Sunscreen Stick Market Size

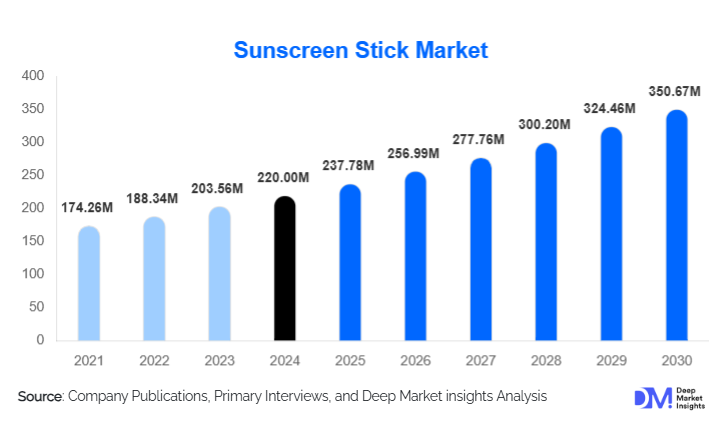

According to Deep Market Insights, the global sunscreen stick market size was valued at USD 220.00 million in 2025 and is projected to grow from USD 237.78 million in 2026 to reach USD 350.67 million by 2031, expanding at a CAGR of 8.08% during the forecast period (2026–2031). The sunscreen stick market growth is primarily driven by rising awareness of UV-induced skin damage, increasing preference for portable and mess-free sun protection formats, and growing adoption of premium and dermatologically recommended skincare products across both developed and emerging economies.

Key Market Insights

- Sunscreen sticks are increasingly preferred for facial and targeted application, driven by convenience, precision, and ease of reapplication during outdoor activities.

- Mineral-based sunscreen sticks are gaining strong traction due to regulatory scrutiny of chemical UV filters and rising demand for sensitive-skin-friendly products.

- North America dominates the global market, supported by high consumer awareness, premium pricing, and strong dermatological endorsement.

- Asia-Pacific is the fastest-growing regional market, fueled by beauty-conscious consumers, urbanization, and rising disposable incomes.

- Premium and super-premium price tiers account for a significant share, reflecting the convergence of sunscreen with skincare and cosmetic benefits.

- E-commerce and direct-to-consumer channels are expanding rapidly, reshaping distribution strategies and brand-consumer engagement.

Sunscreen Stick Market Trends

Shift Toward Mineral and Reef-Safe Formulations

One of the most prominent trends in the sunscreen stick market is the accelerating shift toward mineral-based and reef-safe formulations. Concerns around the environmental impact of chemical UV filters and their potential effects on coral reefs have led to tighter regulations in several countries. As a result, zinc oxide and titanium dioxide-based sunscreen sticks are increasingly favored by consumers, particularly those with sensitive skin, children, and environmentally conscious buyers. Brands are actively reformulating products to meet clean-label expectations, positioning mineral sunscreen sticks as safer, more sustainable alternatives.

Premiumization and Skincare Integration

Sunscreen sticks are increasingly positioned as multifunctional skincare products rather than basic sun protection solutions. New launches incorporate anti-aging actives, antioxidants, moisturizing agents, and blue-light protection, aligning sunscreen usage with daily skincare routines. This premiumization trend has significantly increased average selling prices, particularly in facial sunscreen sticks marketed for urban consumers. Packaging innovations such as refillable sticks and luxury applicators further reinforce premium brand positioning.

Sunscreen Stick Market Drivers

Rising Awareness of UV Damage and Skin Cancer Prevention

Growing awareness of the long-term effects of UV exposure, including premature aging and skin cancer, is a major driver of sunscreen stick adoption. Dermatologists increasingly recommend daily sun protection, even outside beach or vacation settings. Sunscreen sticks benefit from this shift due to their ease of use, portability, and suitability for frequent reapplication, especially on high-exposure areas such as the face, lips, and ears.

Growth in Outdoor and Sports Activities

The global rise in outdoor recreation, fitness, and sports participation has significantly boosted demand for sunscreen sticks. Sweat-resistant, high-SPF sunscreen sticks are particularly popular among athletes, hikers, swimmers, and adventure travelers who require durable and portable sun protection. This driver is especially strong in North America, Europe, and Australia, where outdoor lifestyles are deeply embedded.

Sunscreen Stick Market Restraints

Higher Product Pricing Compared to Traditional Sunscreens

Sunscreen sticks are generally priced higher on a per-unit basis than lotions and sprays due to concentrated formulations, premium packaging, and targeted use positioning. This pricing premium can limit adoption in price-sensitive markets, particularly in parts of Latin America, Africa, and Southeast Asia, where traditional sunscreen formats remain dominant.

