Stuffed and Plush Toys Market Size

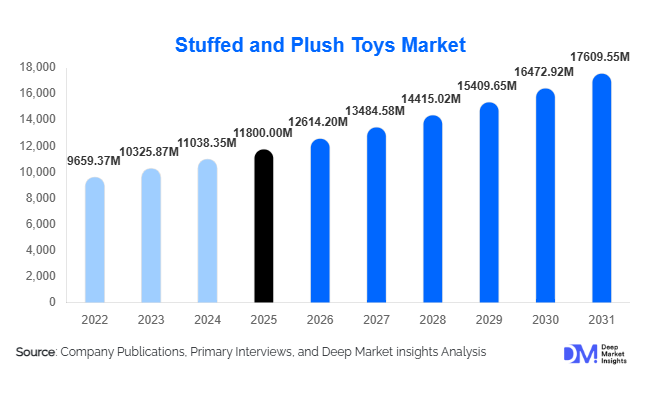

According to Deep Market Insights, the global stuffed and plush toys market size was valued at USD 11,800 million in 2025 and is projected to grow from USD 12,614.20 million in 2026 to reach USD 17,609.55 million by 2031, expanding at a CAGR of 6.9% during the forecast period (2026–2031). The market growth is primarily driven by increasing demand for licensed merchandise, rising gifting culture across global economies, and the expansion of premium and collectible plush toys. Additionally, growing e-commerce penetration and technological advancements in interactive toys are reshaping consumer engagement and product innovation.

Key Market Insights

- Licensed plush toys dominate the market, driven by strong demand for movie, gaming, and character-based merchandise.

- The mid-range pricing segment leads globally, offering a balance between affordability and quality.

- Asia-Pacific dominates production and consumption, supported by manufacturing capabilities and rising middle-class demand.

- Gifting applications account for the largest demand share, fueled by cultural and seasonal buying patterns.

- E-commerce is the fastest-growing distribution channel, enabling global accessibility and customization.

- Sustainable and eco-friendly plush toys are gaining traction, particularly in Europe and North America.

What are the latest trends in the stuffed and plush toys market?

Premiumization and Collectible Plush Toys

The market is witnessing a strong shift toward premium and collectible plush toys, particularly among adult consumers. Limited-edition releases, designer collaborations, and high-quality materials are driving demand in this segment. Consumers are increasingly viewing plush toys as lifestyle and collectible items rather than just children’s products. Brands are leveraging exclusivity and emotional appeal to command higher margins, with collectible plush toys becoming popular in fan communities and niche markets.

Integration of Smart and Interactive Features

Technological innovation is transforming traditional plush toys into interactive products. Features such as voice recognition, touch sensors, and app connectivity are being incorporated to enhance user engagement. These smart plush toys appeal to tech-savvy consumers and parents seeking educational and interactive play experiences for children. This trend is expected to accelerate as advancements in artificial intelligence and IoT continue to evolve.

What are the key drivers in the stuffed and plush toys market?

Rising Demand for Licensed Merchandise

The growing influence of global entertainment franchises has significantly boosted the demand for licensed plush toys. Characters from movies, TV shows, and gaming platforms create strong emotional connections with consumers, leading to repeat purchases and higher brand loyalty. Licensing agreements enable manufacturers to capitalize on established fan bases, ensuring consistent demand across global markets.

Expansion of E-commerce and Direct-to-Consumer Channels

The rapid growth of online retail platforms has transformed the distribution landscape for plush toys. E-commerce enables manufacturers to reach a global audience, offer personalized products, and launch exclusive collections. Direct-to-consumer strategies are also helping brands improve margins and strengthen customer relationships through targeted marketing and digital engagement.

What are the restraints for the global market?

Fluctuating Raw Material Costs

The production of plush toys heavily relies on synthetic materials such as polyester, which are subject to price fluctuations linked to petroleum markets. This volatility impacts manufacturing costs and profit margins, especially for price-sensitive segments. Manufacturers must adopt cost optimization strategies and explore alternative materials to mitigate these risks.

Intense Competition in the Low-Cost Segment

The economy segment of the plush toys market is highly fragmented, with numerous small and regional players competing on price. This leads to reduced profitability and limits differentiation opportunities. New entrants often face challenges in establishing brand identity and competing against established players in this segment.

What are the key opportunities in the stuffed and plush toys industry?

Growth in Sustainable and Eco-friendly Products

The increasing emphasis on sustainability presents a significant opportunity for market players. Consumers are becoming more conscious of environmental impact, driving demand for plush toys made from recycled and organic materials. Companies investing in eco-friendly production processes and certifications can differentiate themselves and capture premium market segments.

Expansion into Adult and Therapeutic Segments

Plush toys are increasingly being used beyond traditional children’s applications, particularly in adult and therapeutic markets. Products designed for stress relief, emotional comfort, and sensory stimulation are gaining popularity. Healthcare institutions and wellness programs are also incorporating plush toys into therapy, creating new growth avenues for manufacturers.

Product Type Insights

Licensed plush toys dominate the global market, accounting for approximately 38% of the market share in 2025, primarily driven by strong brand recognition, franchise popularity, and emotional consumer attachment to characters from movies, gaming, and television. This segment benefits from repeat purchases, collectible trends, and merchandising tie-ins, making it the key driver of product-type growth worldwide. Traditional stuffed animals continue to maintain a significant presence due to their timeless appeal and affordability, particularly among younger children and gift buyers. Interactive and educational plush toys are emerging rapidly, fueled by technological integration such as voice recognition, AI, and app connectivity, supporting both play and learning outcomes. Collectible and premium plush toys are witnessing strong growth in adult demographics, particularly in North America, Europe, and Japan, contributing to higher profit margins and brand differentiation.

