD 1,420 million in 2026 to reach USD 2,050 million by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The sweat pad market growth is primarily driven by increasing awareness of personal hygiene, rising participation in fitness and outdoor activities, and growing demand for discreet and convenient sweat management solutions across both developed and emerging economies.

Key Market Insights

- Rising hygiene awareness and lifestyle changes are driving the adoption of sweat pads across urban populations globally.

- Disposable sweat pads dominate the market, accounting for over 60% share due to convenience and hygiene benefits.

- North America leads the global market, supported by high consumer awareness and strong purchasing power.

- Asia-Pacific is the fastest-growing region, driven by urbanization, rising incomes, and expanding retail penetration.

- Online retail channels are rapidly expanding, contributing significantly to global sales growth.

- Sustainability trends are encouraging reusable and eco-friendly product innovations, especially in Europe and developed markets.

What are the latest trends in the sweat pad market?

Shift Toward Sustainable and Reusable Sweat Pads

Consumers are increasingly favoring eco-friendly alternatives such as reusable and biodegradable sweat pads. Growing environmental awareness is pushing manufacturers to develop products made from bamboo fibers, organic cotton, and recyclable materials. This trend is particularly strong in Europe and North America, where sustainability plays a central role in purchasing decisions. Brands are also incorporating circular economy models, offering washable and long-lasting products that reduce waste generation. This shift is enabling premium pricing strategies and strengthening brand loyalty among environmentally conscious consumers.

Integration of Advanced Materials and Functional Features

Technological advancements in materials are transforming sweat pads into high-performance hygiene products. Features such as antibacterial coatings, odor-neutralizing layers, and moisture-wicking fabrics are becoming standard in premium offerings. Innovations in ultra-thin and invisible designs are also enhancing user comfort and aesthetic appeal, particularly for professional and daily wear. Additionally, integration with apparel, such as garment-embedded sweat pads, is emerging as a new trend, especially in sportswear and formal clothing segments.

What are the key drivers in the sweat pad market?

Growing Awareness of Personal Hygiene and Grooming

Increasing awareness regarding personal hygiene and body odor management is a major driver for the sweat pad market. Consumers are becoming more conscious of their appearance and comfort, especially in professional and social settings. Sweat pads offer a discreet and effective solution, driving widespread adoption across both men and women.

Expansion of Fitness and Sports Activities

The global surge in fitness awareness and participation in sports activities has significantly increased demand for sweat management products. Sweat pads are widely used by athletes and fitness enthusiasts to enhance comfort and performance, making the sports segment a key growth driver.

Growth of E-commerce and Digital Retail

The rapid expansion of e-commerce platforms has improved product accessibility and visibility. Online channels allow consumers to explore a wide range of products, compare prices, and access reviews, leading to higher adoption rates. Direct-to-consumer models are also enabling brands to reach global audiences efficiently.

What are the restraints for the global market?

Availability of Alternative Products

The presence of substitutes such as antiperspirants, deodorants, and sweat-resistant clothing limits the demand for sweat pads. These alternatives are often more familiar to consumers, particularly in price-sensitive markets, posing a challenge to market expansion.

Limited Awareness in Developing Regions

Despite strong growth in urban areas, the lack of awareness in rural and underdeveloped regions remains a key restraint. Cultural factors and limited product exposure hinder adoption, especially in parts of Asia, Africa, and Latin America.

What are the key opportunities in the sweat pad industry?

Expansion into Emerging Markets

Emerging economies in Asia-Pacific, Latin America, and Africa present significant growth opportunities due to rising urbanization, increasing disposable incomes, and improving hygiene awareness. Early market entry and localized product strategies can help companies establish strong footholds in these regions.

Product Innovation and Smart Textile Integration

Advancements in smart textiles and material science offer opportunities to develop high-performance sweat pads with enhanced functionality. Features such as antimicrobial properties, odor control, and moisture regulation are attracting consumers seeking premium products. Integration with apparel also opens new application areas, particularly in sportswear and professional clothing.

