Sustainable Clothing Market Size

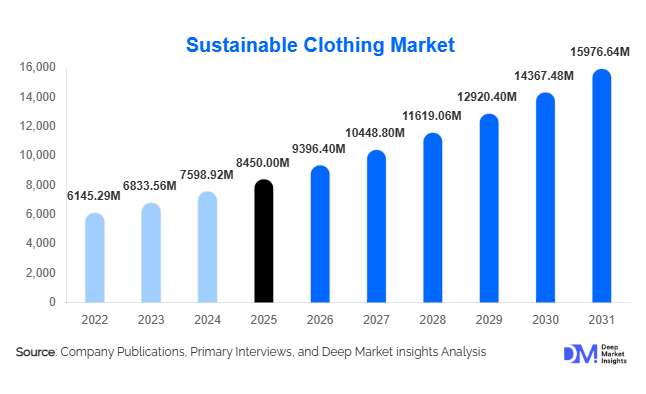

According to Deep Market Insights, the global sustainable clothing market size was valued at USD 8,450 million in 2025 and is projected to grow from USD 9,396.40 million in 2026 to reach USD 15,976.64 million by 2031, expanding at a CAGR of 11.2% during the forecast period (2026–2031). The sustainable clothing market growth is primarily driven by increasing regulatory pressure on textile waste, rising consumer demand for ethical and eco-friendly apparel, and large-scale corporate commitments toward carbon neutrality and circular fashion models.

Key Market Insights

- Mass-market sustainable apparel is expanding rapidly, making eco-friendly clothing accessible beyond premium and niche consumers.

- Organic cotton remains the dominant material segment, accounting for over 30% of total sustainable apparel revenue in 2025.

- Europe leads the global market, supported by strict environmental regulations and high ethical consumer awareness.

- Asia-Pacific is the fastest-growing region, driven by rising middle-class income and growing e-commerce penetration.

- Online retail dominates distribution, contributing more than half of total sustainable clothing sales globally.

- Technological integration in textile recycling and blockchain traceability is reshaping transparency and supply chain accountability.

What are the latest trends in the sustainable clothing market?

Circular Fashion and Textile Recycling Expansion

Circular economy integration is becoming central to sustainable clothing strategies. Brands are increasingly adopting textile-to-textile recycling technologies, take-back programs, and resale platforms to extend garment lifecycles. Chemical recycling of polyester and enzymatic fiber regeneration are scaling commercially, allowing manufacturers to reduce virgin raw material dependency. Many global apparel brands are committing to 50–100% recycled or sustainably sourced materials by 2031. Governments, particularly in Europe, are implementing Extended Producer Responsibility (EPR) frameworks, further accelerating circular adoption. The resale and refurbishment segment is also growing, indirectly strengthening demand for durable and recyclable sustainable garments.

Transparency Through Digital Traceability

Blockchain-enabled traceability, digital product passports, and QR-based transparency tools are increasingly embedded into sustainable apparel collections. Consumers are demanding visibility into sourcing, carbon footprint, and labor conditions. Brands are leveraging AI-powered supply chain analytics and digital tagging to validate sustainability claims and mitigate greenwashing risks. This technological integration is particularly appealing to Gen Z and millennial buyers who prioritize authenticity and accountability when making purchasing decisions.

What are the key drivers in the sustainable clothing market?

Regulatory and ESG Compliance Pressure

Governments across Europe and North America are tightening textile waste regulations and mandating sustainability disclosures. Corporate ESG commitments are pushing global fashion brands to reduce Scope 3 emissions, which account for the majority of apparel supply chain emissions. Compliance with sustainability benchmarks is driving procurement shifts toward certified organic, recycled, and low-impact materials.

Shifting Consumer Preferences Toward Ethical Fashion

Consumers, especially Gen Z and millennials, are willing to pay a 5–20% premium for sustainable apparel. Social media awareness, climate activism, and influencer advocacy have amplified the demand for ethical production practices. Sustainable clothing is transitioning from niche positioning to mainstream retail presence, particularly in women’s fashion and activewear.

What are the restraints for the global market?

Higher Production and Certification Costs

Sustainable raw materials such as organic cotton and recycled fibers cost 15–40% more than conventional alternatives. Certification processes, traceability investments, and sustainable dyeing technologies further increase operational expenditure, compressing manufacturer margins.

Limited Recycling Infrastructure in Emerging Markets

While demand is growing globally, recycling infrastructure and waste collection systems remain underdeveloped in many countries. This restricts circular scalability and limits raw material recovery efficiency, posing challenges to widespread adoption.

What are the key opportunities in the sustainable clothing industry?

Mass-Market Sustainable Apparel Expansion

The introduction of affordable, sustainable lines by major apparel brands presents significant growth potential. As production technologies scale and raw material sourcing improves, cost gaps between sustainable and conventional clothing are narrowing. Brands that position sustainable collections within accessible pricing tiers can capture broad consumer segments, particularly in emerging economies.

Emerging Market Urban Demand

Rapid urbanization and digital retail expansion in Asia-Pacific and Latin America create untapped opportunities. Countries such as India, Indonesia, Brazil, and Mexico are witnessing rising awareness of environmental issues. Local production partnerships and regionally adapted collections can help companies gain an early mover advantage in these high-growth markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8450 Million |

| Market Size in 2026 | USD 9396.40 Million |

| Market Size in 2031 | USD 15976.64 Million |

| CAGR | 11.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Sustainable tops and t-shirts dominate the global market, accounting for approximately 28% of the total 2025 revenue. The leadership of this segment is primarily driven by high purchase frequency, wardrobe essential status, and relatively lower price points compared to outerwear and formal apparel. Consumers often begin their sustainable fashion journey with everyday basics, making this category the most commercially scalable. In addition, brands have been able to integrate organic cotton and recycled fibers into t-shirts more easily than complex garments, accelerating product availability. Sustainable activewear is the fastest-growing product category, supported by the global athleisure trend, increased health awareness, and strong adoption of recycled polyester fabrics. Outerwear and formal sustainable apparel, while comparatively smaller, are expanding steadily due to innovation in bio-based insulation materials and premium eco-conscious fashion collections targeting high-income consumers.