Material Type Insights

Synthetic fibers continue to lead the market with a share of around 65% in 2025, attributed to their durability, cost-effectiveness, and ease of large-scale production. These materials also support the development of interactive and technologically enhanced plush toys. Natural fibers, such as cotton, wool, and bamboo blends, are increasingly preferred due to rising consumer awareness of environmental sustainability and non-toxic materials. Recycled and eco-friendly materials are emerging as a growth segment, particularly in Europe and North America, supported by government regulations, eco-certifications, and a trend toward responsible consumerism.

Distribution Channel Insights

Offline retail channels dominate the market, accounting for approximately 55% of total sales in 2025. Factors driving this dominance include tactile product evaluation, impulse purchasing, and established retail networks in urban and suburban areas. However, online retail is the fastest-growing channel, propelled by the convenience of e-commerce, wider product variety, competitive pricing, and personalization options. Brand-owned websites and marketplaces enable manufacturers to reach global consumers directly, launch exclusive collections, and integrate promotional campaigns, particularly for licensed and collectible products. Digital marketing, social media campaigns, and influencer collaborations are further accelerating online sales growth.

Age Group Insights

Children aged 6–12 years represent the largest consumer segment, contributing around 34% of the global market, driven by high engagement with interactive and licensed plush toys and frequent product usage. Infants and toddlers remain a stable segment, supported by safety-focused products and parent purchasing behavior. The adult segment, encompassing collectors and gifting consumers, is growing rapidly, particularly in North America, Europe, and Japan. Adults often purchase premium, licensed, or limited-edition plush toys, reflecting evolving consumer behavior and expanding market opportunities beyond traditional children’s demographics.

End-Use Insights

The gifting segment dominates the stuffed and plush toys market, accounting for nearly 40% of total demand. Seasonal occasions such as birthdays, festive events, and cultural holidays significantly drive sales. Personal use remains substantial, especially among children aged 6–12 years. Emerging institutional applications, including healthcare, therapy, and educational programs, are supporting market growth by leveraging plush toys’ emotional and therapeutic benefits. Hospitals, schools, and special education centers increasingly use plush toys for sensory stimulation, comfort, and developmental learning, creating new avenues for adoption and differentiation.

| By Product Type | By Material Type | By Distribution Channel | By End-Use | By Age Group |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest market share at approximately 42% in 2025. The region is driven by strong manufacturing capabilities, low production costs, and rising domestic consumption. China leads both production and export volumes, benefiting from robust manufacturing infrastructure and a growing middle-class consumer base. India is the fastest-growing market in the region, with a CAGR of around 8.5%, supported by increasing disposable incomes, urbanization, and the expansion of organized retail and e-commerce channels. Growth is further driven by a rising gifting culture, demand for licensed characters, and a growing adult collector segment. Japan maintains a steady market for premium and collectible plush toys, driven by strong consumer affinity for high-quality, branded products and technological innovations in interactive toys.

North America

North America accounts for around 25% of the global market. The United States leads demand due to high consumer spending, strong brand loyalty, and preference for licensed and collectible plush toys. Market growth is fueled by technological innovation in interactive plush toys, integration of educational features, and the expansion of e-commerce channels. The adult collector and gifting segments further support demand, while promotional tie-ins with media franchises continue to drive licensed toy sales. Canada also contributes through premiumization trends and the adoption of eco-friendly materials.

Europe

Europe represents approximately 20% of the global market, driven by consumer preference for high-quality, safe, and eco-friendly plush toys. Germany, the UK, and France are key markets, supported by stringent regulatory frameworks for toy safety and sustainability. Growth is propelled by rising adoption of natural and recycled materials, a mature gifting culture, and strong demand for licensed characters. Technological adoption, particularly in interactive and educational toys, is also increasing. Consumers’ environmental consciousness encourages brands to offer sustainable options, providing a competitive edge in the region.

Latin America

Latin America accounts for around 7% of the global market, with Brazil and Mexico driving growth. Rising urbanization, expanding retail networks, and increasing disposable incomes support market development. Growth is particularly notable in licensed and collectible plush toys, fueled by youth engagement with entertainment franchises and the expansion of e-commerce. Seasonal gifting patterns and emerging middle-class consumers are key drivers for market penetration in the region.

Middle East & Africa

The Middle East & Africa account for approximately 6% of the global market. In the Middle East, high-income consumers in the UAE and Saudi Arabia drive demand for premium and licensed plush toys, supported by a luxury gifting culture and disposable income. In Africa, South Africa is emerging as a key market due to growing urbanization, retail infrastructure expansion, and increasing awareness of quality and licensed plush products. Market growth in this region is also supported by educational and institutional adoption in schools and pediatric care facilities.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Stuffed and Plush Toys Market

- Mattel Inc.

- Hasbro Inc.

- Spin Master Corp.

- Ty Inc.

- Build-A-Bear Workshop

- Jellycat Ltd.

- Simba Dickie Group

- Steiff Beteiligungsgesellschaft mbH

- Aurora World Inc.

- Sanrio Co., Ltd.

- Bandai Namco Holdings Inc.

- LEGO Group

- VTech Holdings Ltd.

- Kids Preferred LLC

- Gund (Spin Master)