Sustainability-Driven Premium Segments

The growing demand for eco-friendly products is creating a niche but high-value segment. Companies investing in biodegradable materials and reusable designs can differentiate themselves and capture premium market share while aligning with global sustainability goals.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1320 Million |

| Market Size in 2026 | USD 1420 Million |

| Market Size in 2031 | USD 2050 Million |

| CAGR | 7.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Disposable sweat pads dominate the market, accounting for approximately 62% of the global market share in 2025. This dominance is primarily driven by their convenience, single-use hygiene benefits, and wide availability across both online and offline retail channels. Consumers, particularly in urban environments, prefer disposable options due to their ease of use and minimal maintenance requirements, making them ideal for daily professional and active lifestyles. Additionally, affordability and bulk purchasing options further strengthen their market position.

Reusable sweat pads, while currently holding a smaller share, are gaining significant traction, especially in environmentally conscious markets such as Europe and parts of North America. The growth of this segment is driven by increasing awareness of sustainability, long-term cost savings, and rising demand for eco-friendly personal care products. Innovations in washable materials and durability are expected to further accelerate adoption in the coming years.

Material Type Insights

Non-woven fabric-based sweat pads lead the market with around 35% share, supported by their superior absorbency, lightweight structure, and cost-effectiveness. These materials are widely used in mass-market products due to their scalability in manufacturing and ability to provide consistent performance at lower price points. The segment’s leadership is also reinforced by strong demand from emerging markets, where affordability is a key purchasing factor.

Meanwhile, cotton-based and bamboo fiber-based sweat pads are gaining momentum in premium segments. Their growth is driven by increasing consumer preference for skin-friendly, hypoallergenic, and breathable materials. Bamboo fiber, in particular, is witnessing rising adoption due to its natural antibacterial properties and alignment with sustainability trends, making it highly attractive in developed markets.

Application Insights

Underarm sweat pads dominate the market, accounting for nearly 68% of the global share, as underarm perspiration remains the most common and visible concern among consumers. The segment’s growth is driven by increasing workplace grooming standards, fashion consciousness, and the need to prevent sweat stains on formal and casual clothing. This segment benefits from universal applicability across genders and age groups, making it the most commercially scalable category. Other applications, such as foot, facial, and sports-specific sweat pads, are emerging steadily, particularly in niche markets. Growth in these segments is driven by rising participation in sports and fitness activities, as well as increasing demand for targeted sweat management solutions in specialized use cases.

Attachment Type Insights

Adhesive sweat pads dominate the market with approximately 70% market share, owing to their ease of application, versatility, and compatibility with a wide range of clothing types. The segment’s leadership is supported by consumer preference for discreet, secure, and hassle-free solutions that do not require additional accessories or adjustments. Garment-integrated sweat pads are emerging as a premium and innovative segment, particularly in sportswear and formal apparel. This growth is driven by increasing collaboration between apparel manufacturers and hygiene product companies, enabling seamless integration of sweat-absorbing technologies into clothing. This trend is expected to gain traction as consumers seek more permanent and aesthetically integrated solutions.

End User Insights

Women represent the largest consumer segment, accounting for around 55% of the global market. This dominance is driven by higher adoption of personal care and grooming products, as well as greater awareness of hygiene and appearance-related concerns. Women are also more likely to adopt preventive solutions such as sweat pads in professional and social settings. However, the men’s segment is witnessing steady growth, supported by increasing awareness of grooming, rising participation in fitness activities, and the growing influence of personal care marketing targeted toward male consumers. The unisex segment is also expanding, particularly with the introduction of gender-neutral product designs.

Distribution Channel Insights

Online retail channels account for approximately 38% of total sales and represent the fastest-growing segment in the sweat pad market. The growth of this channel is driven by increasing internet penetration, convenience, wider product availability, and the ability to compare prices and reviews. Direct-to-consumer (DTC) strategies and subscription-based purchasing models are further enhancing customer retention and repeat purchases. Offline channels, including pharmacies, supermarkets, and specialty stores, continue to play a significant role, particularly in regions where consumers prefer physical product evaluation before purchase. However, the shift toward digital platforms is expected to continue accelerating globally.