Material Type Insights

Organic cotton leads the material segment with nearly 32% market share in 2025, driven by strong certification ecosystems, global cultivation networks, and high consumer familiarity. Its dominance is reinforced by regulatory support for pesticide-free farming and lower water consumption compared to conventional cotton. Major apparel brands have prioritized organic cotton sourcing to meet sustainability pledges, strengthening their leadership. Recycled polyester is the second-largest material segment, particularly dominant in activewear and sportswear due to durability, moisture-wicking performance, and a lower carbon footprint compared to virgin polyester. Regenerated cellulosic fibers such as lyocell and modal are rapidly gaining market share as they offer softness, biodegradability, and reduced environmental impact. These materials are increasingly used in premium collections, supporting their gradual revenue expansion.

Distribution Channel Insights

Online retail accounts for approximately 55% of global sustainable clothing sales, making it the leading distribution channel. The primary driver of this dominance is the ability of digital platforms to communicate sustainability narratives, certifications, sourcing transparency, and environmental impact metrics directly to consumers. Brand-owned D2C platforms allow companies to maintain higher margins while controlling sustainability messaging. E-commerce marketplaces further enhance accessibility in emerging economies. Additionally, AI-powered recommendations and digital traceability tools enhance consumer trust. Offline specialty stores and department retailers continue to play a strategic role in premium and luxury sustainable segments, where tactile experience and brand immersion influence purchasing decisions.

End-User Insights

Women represent the largest consumer segment, contributing approximately 52% of global sustainable clothing revenue in 2025. The dominance of this segment is linked to higher apparel consumption rates, stronger engagement with fashion trends, and greater responsiveness to ethical and environmental messaging. Women-led fashion brands have also played a significant role in mainstreaming sustainable collections. Men’s sustainable apparel is growing at nearly 10% CAGR, supported by increasing awareness of responsible consumption and expansion of sustainable activewear lines. Kidswear is emerging as a high-potential niche segment, driven by parental preference for toxin-free, hypoallergenic, and organic fabrics, especially in developed markets.

Explore more data points, trends and opportunities Download Free Sample Report

Sustainable Clothing Market Segmentations

By Product Type

- Sustainable Tops & T-Shirts

- Sustainable Bottom Wear

- Sustainable Activewear & Sportswear

- Sustainable Outerwear

- Sustainable Intimate Wear & Loungewear

- Sustainable Formal & Occasion Wear

By Material Type

- Organic Cotton

- Recycled Polyester

- Regenerated Cellulosic Fibers (Lyocell, Modal)

- Hemp

- Recycled Wool

- Other Bio-Based & Innovative Materials

By Distribution Channel

- Online Retail

- Offline Retail

By End User

- Women

- Men

- Kids

Regional Insights

Europe

Europe leads the global sustainable clothing market, accounting for approximately 34% of total revenue in 2025. Germany, the United Kingdom, and France are the primary demand centers, with Germany alone contributing nearly 9% of global revenue. The region’s leadership is driven by stringent EU regulations on textile waste, Extended Producer Responsibility (EPR) frameworks, and aggressive carbon neutrality targets. High consumer environmental awareness, strong adoption of ethical fashion labels, and established circular economy infrastructure further reinforce market growth. Retailers across Scandinavia and Western Europe are integrating sustainability as a core brand identity, accelerating regional expansion.

North America

North America holds around 29% of the global market, with the United States contributing nearly 24%. Growth in this region is primarily driven by strong ESG commitments from major apparel corporations, high disposable income levels, and expanding D2C sustainable fashion brands. Consumer activism, climate awareness movements, and social media-driven transparency campaigns have strengthened demand for traceable and ethically produced garments. Canada also demonstrates rising adoption, particularly in premium and outdoor sustainable apparel categories, supported by environmentally conscious consumer behavior.

Asia-Pacific

Asia-Pacific accounts for approximately 25% of global revenue and is the fastest-growing region, expanding at nearly 13% CAGR. China and India are the principal growth engines. China benefits from rising urban middle-class income, domestic eco-fashion startups, and strong e-commerce ecosystems. India’s growth, exceeding 14% annually, is supported by its organic cotton production advantage and government-backed textile modernization initiatives. Increasing awareness of environmental issues among younger consumers, combined with rapid digital retail penetration, is driving demand across Southeast Asia and Australia as well.

Latin America

Latin America contributes roughly 7% of global revenue, led by Brazil and Mexico. Regional growth is driven by rising urbanization, growing social media influence on ethical fashion trends, and the expansion of regional sustainable fashion startups. Import penetration of sustainable brands from Europe and North America is also increasing, supported by improving e-commerce infrastructure. Government initiatives promoting sustainable agriculture indirectly support organic cotton-based apparel growth.

Middle East & Africa

The Middle East & Africa region accounts for approximately 5% of the global market. The UAE and South Africa are key contributors. Growth in the Middle East is fueled by high-income consumers seeking premium sustainable fashion and increasing ESG integration within luxury retail. In Africa, South Africa is emerging as a regional hub due to expanding ethical fashion startups and improving retail ecosystems. Rising awareness of sustainable consumption and international brand penetration are expected to gradually strengthen regional demand over the forecast period.