Raw Material Price Volatility

Fluctuations in the prices of key raw materials such as zinc oxide, natural waxes, and specialty emollients pose challenges for manufacturers. Rising input costs can pressure profit margins and lead to frequent price adjustments, potentially impacting demand elasticity in mass-market segments.

Sunscreen Stick Market Opportunities

Expansion in Asia-Pacific Beauty and Skincare Markets

Asia-Pacific presents a significant growth opportunity for sunscreen stick manufacturers. Increasing beauty awareness, strong emphasis on facial skincare, and rising urban pollution levels are driving daily sunscreen usage in countries such as China, South Korea, Japan, and India. Sunscreen sticks align well with makeup routines and on-the-go lifestyles, making them particularly attractive to younger consumers in metropolitan areas.

Innovation in Sports-Specific and Child-Safe Products

There is a growing opportunity in developing sports-specific, water-resistant, and child-safe sunscreen sticks. Pediatric and sports dermatology endorsements are strengthening consumer trust in these specialized products. Additionally, innovations such as ultra-durable formulas, ergonomic designs, and refillable packaging are expected to create differentiation and support long-term market expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 220 Million |

| Market Size in 2026 | USD 237.78 Million |

| Market Size in 2031 | USD 350.67 Million |

| CAGR | 8.08% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Mineral sunscreen sticks dominate the product landscape, accounting for approximately 38% of global revenue in 2025, driven by clean-label demand and regulatory compliance. Chemical sunscreen sticks continue to hold a significant share due to lighter textures and cosmetic appeal, particularly in mass-market products. Hybrid formulations, combining mineral and chemical filters, are emerging as a fast-growing segment, offering balanced performance and broader consumer acceptance.

SPF Strength Insights

Sunscreen sticks with SPF 50 and above represent the largest segment, contributing around 42% of the 2025 market. This dominance is supported by dermatological recommendations and consumer preference for maximum protection. SPF 30–49 products remain popular for daily urban use, while lower SPF variants are increasingly limited to niche cosmetic or indoor-use applications.

Distribution Channel Insights

Online retail channels account for nearly 29% of global sunscreen stick sales, driven by direct-to-consumer strategies, subscription models, and influencer-led marketing. Pharmacies and drugstores remain critical channels, particularly for dermatologist-recommended and pediatric products. Specialty beauty stores and supermarkets continue to serve as important touchpoints for brand discovery and impulse purchases.

End-Use Insights

Adult consumers account for approximately 61% of total demand, driven by daily facial sunscreen usage. Sports and outdoor enthusiasts represent the fastest-growing end-use segment, expanding at a CAGR exceeding 11%. Children and baby care applications are also growing rapidly, supported by rising parental awareness and preference for mineral-only formulations.

Explore more data points, trends and opportunities Download Free Sample Report

Sunscreen Stick Market Segmentations

By SPF Strength

- SPF Below 15

- SPF 15–29

- SPF 30–49

- SPF 50 and Above

By Product Formulation

- Mineral (Physical) Sunscreen Sticks

- Chemical Sunscreen Sticks

- Hybrid (Mineral + Chemical) Sunscreen Sticks

By Target Consumer Group

- Adults

- Children & Babies

- Sports & Outdoor Enthusiasts

By Distribution Channel

- Supermarkets & Hypermarkets

- Pharmacies & Drugstores

- Online Retail

- Specialty Beauty Stores

Regional Insights

North America

North America leads the global sunscreen stick market with a 34% share in 2025. The United States dominates regional demand due to high awareness, premium product adoption, and strong dermatologist influence. Canada also contributes steadily, supported by outdoor lifestyle trends and regulatory emphasis on sun safety.

Europe

Europe accounts for approximately 26% of the global market, with Germany, France, and the U.K. as key contributors. Strong demand for mineral and eco-friendly formulations, combined with high skincare penetration, supports market growth across the region.

Asia-Pacific

Asia-Pacific holds around 24% of global revenue and is the fastest-growing region, with a CAGR of nearly 11.8%. China, South Korea, and Japan drive demand through beauty-focused consumption, while India is emerging as a high-growth market due to rising urban awareness and expanding middle-class incomes.

Latin America

Latin America represents a smaller but growing market, led by Brazil and Mexico. Increasing beach tourism, sports participation, and the gradual premiumization of skincare products are supporting sunscreen stick adoption.

Middle East & Africa

The Middle East & Africa market is driven by high UV exposure and growing awareness in countries such as the UAE, Saudi Arabia, and South Africa. Premium and dermatologist-backed products perform particularly well in urban centers.

Key Players in the Sunscreen Stick Market

- Beiersdorf

- L’Oréal

- Johnson & Johnson

- Shiseido

- Edgewell Personal Care

- Kao Corporation

- Amorepacific

- Unilever

- Coty

- Pierre Fabre

- Clarins

- Rohto Pharmaceutical

- ISDIN

- Blue Lizard

- Neutrogena (Brand owned by J&J)