End-Use Industry Insights

The personal care and hygiene industry remains the primary end-use segment, accounting for the majority of sweat pad demand. With the global personal care industry valued at over USD 500 billion, the segment provides a strong and stable demand base. Increasing consumer focus on hygiene, grooming, and daily comfort continues to drive product adoption. The sports and fitness industry is the fastest-growing end-use segment, driven by rising health awareness, increasing gym memberships, and growing participation in outdoor and athletic activities. Sweat pads are increasingly being used to enhance comfort and performance during physical exertion. Healthcare applications are also emerging, particularly for individuals suffering from hyperhidrosis or requiring post-surgical care. Additionally, export-driven demand from Asia-Pacific to North America and Europe is playing a critical role in market expansion, supported by cost-efficient manufacturing and strong global supply chains.

Explore more data points, trends and opportunities Download Free Sample Report

Sweat Pad Market Segmentations

By Product Type

- Disposable Sweat Pads

- Reusable Sweat Pads

By Material Type

- Non-woven Fabric

- Cotton-based

- Bamboo Fiber-based

- Gel-based

- Silicone-based

- Blended/Composite Materials

By Application

- Underarm Sweat Pads

- Facial Sweat Pads

- Foot Sweat Pads

- Back & Torso Sweat Pads

- Sports-specific Sweat Pads

By End User

- Men

- Women

- Unisex

By Distribution Channel

- Online Retail

- Pharmacies & Drugstores

- Supermarkets & Hypermarkets

- Specialty Stores

Regional Insights

North America

North America accounts for approximately 32% of the global market share in 2025, making it the largest regional market. The United States dominates demand, supported by high consumer awareness, strong purchasing power, and a well-established personal care industry. Key growth drivers in the region include increasing adoption of premium hygiene products, high penetration of e-commerce platforms, and strong demand from working professionals and fitness enthusiasts. Additionally, growing interest in sustainable and reusable products is further shaping market dynamics in North America.

Asia-Pacific

Asia-Pacific holds around 29% market share and is the fastest-growing region, with a projected CAGR exceeding 9%. China and India are the primary growth engines, driven by rapid urbanization, rising disposable incomes, and expanding middle-class populations. Increasing awareness of personal hygiene, coupled with aggressive expansion of online retail platforms, is significantly boosting demand. In India, government initiatives promoting hygiene and the rapid growth of organized retail are key drivers, while China benefits from strong manufacturing capabilities and export-oriented production.

Europe

Europe accounts for approximately 24% of the market, with major demand coming from Germany, the UK, and France. The region’s growth is primarily driven by strong consumer preference for sustainable and eco-friendly products. Increasing regulatory focus on environmental compliance and material safety is encouraging the adoption of reusable and biodegradable sweat pads. Additionally, high fashion consciousness and workplace grooming standards are supporting consistent demand across the region.

Middle East & Africa

The Middle East and Africa region holds about 8% market share, with demand largely driven by hot climatic conditions that result in higher perspiration levels. Countries such as the UAE and Saudi Arabia are key contributors, supported by rising disposable incomes and increasing adoption of personal care products. Growth in organized retail and expanding e-commerce platforms is further enhancing product accessibility in the region.

Latin America

Latin America accounts for around 7% of the global market, with Brazil and Mexico leading demand. The region’s growth is driven by rising middle-class populations, improving access to personal care products, and increasing awareness of hygiene. Expansion of retail infrastructure and the growing influence of global brands are also contributing to market development, although price sensitivity remains a key factor influencing purchasing decisions.

Key Players in the Sweat Pad Market

- Procter & Gamble

- Unicharm Corporation

- Kao Corporation

- Kimberly-Clark Corporation

- Johnson & Johnson

- 3M Company

- Beiersdorf AG

- Colgate-Palmolive Company

- Edgewell Personal Care

- SweatBlock

- Perspi-Guard

- Sirona Hygiene

- Certain Dri

- Dry Idea

- Nivea